Key Takeaways:

- AI Security Leadership: PANW is capturing early AI security demand with Prisma AIRS 2.0, addressing the 94% of organizations lacking AI security guardrails.

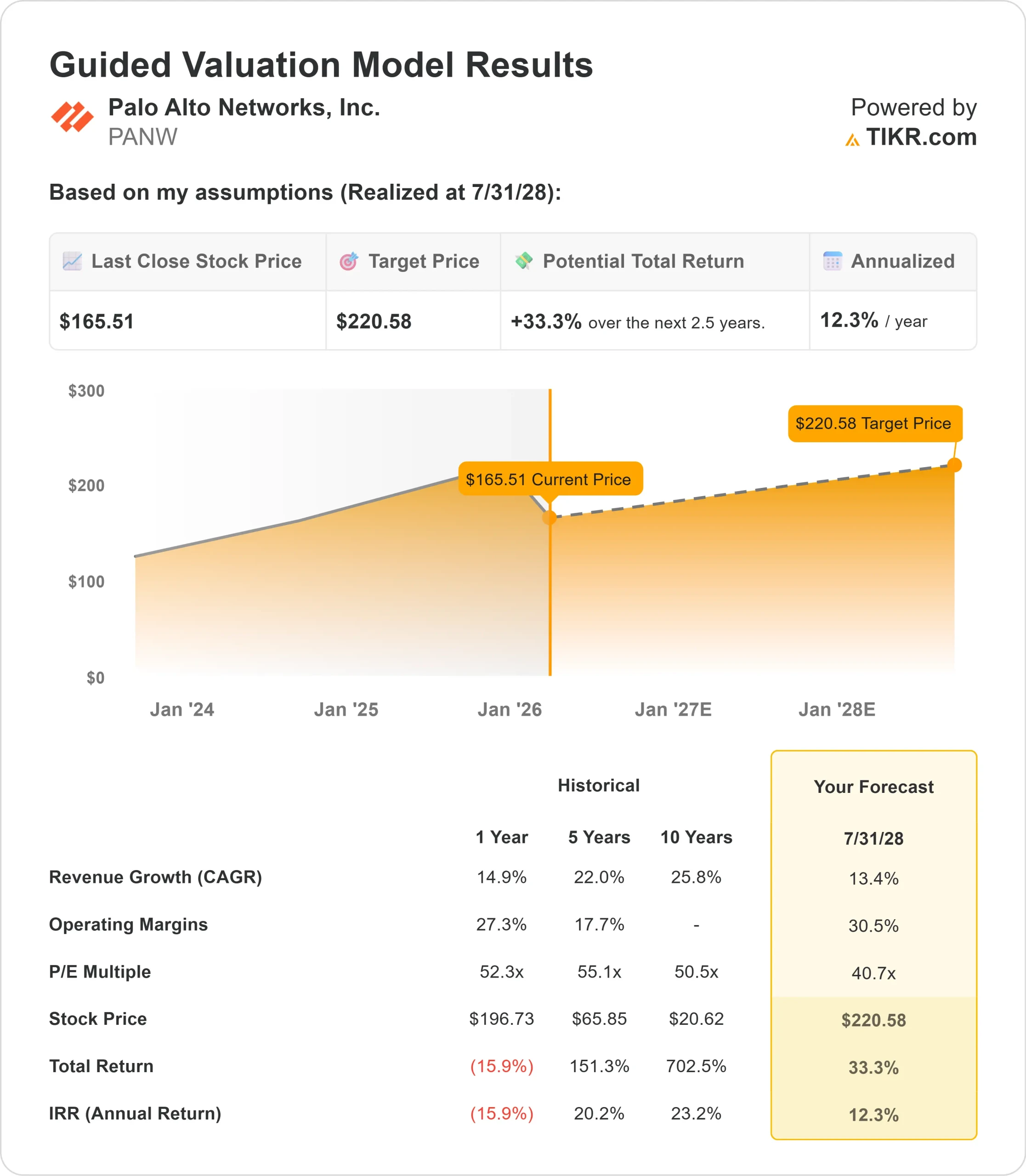

- Price Projection: Based on current execution, PANW stock could reach $221 by July 2028.

- Potential Gains: This target implies a total return of 33% from the current price of $166.

- Annual Return: Investors could see roughly 12% growth over the next 2.5 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Palo Alto Networks (PANW) delivered exceptional first-quarter fiscal 2026 results, exceeding expectations across all guided metrics and demonstrating the impact of its platformization strategy.

The company achieved 24% RPO growth, 29% NGS ARR expansion, and 16% total revenue growth. CEO Nikesh Arora emphasized that customers are shifting from managing vendor sprawl to demanding superior security outcomes through unified platforms.

- The threat landscape is evolving faster than anticipated because of AI. Recently, a major AI platform reported the first known instance of an AI agent autonomously conducting a large-scale nation-state cyberattack. This marked a turning point where AI hackers are no longer a future threat but a present reality.

- SASE had a phenomenal quarter, with ARR growing 34% to surpass $1.3 billion. This makes Palo Alto the fastest-growing SASE provider at scale. The company now serves approximately 6,800 SASE customers, including one-third of the Fortune 500.

- Software firewalls are emerging as a hidden gem. Product revenues grew 23%, with nearly half now driven by software form factors. As AI transformation accelerates cloud workload growth, software firewalls provide essential runtime protection for new AI data centers.

- XSIAM continued its trajectory, with approximately 470 customers, each averaging over $1 million in ARR. The platform processes 15 petabytes of telemetry daily. Over 60% of deployed customers have reduced their median response time from days or weeks to minutes.

- The company announced two significant acquisitions. The CyberArk acquisition remains on track for fiscal Q3 close, with overwhelming shareholder support. The Chronosphere acquisition for $3.35 billion addresses the observability market, delivering comprehensive capabilities at one-third the cost of competitors.

Management raised its FY 2030 NGS ARR target from $15 billion to $20 billion, reflecting confidence in core business strength and expanding opportunities.

See analysts’ full growth forecasts and estimates for PANW stock (It’s free) >>>

What the Model Says for Palo Alto Networks Stock

We analyzed Palo Alto Networks’ transformation into a comprehensive cybersecurity platform provider with an expanding addressable market.

The company benefits from multiple growth drivers. Platformization continues accelerating as customers consolidate disparate point products.

AI security represents a massive opportunity, with 94% of organizations lacking necessary security guardrails despite 78% embracing AI transformation.

Using a forecast of 13.4% annual revenue growth and 30.5% operating margins, our model projects the stock will rise to $221 within 2.5 years. This assumes a 40.7x price-to-earnings multiple.

That represents compression from Palo Alto’s historical P/E averages of 52.3x (one year) and 52.1x (three years). The lower multiple acknowledges integration complexity from two major acquisitions and normal multiple compression as the company scales.

The real value lies in capturing the shift toward platformization while expanding into identity security and observability markets experiencing inflection points due to AI.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PANW stock:

1. Revenue Growth: 13.4%

Palo Alto’s growth centers on structural demand for platformization and AI security.

- The company delivered 16% total revenue growth in Q1, with strength across SASE, software firewalls, and XSIAM.

- Management expects this momentum to continue as enterprises consolidate point products onto unified platforms.

- SASE ARR grew 34% to $1.3 billion, outpacing independent public SASE providers.

- Software firewalls now represent 44% of product revenue, up from 38% last year, as cloud workload migration accelerates.

- The pending acquisitions of CyberArk and Chronosphere significantly expand the addressable market.

Management raised the FY 2030 NGS ARR target to $20 billion, implying sustained double-digit growth.

2. Operating margins: 30.5%

Palo Alto achieved 30.2% operating margin in Q1, marking the second consecutive quarter above 30%. This performance reflects operational leverage and disciplined cost management.

The company has deployed AI across functions, driving three consecutive quarters of case-volume reduction in customer support and eleven consecutive quarters of reduced time to resolution.

Management expects operating margins of 29.5% to 30% for fiscal 2026.

As the business scales and integrates acquisitions, there are continued opportunities for margin expansion through automation and platform efficiencies.

3. Exit P/E Multiple: 40.7x

The market values Palo Alto at 42x earnings. We assume the P/E will compress to 40.7x over our forecast period.

The near-term integration of CyberArk and Chronosphere introduces complexity. The company is balancing two major acquisitions simultaneously, which introduces execution risk.

As platformization continues to deliver sustained results and Palo Alto demonstrates the value of its expanded identity and observability offerings, the company should maintain a premium multiple.

The leadership position in AI security and quantum-safe solutions provides additional competitive moats.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Cybersecurity companies face competitive pressures and technology transitions. Here’s how Palo Alto stock might perform under different scenarios through July 2030:

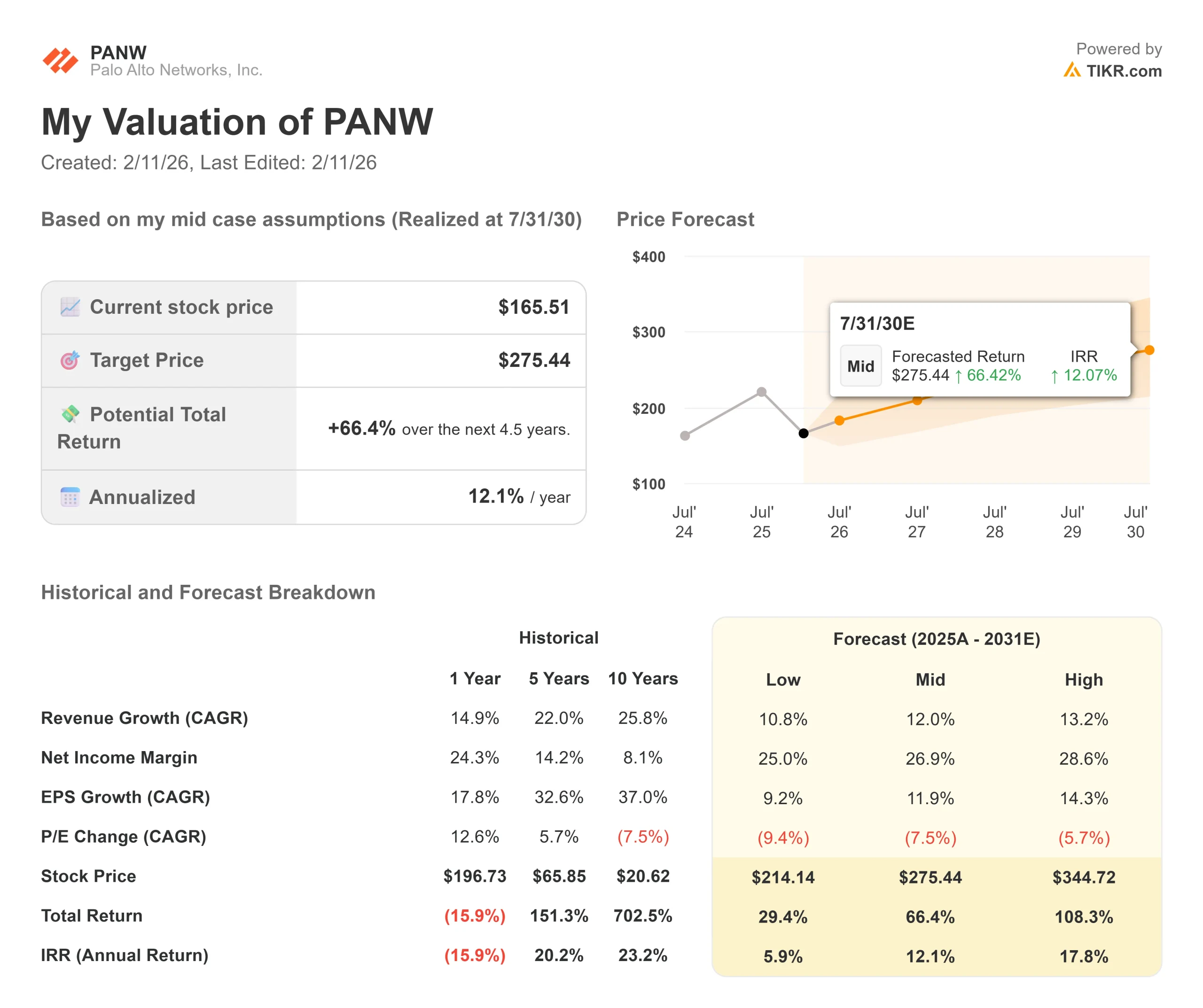

- Low Case: If revenue growth slows to 10.8% and net income margins compress to 25%, investors still see a 29% total return (6% annually).

- Mid Case: With 12% growth and 27% margins, we expect a total return of 66% (12% annually).

- High Case: If AI security and platformization accelerate to drive 13.2% revenue growth while Palo Alto maintains 29% margins, returns could hit 108% total (18% annually).

See what analysts think about PANW stock right now (Free with TIKR) >>>

The range reflects execution on platformization, successful integration of CyberArk and Chronosphere, and the company’s ability to capture emerging AI security demand.

In the low case, integration challenges slow growth or competitive pressures intensify.

In the high case, platformization accelerates faster than expected, AI security demand exceeds projections, and the company successfully democratizes identity security across its customer base.

How Much Upside Does Palo Alto Networks Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!