Key Takeaways:

- Earnings Momentum: Arm Holdings delivered Q3 revenue of $1 billion and guided Q4 revenue to $1 billion, beating estimates and reinforcing execution strength as Arm Holdings expands licensing demand across AI, data center, and automotive markets.

- Strategic Visibility: Arm Holdings scheduled its Arm Everywhere event for March 24 2026, signaling deeper focus on AI compute platforms as management positions the architecture at the center of next-generation semiconductor roadmaps.

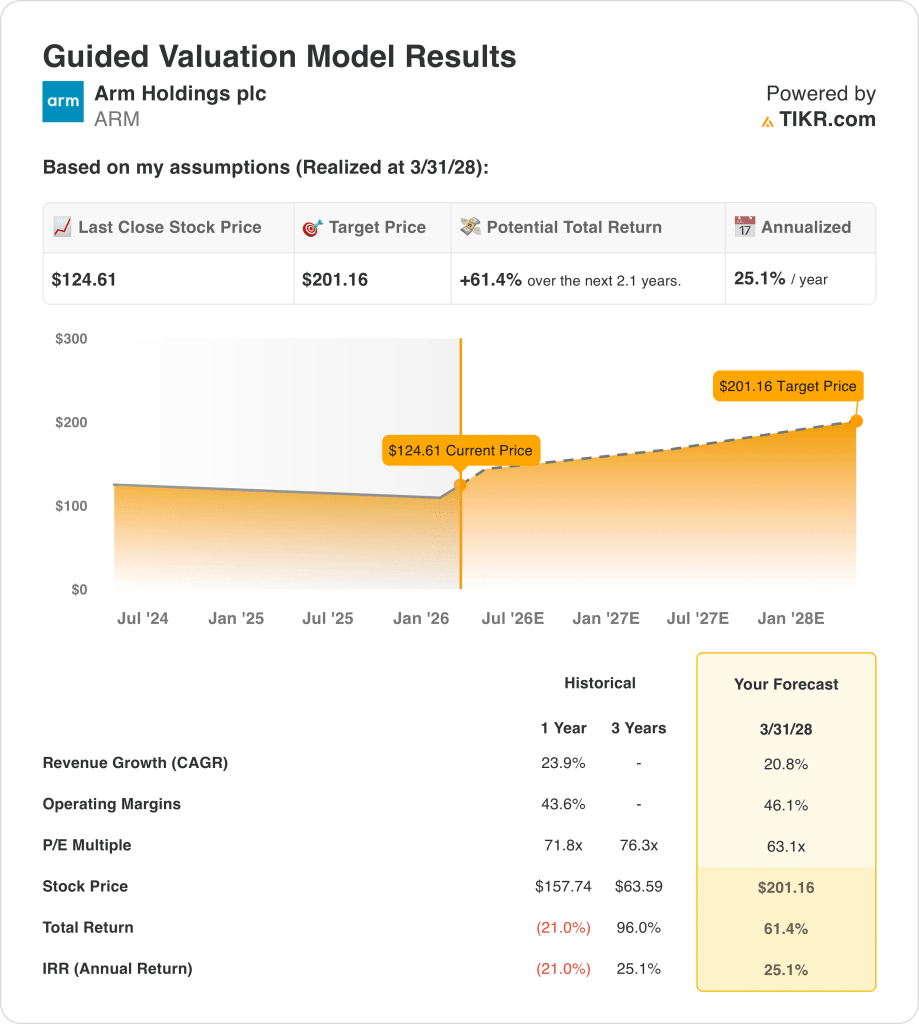

- Valuation Framework: Based on sustained revenue growth near 21% and operating margins expanding toward 46%, Arm Holdings stock could reach $201 by fiscal 2028 using a normalized multiple of 63x earnings.

- Return Math: From the current Arm Holdings price of $125, the $201 target implies 61% total upside and a 25% annualized return over roughly 2 years driven by earnings growth and multiple normalization.

Arm Holdings plc (ARM) designs and licenses CPU architectures and system IP used by semiconductor manufacturers across smartphones, data centers, automotive systems, and IoT devices, earning revenue primarily through upfront licenses and ongoing royalties tied to unit volumes.

Financially, Arm’s revenue reached $4 billion in fiscal 2025, gross profit approached $4 billion, and operating income rebounded to $1 billion as operating margins recovered to 21% following elevated R&D investment.

Arm stock’s operating expenses totaled $3 billion in fiscal 2025, driven largely by $2 billion of R&D spending, reflecting management’s emphasis on long-term platform relevance rather than near-term margin maximization.

Recent results reinforced that strategy, with Q3 revenue of $1 billion and Q4 revenue guidance of $1 billion exceeding expectations as AI-related licensing activity accelerated across infrastructure and automotive end markets.

Last week on earnings call, Arm’s CEO, Rene Haas stated, “We are seeing strong demand for Arm across AI, cloud, and automotive as customers build more efficient compute platforms,” underscoring management’s focus on architectural ubiquity rather than vertical integration.

With revenue projected near $5 billion in fiscal 2026 and normalized net income approaching $2 billion, investor attention centers on whether a valuation near 63x earnings fairly reflects growth durability versus execution risk at current scale.

What the Model Says for ARM Stock

Arm stock benefits from scalable IP economics and low capital intensity, supporting elevated expectations as operating margins reached 46.1% alongside strong platform positioning.

However, the model assumes 20.8% revenue growth, 46.1% margins, and a 63.1x exit multiple, producing a $201.16 target price by fiscal 2028.

From $124.61, the modeled 61.4% total upside and 25.1% annualized return exceed opportunity costs relative to typical public equity alternatives.

The model signals a Buy, as a 25.1% annualized return reflects risk-adjusted compensation well above standard equity hurdle rates.

With a modeled 25.1% annualized return exceeding a typical 10% equity hurdle, the valuation emphasizes capital appreciation over preservation, indicating risk-adjusted compensation is sufficient, justifying a Buy under disciplined valuation logic.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Arm stock:

1. Revenue Growth: 20.8%

Arm stock recorded 23.9% revenue growth over the last year, supported by licensing momentum across AI infrastructure, automotive compute, and rising royalty intensity from newer architectures.

Current execution supports continued expansion, with revenue at $4 billion in fiscal 2025 and projected near $5 billion in fiscal 2026 as Arm deepens penetration across cloud and edge platforms.

Sustaining 20.8% growth requires AI-related licensing conversion and stable end-market volumes, while smartphone weakness or customer concentration would translate quickly into growth deceleration.

This is below the historical 1-year revenue growth of 23.9%, indicating the model assumes deceleration consistent with scale rather than persistence of peak-cycle expansion.

2. Operating Margins: 46.1%

Operating margins of Arm stock averaged 43.6% over the last year, reflecting Arm’s IP-heavy model offset by elevated R&D investment to maintain architectural relevance.

Recent performance shows operating income rebounding to $1 billion, with scale benefits and licensing mix supporting margin expansion despite roughly $2 billion in annual R&D spending.

Reaching 46.1% margins assumes monetization efficiency and cost discipline persist, while renewed investment intensity or pricing pressure would erode incremental operating leverage.

Compared to market expectations embedded in forward valuation through 12/31/26 E, margin assumptions align with visible operating leverage rather than a structural reset.

This is above the historical 1-year operating margin of 43.6%, indicating the model assumes incremental efficiency gains rather than a step-change in cost structure.

3. Exit P/E Multiple: 63.1x

rm Holdings has traded at elevated valuation levels, with a 1-year P/E of 71.8x and a 2/9/26 NTM P/E of 63.07x reflecting long-duration earnings expectations.

At exit, earnings are assumed to scale alongside 46.1% margins, meaning valuation capitalizes durable profitability already embedded in forward earnings expectations.

The 63.1x exit multiple assumes execution consistency rather than multiple expansion, while any earnings shortfall would result in rapid compression given limited valuation buffer.

Relative to the 2026 market P/E assumption of 63.07x, the model effectively holds prevailing sentiment constant to avoid compounding optimism at the terminal year.

This is below the historical 1-year P/E of 71.8x, indicating the model assumes valuation compression as growth matures and earnings durability replaces scarcity-driven premiums.

What Happens If Things Go Better or Worse?

Arm Holdings stock paths depend on AI licensing momentum, royalty mix progression, and sustained execution discipline through 2030.

- Low Case: If AI demand moderates and licensing conversion slows, revenue grows around 19.3% and margins stay near 43.4% → 17.4% annualized return.

- Mid Case: With core licensing demand holding and cost discipline intact, revenue growth near 21.4% and margins improving toward 46.3% → 25.8% annualized return.

- High Case: If AI adoption accelerates and royalties scale efficiently, revenue reaches about 23.5% and margins approach 48.8% → 34.0% annualized return.

How Much Upside Does Arm Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!