Key Takeaways:

- AI Networking Surge: $2.75B AI revenue target for 2026, up from $1.5B in 2025.

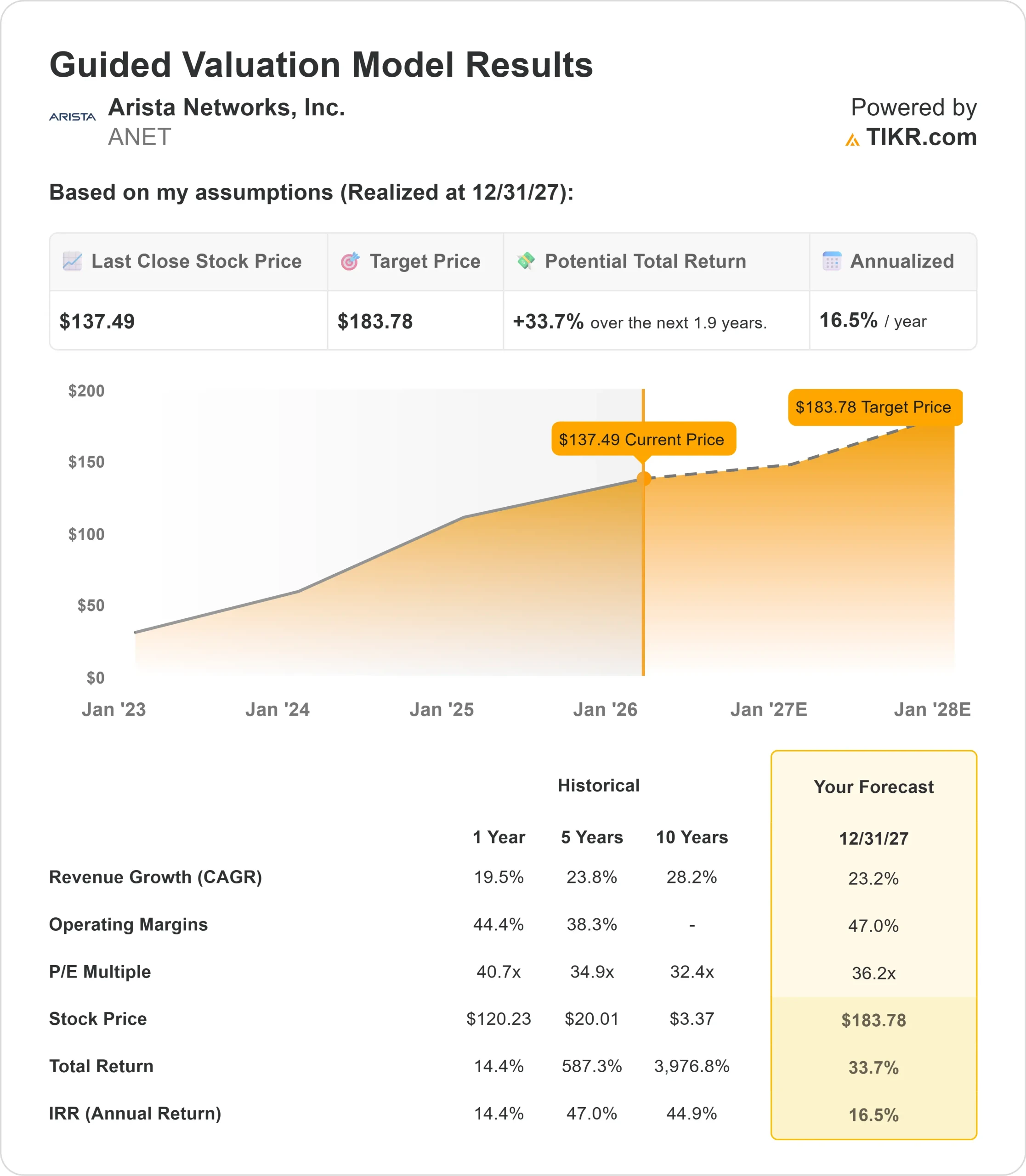

- Price Projection: Based on current execution, ANET stock could reach $184 by December 2027.

- Potential Gains: This target implies a total return of 34% from the current price of $137.

- Annual Return: Investors could see roughly 16.5% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Arista Networks (ANET) just posted its 19th consecutive record quarter with revenue hitting $2.31 billion in Q3 2025, up 27.5% year-over-year. The networking leader is capitalizing on the AI infrastructure boom while maintaining an industry-leading 65.2% gross margin.

CEO Jayshree Ullal and newly promoted President & CTO Ken Duda are executing an aggressive strategy centered on AI data center networking.

The company guided FY 2025 revenue to $8.87 billion (26-27% growth) and raised its 2026 outlook to $10.65 billion, representing 20% growth on a much larger base.

Arista’s AI networking revenue is accelerating sharply – from a $1.5 billion target in 2025 to $2.75 billion in 2026.

The company is winning across both back-end AI training networks and front-end inference deployments at cloud titans, while its campus business continues to grow steadily toward $1.25 billion.

Despite this momentum, Arista stock trades at $137, offering meaningful upside for investors who recognize the company’s dominant position in AI networking infrastructure.

See analysts’ full growth forecasts and estimates for ANET stock (It’s free) >>>

What the Model Says for Arista Networks Stock

We analyzed Arista’s transformation into the premier networking provider for AI data centers, with unmatched software capabilities and customer relationships.

The company is capturing share across multiple AI networking segments. While competitors like NVIDIA bundle networking with GPUs and white-box vendors offer commodity solutions, Arista provides the “best” option – superior hardware with built-in diagnostics and the industry’s most reliable EOS operating system.

Arista now works closely with AI model developers such as OpenAI and Anthropic, not just infrastructure providers.

The company’s Etherlink portfolio supports scale-out networking today and is positioned for scale-up opportunities as Ethernet standards like ESUN mature. With cloud titans building 100,000+ GPU clusters and power-hungry gigawatt-scale data centers, Arista sits at the center of unprecedented networking demand.

Using a forecast of 23.2% annual revenue growth and 47% operating margins, our model projects the stock will rise to $184 within 1.9 years. This assumes a 36.2x price-to-earnings multiple.

That represents modest compression from Arista’s historical P/E averages of 40.7x (one year) and 34.9x (five years). The slightly lower multiple acknowledges potential moderation in AI infrastructure spending and competitive dynamics, while still reflecting Arista’s premium position.

The real value lies in sustaining AI networking leadership, expanding into scale-up architectures, and maintaining higher margins through operational excellence.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ANET stock:

1. Revenue Growth: 23.2%

Arista’s growth is driven by explosive AI networking demand across multiple customer segments.

The company achieved its $1.5 billion AI target for 2025 and now expects $2.75 billion in 2026 – an 83% increase in AI revenue alone. Management views AI networking as a long-term growth driver as models scale, requiring massive back-end training networks and expanding front-end inference infrastructure.

Beyond AI, Arista’s campus business continues gaining traction following the VeloCloud acquisition. The company targets $1.25 billion in campus revenue for 2026, up from roughly $750-800 million in 2025. International expansion and new customer wins provide additional runway.

2. Operating margins: 47%

Arista sustains excellent profitability through operational discipline and software differentiation.

The company delivered a 48.6% operating margin in Q3 2025, demonstrating its ability to maintain efficiency amid rapid growth. Q4 guidance of 47-48% operating margin and the 2026 outlook of 43-45% reflect investments in go-to-market expansion and product development, while still far exceeding industry peers.

Gross margins remain strong at 64-65%, supported by software and services revenue approaching 19% of total sales. Even as the customer mix shifts toward high-volume cloud titans, Arista’s software value and operational excellence sustain industry-leading profitability.

3. Exit P/E Multiple: 36.2x

The market currently values Arista at 42.9x earnings. We assume compression to 36.2x over our forecast period.

Near-term uncertainty around AI infrastructure spending patterns and competitive intensity from bundled solutions justifies some compression of multiples.

However, Arista’s track record of 19 consecutive quarters of record results, deep customer relationships with every major cloud provider, and an expanding total addressable market support a premium valuation.

As the company demonstrates consistent execution at a $10+ billion revenue scale and maintains differentiation through software innovation, the multiple should stabilize well above the networking industry average.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

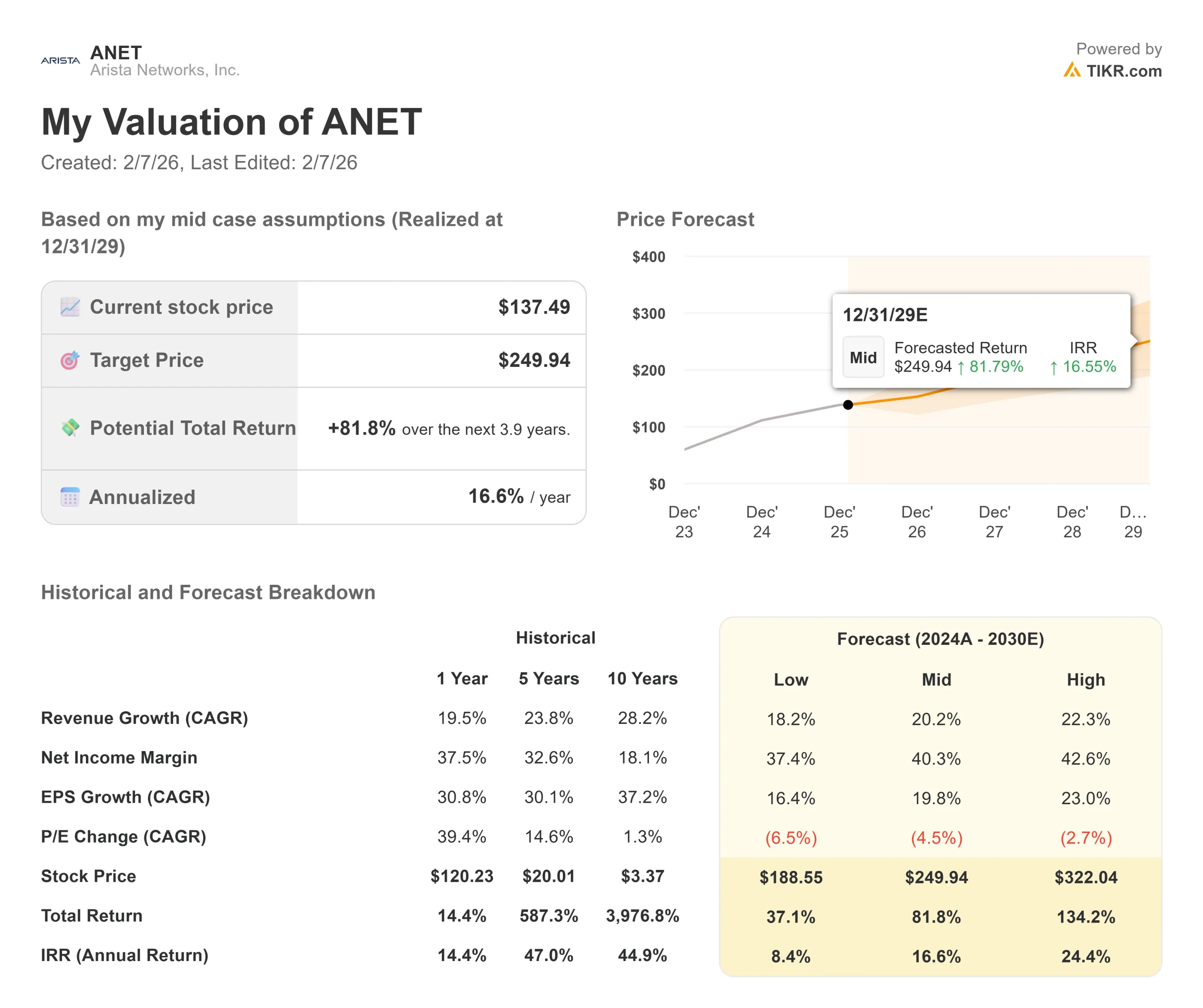

AI networking faces both massive opportunities and execution challenges. Here’s how Arista stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth slows to 18.2% and net income margins compress to 37.4%, investors still see a 37.1% total return (8.4% annually).

- Mid Case: With 20.2% growth and 40.3% margins, we expect a total return of 81.8% (16.6% annually).

- High Case: If AI infrastructure accelerates and Arista maintains 42.6% margins while growing at 22.3%, total returns could reach 134.2% (24.4% annually).

See what analysts think about ANET stock right now (Free with TIKR) >>>

The range reflects execution on AI networking demand, successful scale-up Ethernet adoption, and maintaining margin discipline as the business scales.

In the low case, AI spending moderates or competitive pressures from bundled solutions intensify.

In the high case, AI infrastructure demand exceeds expectations, Arista wins scale-up networking share earlier than anticipated, and the campus business accelerates faster than expected.

How Much Upside Does Arista Networks Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!