Key Takeaways:

- Network Transformation: UPS reducing Amazon volume by 1M packages/day while automating 68% of facilities.

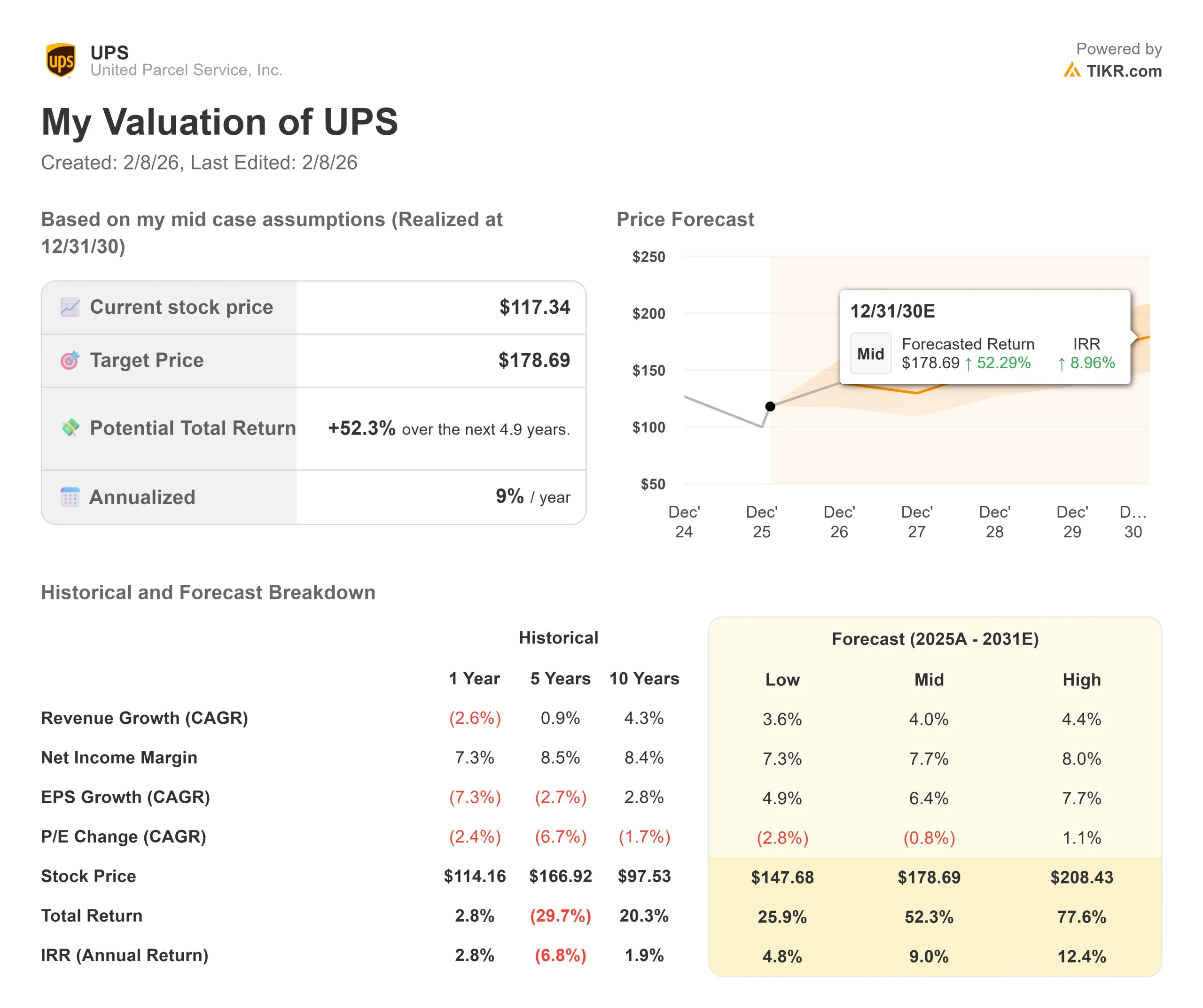

- Price Projection: Based on current execution, UPS stock could reach $141 by December 2028.

- Potential Gains: This target implies a total return of 20% from the current price of $117.

- Annual Return: Investors could see roughly 6.6% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

United Parcel Service (UPS) is in the middle of a major transformation. The company posted Q4 revenue of $24.5 billion and full-year revenue of $88.7 billion, but those numbers tell only part of the story.

CEO Carol Tomé is executing a deliberate strategy to shrink the network, improve margins, and position UPS for sustainable growth.

- The company reduced Amazon volume by approximately one million pieces per day in 2025 and plans to cut another one million in 2026.

- This glide-down enabled UPS to close 93 buildings, reduce labor hours by 26.9 million, and eliminate 48,000 operational positions.

- Despite the volume decline, UPS delivered $3.5 billion in savings and maintained industry-leading service for the eighth consecutive year.

CFO Brian Dykes emphasized that 2026 will be a transitional year with different halves. The first half faces headwinds from the Amazon glide-down, outsourcing part of Ground Saver to USPS, and MD-11 fleet retirement costs.

The second half should show operating profit growth as UPS exits with a leaner, more efficient network built for margin expansion.

See analysts’ full growth forecasts and estimates for UPS stock (It’s free) >>>

What the Model Says for UPS Stock

We analyzed UPS through its transformation into a more efficient logistics operator focused on premium customers and high-value services.

The company is shifting away from low-margin e-commerce volume.

- In Q4, small and medium business (SMB) penetration reached 31.2% of total U.S. volume, the highest fourth-quarter penetration in company history.

- Business-to-business (B2B) volume hit 37.5%, the best Q4 penetration in six years. This mix improvement drove revenue per piece up 8.3% year-over-year, the strongest growth in four years.

- UPS now processes 66.5% of its volume through automated facilities, which have a 28% lower cost per piece than conventional facilities.

- The company plans to increase automation to 68% by year-end 2026, adding 24 new automated facilities while closing at least 24 more conventional buildings in the first half alone.

Using a forecast of 2.6% annual revenue growth and 10.3% operating margins, our model projects the stock will rise to $141 within 2.9 years. This assumes a 13.9x price-to-earnings multiple.

That represents compression from UPS’s historical P/E averages of 15.9x (five years) and 16.4x (ten years).

The lower multiple reflects execution risks from the network transformation, near-term margin pressure in the first half of 2026, and uncertainty around international trade policies.

The real value lies in completing the network reconfiguration while capturing growth in SMB, healthcare, and premium services that command higher margins.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for UPS stock:

1. Revenue Growth: 2.6%

UPS expects modest growth as it completes its strategic transformation.

The company anticipates flat U.S. domestic revenue in 2026, with declines in the first half offset by growth in the second half. SMB and enterprise revenue should grow low single digits in H1, then accelerate to mid-single digits in H2 as the Amazon glide-down concludes.

International revenue faces headwinds from tariff changes and the elimination of the de minimis exemption, which drove U.S. import volume down 24.4% year-over-year in Q4.

However, UPS is seeing double-digit growth in Asian markets outside China, with new hubs in Vietnam, the Philippines, and Hong Kong that are expanding capacity across expanding trade lanes.

2. Operating margins: 10.3%

UPS is targeting sustained margin improvement through operational efficiency.

The company delivered 9.8% operating margin in 2025 despite volume declines. Management expects flat margins in 2026 as first-half transition costs offset second-half improvements. U.S. domestic operating margin should exit 2026 with an increase after dipping to mid-single digits in Q1.

UPS plans $3 billion in savings from the final phase of the Amazon glide-down, including 25 million fewer operational hours and up to 30,000 position reductions through attrition and voluntary driver buyouts.

Outsourcing Ground Saver to USPS will improve economics, though full benefits won’t materialize until 2027.

3. Exit P/E Multiple: 13.9x

The market values UPS at 16.6x earnings. We assume the P/E will compress to 13.9x over our forecast period.

Near-term execution complexity weighs on the multiple. The company faces Q1 2026 margin pressure from Ground Saver transition costs, timing lags in removing Amazon-related expenses, and additional aircraft lease costs from the MD-11 retirement.

As UPS demonstrates consistent execution in the second half of 2026 and proves it can grow while expanding margins, the multiple should stabilize. The company’s investments in capabilities such as RFID technology are already driving commercial wins, with Q4 wins up 25% year over year.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Logistics companies face economic cycles and competitive pressures. Here’s how UPS stock might perform under different scenarios through December 2028:

- Low Case: If revenue growth slows to 3.6% and margins are at 7.3%, investors still see total returns of 25.9% (4.8% annually).

- Mid Case: With 4.0% growth and 7.7% margins, we expect a total return of 52.3% (9% annually).

- High Case: If the network transformation exceeds expectations and UPS captures accelerated growth in SMB and healthcare to 4.4%, while expanding margins 8% faster than anticipated, returns could be substantially higher, at around 77.6% (12.4% annually).

See what analysts think about UPS stock right now (Free with TIKR) >>>

The range depends on completing the Amazon glide-down without service issues, capturing profitable market share in targeted segments, and sustaining margin expansion despite labor cost increases scheduled for the back half of the Teamsters contract.

How Much Upside Does UPS Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!