Key Stats for LyondellBasell Stock

- This-Week Performance: 12%

- 52-Week Range: $42 to $79

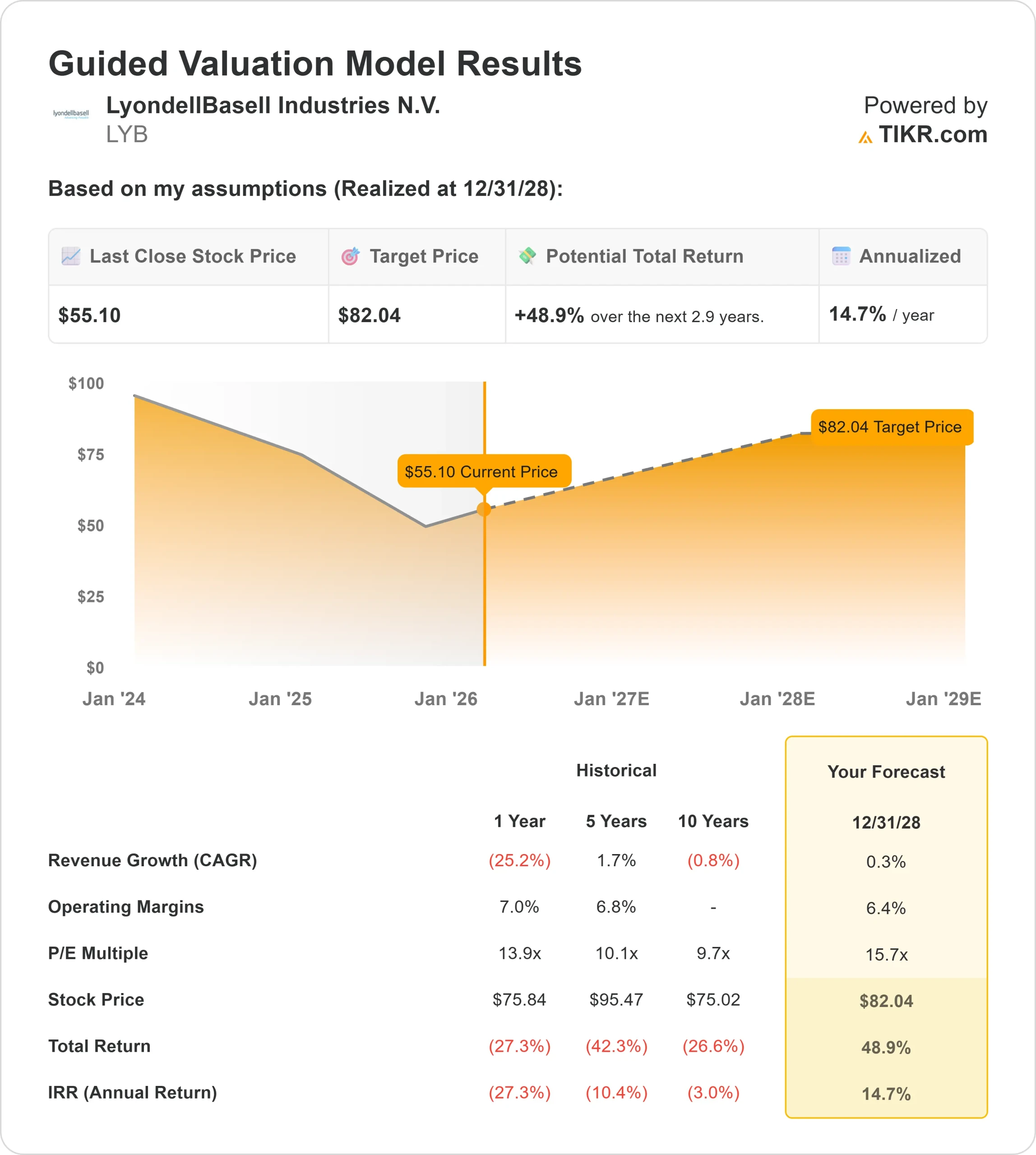

- Valuation Model Target Price: $82

- Implied Upside: 49%

Value your favorite stocks like LyondellBasell with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

LyondellBasell Industries stock rose about 12% this week, trading near $55 per share, as investors reacted to earnings follow-through, heavy institutional repositioning, and fresh analyst price target updates. The advance came even as analysts remain cautious on the sector, suggesting the move was driven more by balance sheet confidence and positioning shifts than by a sharp improvement in industry fundamentals.

Shares moved higher this week as investors focused on significant institutional reshuffling, with large exits offset by a major new long-term position.

Federated Hermes Inc. reduced its stake by 99.4%, selling 2.40 million shares and retaining 14,053 shares worth about $689,000, while Truist Financial cut its position by 54.8% to 51,391 shares valued near $2.52 million.

In contrast, Norges Bank initiated a new position worth roughly $280 million, signaling long-term interest even as other firms trimmed exposure.

Additional filings reflected mixed but active rebalancing. Allianz Asset Management trimmed its stake by 3.3%, holding 565,437 shares worth about $27.7 million, while Altrius Capital Management increased its position by 19.7% to 169,105 shares, making LYB roughly 1.9% of its portfolio.

That split behavior highlights a market reassessing downside risk versus recovery optionality at current prices.

Analyst actions added further context this week. Citigroup raised its price target to $49 while maintaining a neutral rating, implying about 9% downside, while Royal Bank of Canada lifted its target from $49 to $51, still pointing to roughly 5% downside.

Against that backdrop, shares held firm as investors focused on management’s confirmation of $2.3 billion in 2025 operating cash flow, a 95% cash conversion ratio, and continued capital discipline, helping stabilize sentiment despite a still-challenging industry environment.

See analysts’ growth forecasts and price targets for LyondellBasell (It’s free) >>>

Is LyondellBasell Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 0.3%

- Operating Margins: 6.4%

- Exit P/E Multiple: 15.7x

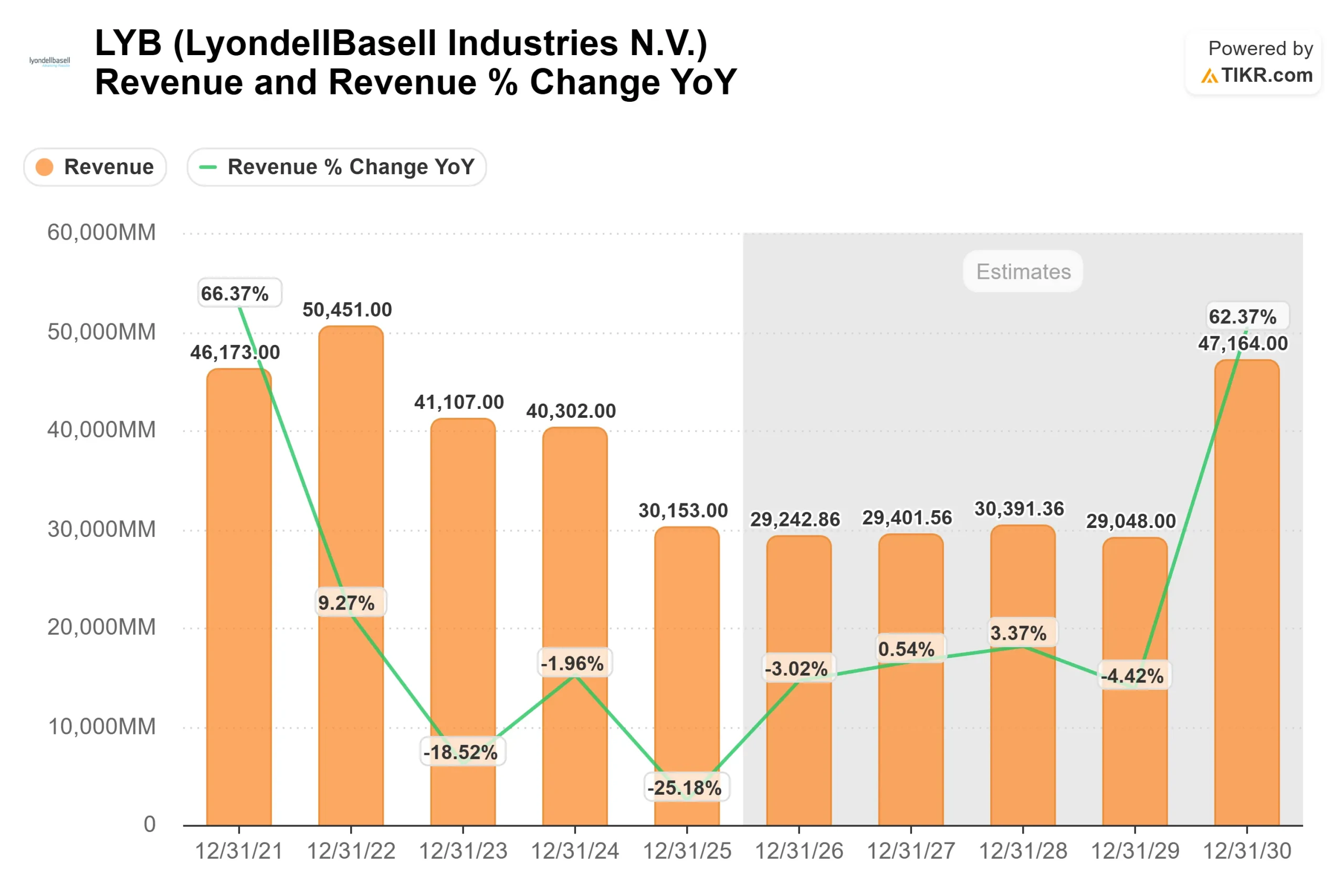

Revenue growth assumptions reflect a business operating near the bottom of a prolonged industry cycle rather than one dependent on volume expansion, with expectations remaining muted while pricing and utilization gradually stabilize.

That framework matters because LyondellBasell’s earnings power is driven less by top-line growth and more by margin normalization once supply and demand rebalance.

Profit recovery is supported by several company-specific developments. Capacity rationalization across global petrochemical markets is accelerating, while LyondellBasell continues to reduce exposure to structurally challenged assets through planned European divestitures.

At the same time, disciplined capital spending, fewer major turnarounds in 2026, and ongoing cost reductions improve cash flow resilience even before a full demand recovery materializes.

This setup supports the view that future returns are tied to margin leverage, asset optimization, and cash generation rather than aggressive revenue acceleration.

Even modest improvements in polyethylene and polypropylene pricing can drive outsized earnings gains due to the company’s fixed-cost structure and operating leverage.

Based on these inputs, the model estimates a target price of $82, implying roughly 49% total upside over about 2.9 years, or roughly 14.7% annualized, which indicates the stock appears undervalued under the firm’s framework.

That upside does not rely on a strong macro rebound, but on margins moving back toward mid-cycle levels as supply discipline holds.

Results over the next year hinge on execution across several higher-impact areas. Continued capacity closures, pricing initiatives supported by low industry inventories, and progress on asset sales remain central to earnings recovery.

Strong free cash flow generation and disciplined capital allocation provide downside protection while positioning the company to benefit as industry conditions improve.

At current levels, LyondellBasell appears undervalued, with future performance driven by margin recovery, supply tightening, and capital discipline rather than top-line growth.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>