Key Stats for Marathon Petroleum Stock

- This-Week Performance: 15%

- 52-Week Range: $115 to $204

- Valuation Model Target Price: $246

- Implied Upside: 21%

Value your favorite stocks like Marathon Petroleum with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Marathon Petroleum stock rose about 15% this week, finishing near $203 per share, as investors reacted to strong earnings follow-through, higher analyst price targets, and fresh institutional positioning data released after the company’s latest results.

Shares moved higher after Marathon’s fourth-quarter earnings confirmed stronger-than-expected cash generation and refining performance, easing concerns around margin durability in a softer refining environment.

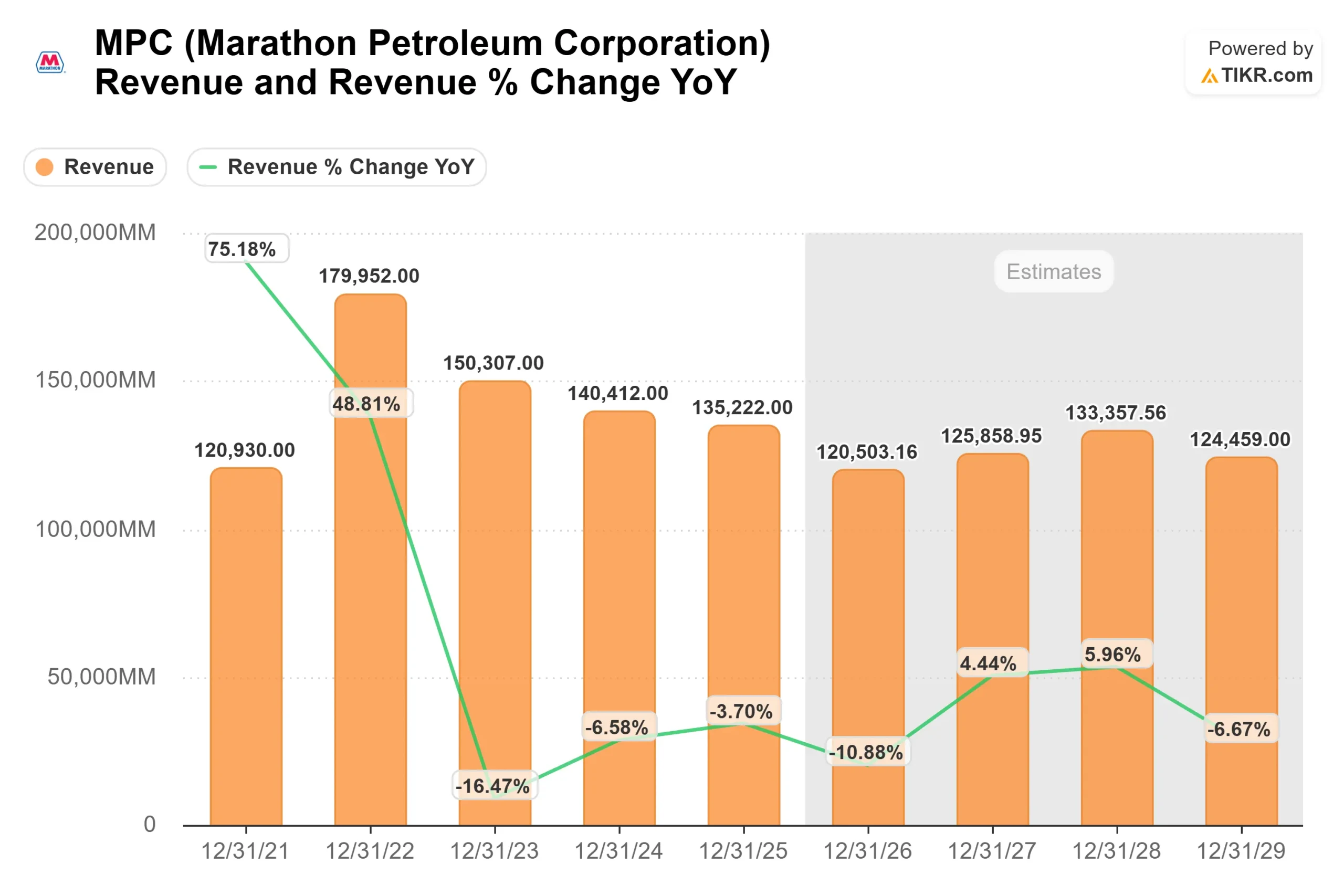

The company reported adjusted EPS of $4.07 and adjusted EBITDA of about $3.5 billion, supported by 95% refinery utilization and record throughput at key facilities, reinforcing confidence in operational execution.

Analyst actions added momentum this week. TD Cowen raised its price target to $198 from $183 and reiterated a Buy rating, aligning with the broader analyst view that Marathon’s cash flow and capital return profile remains intact as the company moves into 2026.

The target increase reflected improved visibility into free cash flow generation and disciplined capital spending plans.

Recent institutional filings showed active repositioning rather than broad risk-off behavior. Canada Post Corp Registered Pension Plan boosted its stake by 256.4%, while Jones Financial Companies and Thrivent Financial for Lutherans also increased holdings, offsetting trims from swisspartners Advisors and Mediolanum International Funds.

With institutional ownership at 76.77%, the mixed but constructive activity supported the stock’s sharp move higher this week.

See analysts’ growth forecasts and price targets for Marathon Petroleum (It’s free) >>>

Is Marathon Petroleum Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): (0.5%)

- Operating Margins: 6.1%

- Exit P/E Multiple: 12.8x

Revenue expectations remain muted, reflecting a refining business normalizing after a cyclical peak rather than one dependent on sustained volume expansion.

That places greater emphasis on margin recovery, cost control, and capital efficiency, areas where Marathon’s scale and integrated refining system provide a competitive advantage.

Analyst assumptions continue to reflect a tight global refining backdrop. Limited new capacity additions, regional refinery closures, and consistently high utilization rates support the view that margins can remain structurally healthier than in prior down cycles, even if revenue trends stay uneven.

Results over the next year hinge on execution across several high-impact drivers. Refining throughput, maintenance efficiency, and regional pricing differentials will play an outsized role in earnings durability as supply constraints persist across key U.S. markets.

Capital allocation further strengthens the setup. Marathon plans roughly $700 million in refining capital spending for 2026, about a 20% reduction year over year, focused on high-return projects that target returns of 25% or more, including expanding crude throughput by 30,000 barrels per day at Garyville and adding 10,000 barrels per day of export-grade gasoline capacity.

Midstream contributions add another layer of support. MPLX plans to deploy $2.4 billion of growth capital, with 90% directed toward Natural Gas and NGL Services, and targets a 12.5% distribution growth rate that is expected to lift annual cash distributions to Marathon above $3.5 billion, helping fund dividends and buybacks.

Based on a current price near $203 and a valuation model target of about $246, the setup implies roughly 21% total upside over about 2.9 years, translating to an annualized return near 7%, which screens as undervalued under these assumptions.

At current levels, Marathon Petroleum appears undervalued, with future performance driven by margin resilience, disciplined refining execution, midstream cash flows, and sustained capital returns rather than top-line growth acceleration.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>