Key Takeaways:

- AI Transformation Leader: $2.2 billion in advanced AI bookings in Q1, nearly doubling year-over-year.

- Price Projection: Based on current execution, ACN stock could reach $306 by August 2028.

- Potential Gains: This target implies a total return of 27% from the current price of $241.

- Annual Return: Investors could see roughly 10% growth over the next 2.6 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Accenture (ACN) just delivered a strong first quarter in recent memory, posting $18.7 billion in revenue while growing 5% in local currency. The company secured $20.9 billion in new bookings, including 33 clients with quarterly bookings exceeding $100 million each.

CEO Julie Sweet is executing an aggressive strategy centered on enterprise AI adoption and digital transformation.

- It booked $2.2 billion in advanced AI projects during Q1, nearly doubling from the prior year. With adjusted operating margin expanding 30 basis points to 17%,

- Accenture continues taking market share from competitors while investing heavily in talent rotation and AI capabilities.

- The company now has nearly 80,000 AI and data professionals who participated in roughly 8 million training hours this quarter.

Despite trading at $241, down significantly from recent highs, the stock offers compelling upside for investors who recognize Accenture’s position at the center of enterprise reinvention.

See analysts’ full growth forecasts and estimates for ACN stock (It’s free) >>>

What the Model Says for Accenture Stock

We analyzed Accenture’s transformation into the dominant partner in enterprise AI adoption and large-scale digital reinvention programs.

The company is expanding beyond traditional consulting work. Advanced AI is now embedded across nearly everything Accenture does, from building digital cores and modernizing data platforms to transforming customer experiences and supply chains.

With 60% of revenue tied to work with its top 10 ecosystem partners—growing faster than overall revenue—Accenture is capturing the full value chain as enterprises reinvent themselves.

The company now serves over 1,300 clients on advanced AI projects, representing 14% of its total client base.

This broad exposure provides runway for expansion while the AI buildout creates unprecedented demand for end-to-end transformation services that integrate technology, process redesign, and talent upskilling.

Using a forecast of 5.9% annual revenue growth and 15.9% operating margins, our model projects the stock will rise to $306 within 2.6 years. This assumes a 16.7x price-to-earnings multiple.

That represents compression from Accenture’s historical P/E averages of 21.1x (one year) and 26.6x (five years). The lower multiple acknowledges macroeconomic uncertainty and muted discretionary spending that has persisted for over a year.

The real value lies in Accenture’s ability to help clients scale AI across enterprises while maintaining industry-leading margins and taking market share in a challenging environment.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ACN stock:

1. Revenue Growth: 5.9%

Accenture’s growth centers on large, transformational programs that translate into revenue more slowly but position the company at the center of clients’ reinvention agendas.

- The company delivered broad-based growth across geographic markets and service types in Q1. Managed services grew 8% in USD terms, driven by high-single-digit growth in technology services.

- Consulting grew 4% in USD terms, as clients prioritize strategic initiatives over discretionary spending.

- Management expects fiscal 2026 revenue growth of 2% to 5% in local currency, including a 1% headwind from federal business. Excluding federal, growth would be 3% to 6%.

The company continues investing roughly $3 billion in strategic acquisitions, including the recent majority stake in DLB Associates, a US-based leader in AI, data center engineering, and consulting, positioning Accenture in the rapidly growing data center consulting market.

2. Operating margins: 15.9%

Accenture is sustaining strong profitability while rotating its workforce and investing in long-term leadership.

The company delivered a 17% adjusted operating margin in Q1, up 30 basis points year over year. This performance reflects execution on fixed-price contracts, which now represent about 60% of total work, up 10 percentage points over three years.

Fixed-price work provides clients with cost certainty while demonstrating Accenture’s ability to deliver outcomes at scale.

Management expects the full-year fiscal 2026 adjusted operating margin of 15.7% to 15.9%, representing 10 to 30 basis points of expansion.

Contract profitability is improving as better pricing shows up in the P&L, even as the company continues significant talent investments.

3. Exit P/E Multiple: 16.7x

The market values Accenture at 17.2x trailing earnings. We assume the P/E will compress slightly to 16.7x over our forecast period.

Near-term discretionary spending remains muted with no clear catalyst for improvement. CEO Julie Sweet noted the company isn’t waiting for market conditions to improve—instead, it is focusing on gaining market share through large, transformational deals and positioning itself to benefit when tailwinds eventually return.

As enterprise AI adoption scales and Accenture demonstrates its ability to deliver measurable outcomes across industries, the company should command a premium multiple.

The company’s fixed-price model, deep ecosystem partnerships, and early leadership in Agentic AI provide competitive advantages that strengthen over time.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

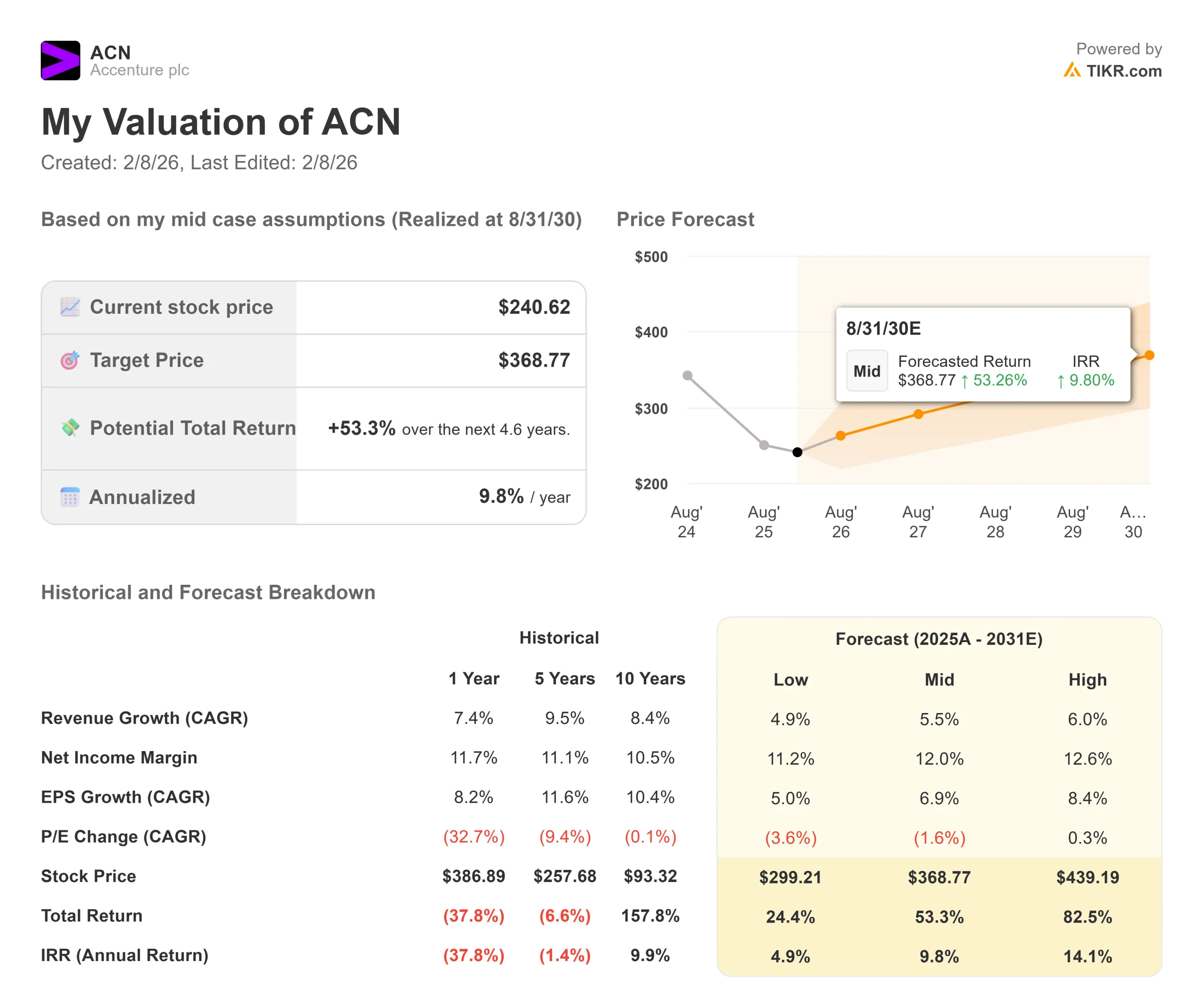

Professional services firms face technology transitions and economic cycles. Here’s how Accenture stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 4.9% and net income margins compress to 11.2%, investors could still see a 24% total return (4.9% annually).

- Mid Case: With 5.5% growth and 12.0% margins, we expect a total return of 53% (9.8% annually).

- High Case: If AI adoption accelerates and Accenture maintains 12.6% margins while growing at 6.0%, total returns could reach 83% (14.1% annually).

See what analysts think about ACN stock right now (Free with TIKR) >>>

The range reflects execution on enterprise AI demand, successful integration of acquisitions, and margin expansion as fixed-price contracts scale.

In the low case, discretionary spending remains weak or AI adoption stalls.

In the high case, enterprise AI demand exceeds expectations and market conditions improve faster than anticipated.

How Much Upside Does Accenture Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!