Key Takeaways:

- Scores Dominance: FICO Score remains the standard for 90% of top U.S. lenders amid major product launches.

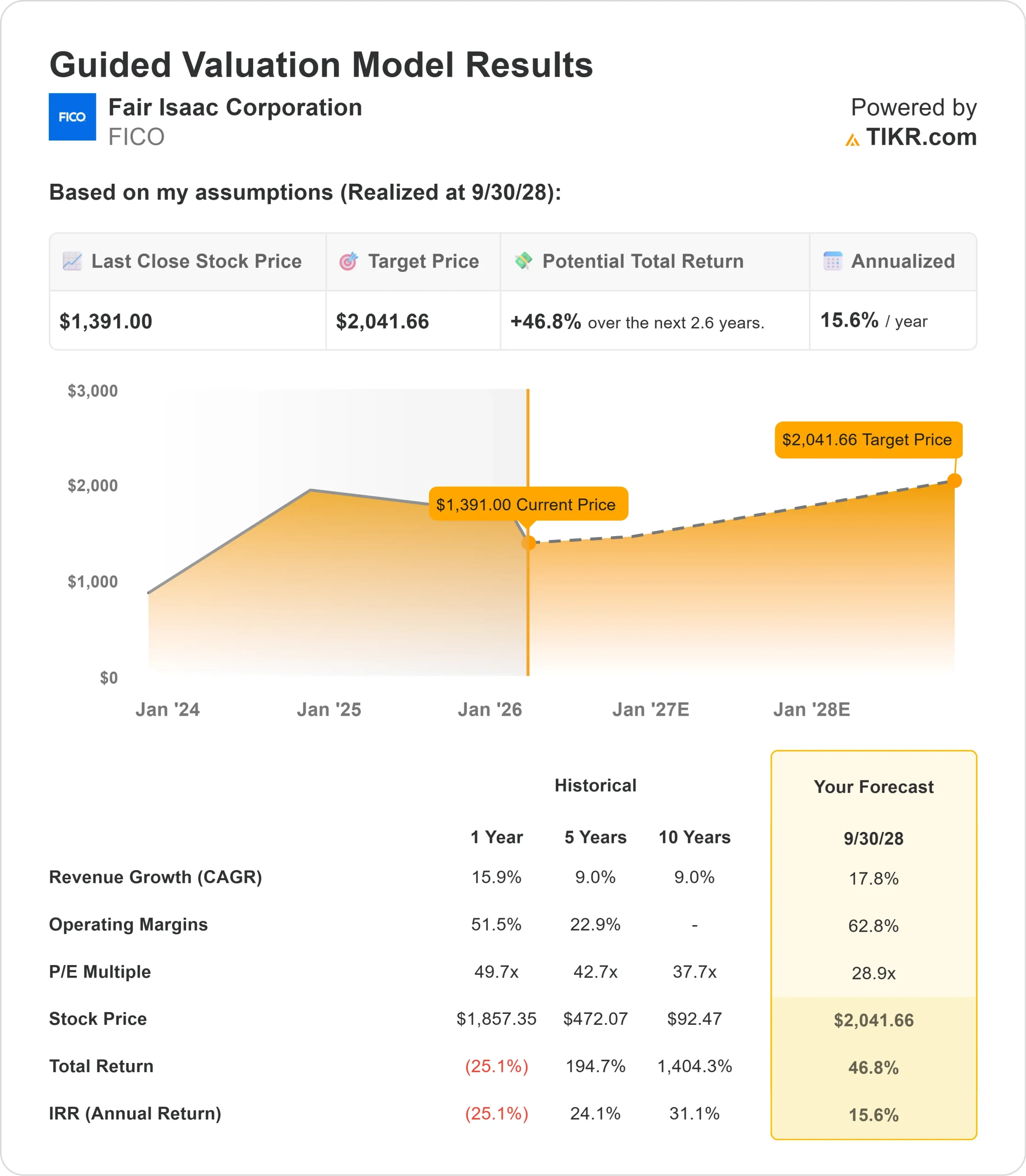

- Price Projection: Based on current execution, FICO stock could reach $2,042 by September 2028.

- Potential Gains: This target implies a total return of 47% from the current price of $1,391.

- Annual Return: Investors could see roughly 16% growth over the next 2.6 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Fair Isaac Corporation (FICO) delivered impressive first-quarter fiscal 2026 results with revenues of $512 million, up 16% year-over-year, while maintaining its full-year guidance.

CEO Will Lansing emphasized strong momentum across both business segments. The company reported non-GAAP earnings of $7.33 per share, up 27% from the prior year, and generated $165 million in free cash flow during the quarter.

- Scores segment revenues surged 29% to $305 million, driven primarily by B2B growth of 36%. Mortgage origination revenues jumped 60% versus last year, reflecting both higher unit pricing and increased volume as the housing market showed signs of recovery.

- The company announced four new strategic participants in its FICO Mortgage Direct Licensing Program, including Xactus, Cotality, Ascend Companies, and CIC Credit. MeridianLink, a major platform provider, also joined the program

- Multiple resellers are progressing through production testing, with one large partner close to completing integration and another already testing downstream systems. The program currently supports classic FICO scores, with FICO Score 10T expected to be available for both conforming and nonconforming markets in the first half of calendar 2026.

- FICO Score 10T represents a meaningful advancement in credit risk assessment. The company has nearly doubled its adopter program participants over the past year, now including lenders with over $377 billion in annual originations and $1.6 trillion in servicing volume.

- The software business showed encouraging signs with record quarterly ACV bookings of $38 million, including an above-average international multi-use case platform deal.

- Platform ARR grew 33% to $303 million, now representing 40% of total software ARR. Total software ARR reached $766 million, up 5% year-over-year.

FICO was recognized as a leader in Gartner’s January 2026 Magic Quadrant for Decision Intelligence Platforms, positioned highest for ability to execute.

The company now serves over 150 platform customers, with more than half leveraging multiple use cases.

See analysts’ full growth forecasts and estimates for FICO stock (It’s free) >>>

What the Model Says for Fair Isaac Stock

We analyzed FICO’s transformation into the dominant credit-scoring provider and a growing decision-intelligence platform.

- The Scores business benefits from structural advantages. FICO Score remains the industry standard, creating significant switching costs for lenders.

- Recent price increases in mortgage originations, combined with volume recovery, provide near-term tailwinds.

- The Direct Licensing Program and adoption of FICO Score 10T create additional growth drivers.

- These innovations expand FICO’s addressable market and strengthen relationships with lenders and resellers.

- The software platform shows accelerating momentum. Platform ARR growth of 33% demonstrates strong demand for real-time decision intelligence.

Using a forecast of 17.8% annual revenue growth and 62.8% operating margins, our model projects the stock will rise to $2,042 within 2.6 years. This assumes a 28.9x price-to-earnings multiple.

That represents compression from FICO’s historical P/E averages of 49.7x (one year) and 50x (three years). The lower multiple reflects near-term regulatory uncertainty regarding credit-scoring alternatives and the ongoing transition to new products.

The real value lies in FICO’s market dominance and its potential to expand its platform across financial services and other verticals.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for FICO stock:

1. Revenue Growth: 17.8%

FICO’s growth centers on expanding adoption across Scores innovations and platform momentum. First quarter Scores revenue grew 29%, with particular strength in mortgage originations, up 60%.

Management expects continued platform bookings acceleration. Recent large deals and expanding use cases among existing customers support sustained double-digit growth.

Auto origination revenues grew 21%, while credit card and personal loan revenues increased 10%.

2. Operating margins: 62.8%

FICO has maintained industry-leading margins through operational discipline and high-value products. The company expanded non-GAAP operating margins by 432 basis points year-over-year to 54% in the first quarter.

The platform business is designed for profitable scaling. As more customers migrate from legacy solutions and platform ARR grows, margin expansion opportunities increase through operating leverage.

3. Exit P/E Multiple: 28.9x

The market values FICO at 30.9x earnings. We assume modest compression to 28.9x over our forecast period. Near-term uncertainty around regulatory decisions on credit scoring alternatives and the FICO Score 10T approval timeline creates some multiple pressures.

However, FICO’s dominant market position, recurring revenue model, and expanding platform business should support a premium valuation as execution continues.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

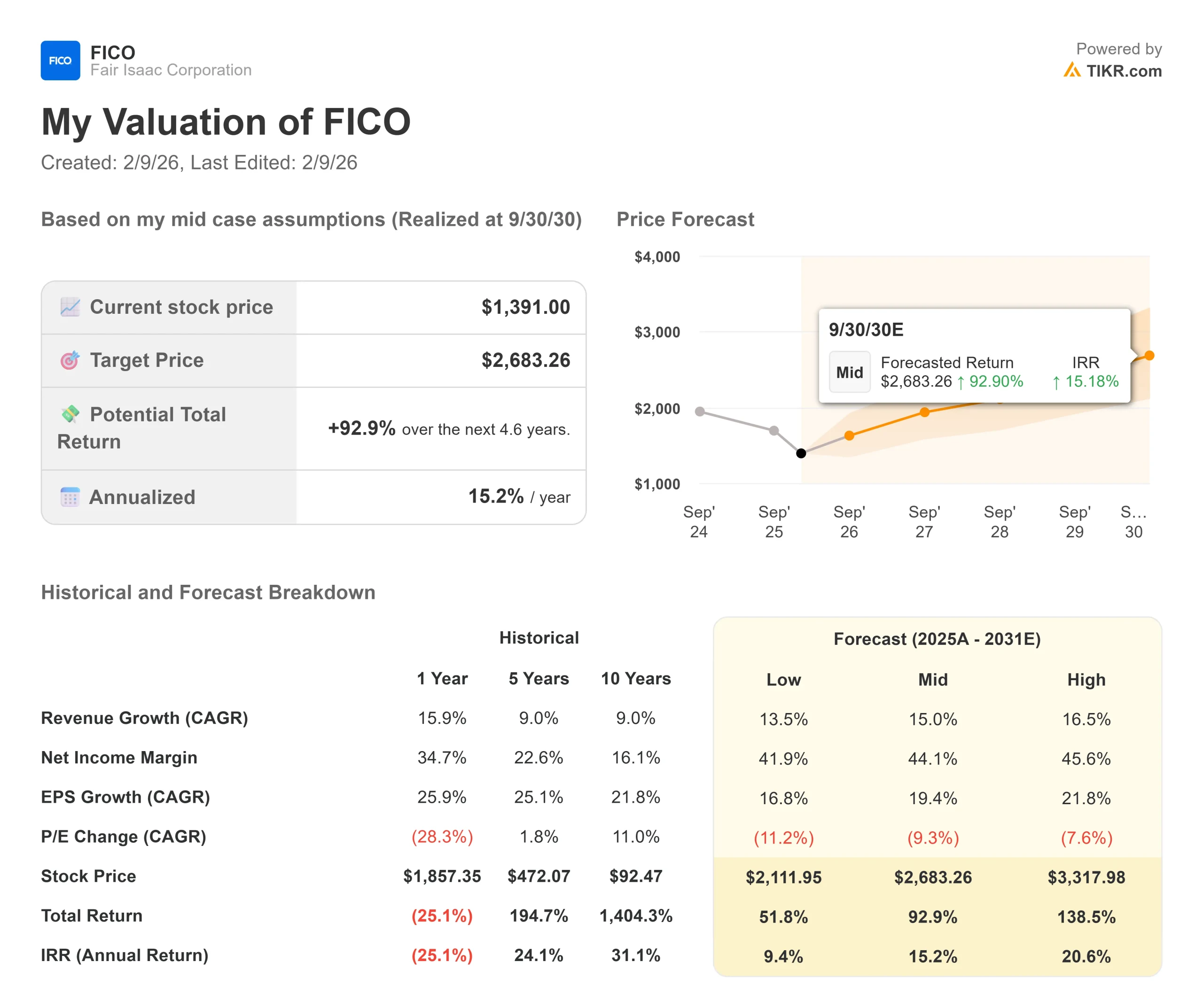

Credit scoring and decision intelligence are evolving under regulatory and technological pressures. Here’s how FICO stock might perform under different scenarios through September 2030:

- Low Case: If revenue growth slows to 13.5% and net income margins compress to 41.9%, investors still see a 51.8% total return (9.4% annually).

- Mid Case: With 15% growth and 44.1% margins, we expect a total return of 92.9% (15.2% annually).

- High Case: If Scores momentum accelerates and platform adoption drives 16.5% revenue growth while FICO maintains 45.6% margins, returns could hit 138.5% total (20.6% annually).

See what analysts think about FICO stock right now (Free with TIKR) >>>

The range reflects execution on Direct Licensing adoption, FICO Score 10T approval timing, regulatory outcomes, and platform customer expansion across use cases and verticals.

How Much Upside Does Fair Isaac Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!