Key Takeaways:

- AI Infrastructure Boom: The multi-trillion-dollar AI buildout is driving unprecedented demand for advanced chip design tools.

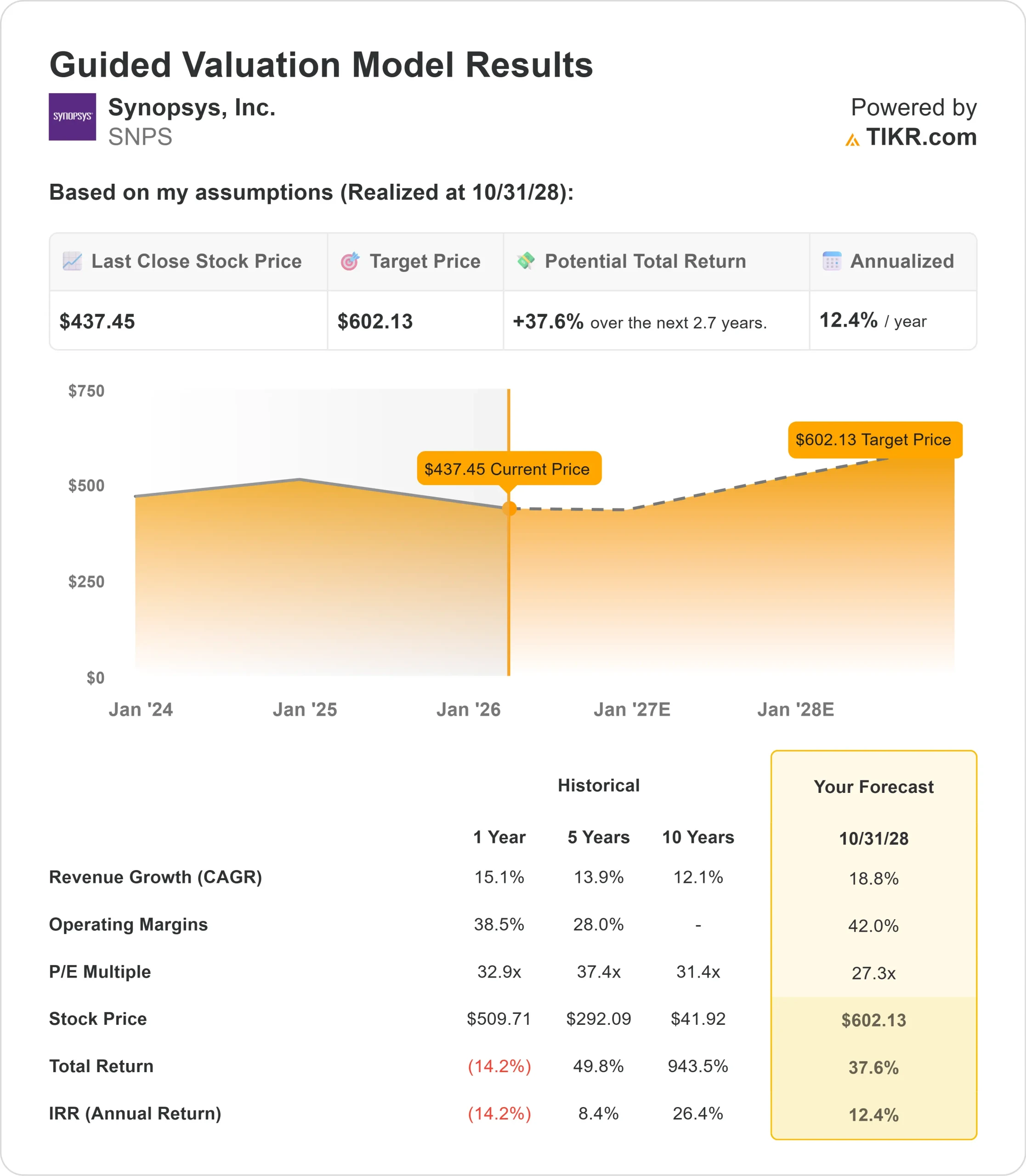

- Price Projection: Based on current execution, SNPS stock could reach $602 by October 2028.

- Potential Gains: This target implies a total return of 38% from the current price of $437.

- Annual Return: Investors could see roughly 12% growth over the next 2.7 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Synopsys (SNPS) closed fiscal 2025 with record revenue of $7.05 billion and raised its profile dramatically through the Ansys acquisition. The company exited the year with over $11 billion in backlog, reflecting strong customer commitments.

CEO Sassine Ghazi pointed to robust fundamentals across the business. The company is operating amid a massive AI infrastructure buildout that’s driving semiconductor demand, and design starts for both specialized and general-purpose compute.

- AI is revolutionizing chip design. Modern processors are being pushed to the atomic level as they scale from factories to edge devices. As AI evolves from large language models to world models, the engineering challenge isn’t just software—it’s physics.

- This complexity plays directly to Synopsys’ strengths. The company saw continued strong demand for hardware-assisted verification in Q4, driven by the increasing complexity of AI and high-performance computing. The business ended a record year with 12 competitive wins in the fourth quarter alone.

- Nearly 5,000 active users among tier-one semiconductor customers are now applying Synopsys.ai capabilities to increase engineering productivity. The company continues to advance agentic AI technology with partners such as NVIDIA and Microsoft, promising to transform workflows entirely.

- The Ansys combination transformed Synopsys from an EDA leader to the leader in engineering solutions from silicon to systems. The deal diversified revenue, expanded the customer base, and created opportunities for joint solutions that bridge the digital and physical design domains.

Management expects muted growth in the IP business for 2026 as the team works through a transitional year. China’s revenue declined 22% in fiscal 2025, and the company is taking a pragmatic view that the difficult environment persists.

Still, the long-term picture looks compelling. Synopsys is mission-critical to technology innovation at a time when complexity is accelerating, and traditional approaches are breaking down.

See analysts’ full growth forecasts and estimates for SNPS stock (It’s free) >>>

What the Model Says for Synopsys Stock

We analyzed Synopsys by examining its position as the essential enabler of AI-era chip design and its expansion into multiphysics simulation through Ansys.

The company benefits from multiple growth drivers. Hyperscalers are pursuing three parallel strategies—buying merchant chips, engaging in custom ASICs, and developing proprietary silicon.

Since Synopsys sells on a chip-start basis rather than by volume, each design represents a revenue opportunity regardless of who manufactures the final product.

Synopsys leadership in advanced node, multi-die, and AI design is driving steady demand. AWS recently launched Graviton5 using Synopsys tools, including VCS, PrimeTime, Fusion Compiler, and IC Validator—demonstrating the mission-critical nature of the platform.

The Ansys business adds diversification. Customers across industrial, automotive, and aerospace are using simulation to virtualize and optimize production, saving time and money.

At Microsoft Ignite, Microsoft partnered with NVIDIA and Krones to demonstrate how Ansys physics solvers enable real-time digital twins of production lines.

Using a forecast of 18.8% annual revenue growth and 42% operating margins, our model projects the stock will rise to $602 within 2.7 years. This assumes a 27.3x price-to-earnings multiple.

That represents compression from Synopsys’ historical P/E averages of 32.9x (one year) and 37.4x (five years). The lower multiple reflects near-term headwinds from the IP business transition and China market challenges.

The real value lies in capturing AI-driven design complexity while scaling the Ansys simulation business across industries.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SNPS stock:

1. Revenue Growth: 18.8%

Synopsys growth centers on AI-driven chip complexity and the Ansys combination. Management guided fiscal 2026 revenue to $9.61 billion at the midpoint, which includes double-digit growth from Ansys at $2.9 billion.

The core EDA business delivered approximately 8% growth in fiscal 2025, with record performance in hardware.

While China headwinds and IP business transition create near-term challenges, the company expects its first joint Synopsys-Ansys solutions in the first half of 2026.

The complexity of AI chip design continues to accelerate. Customers need new tools with multi-domain integration and new workflows for tight software-hardware co-design.

2. Operating margins: 42%

Synopsys guided non-GAAP operating margin to 40.5% at the midpoint for fiscal 2026, up approximately 320 basis points versus 2025. This expansion reflects both the inclusion of Ansys and the acceleration of cost synergies.

The company announced a 10% workforce reduction to drive efficiency and is well underway with execution.

Management maintains focus on sustainable growth and margin expansion through disciplined cost and portfolio management.

3. Exit P/E Multiple: 27.3x

The market values Synopsys at roughly 30x earnings. We assume modest compression to 27.3x over our forecast period.

Near-term uncertainty from the IP business transition and China restrictions weighs on the multiple.

The IP segment faces a transitional 2026, with muted growth, as the team repositions resources and expands critical titles for HPC customers.

As Synopsys delivers joint solutions and demonstrates the value of the combined platform, the company should command a premium multiple given its mission-critical role in AI-era innovation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

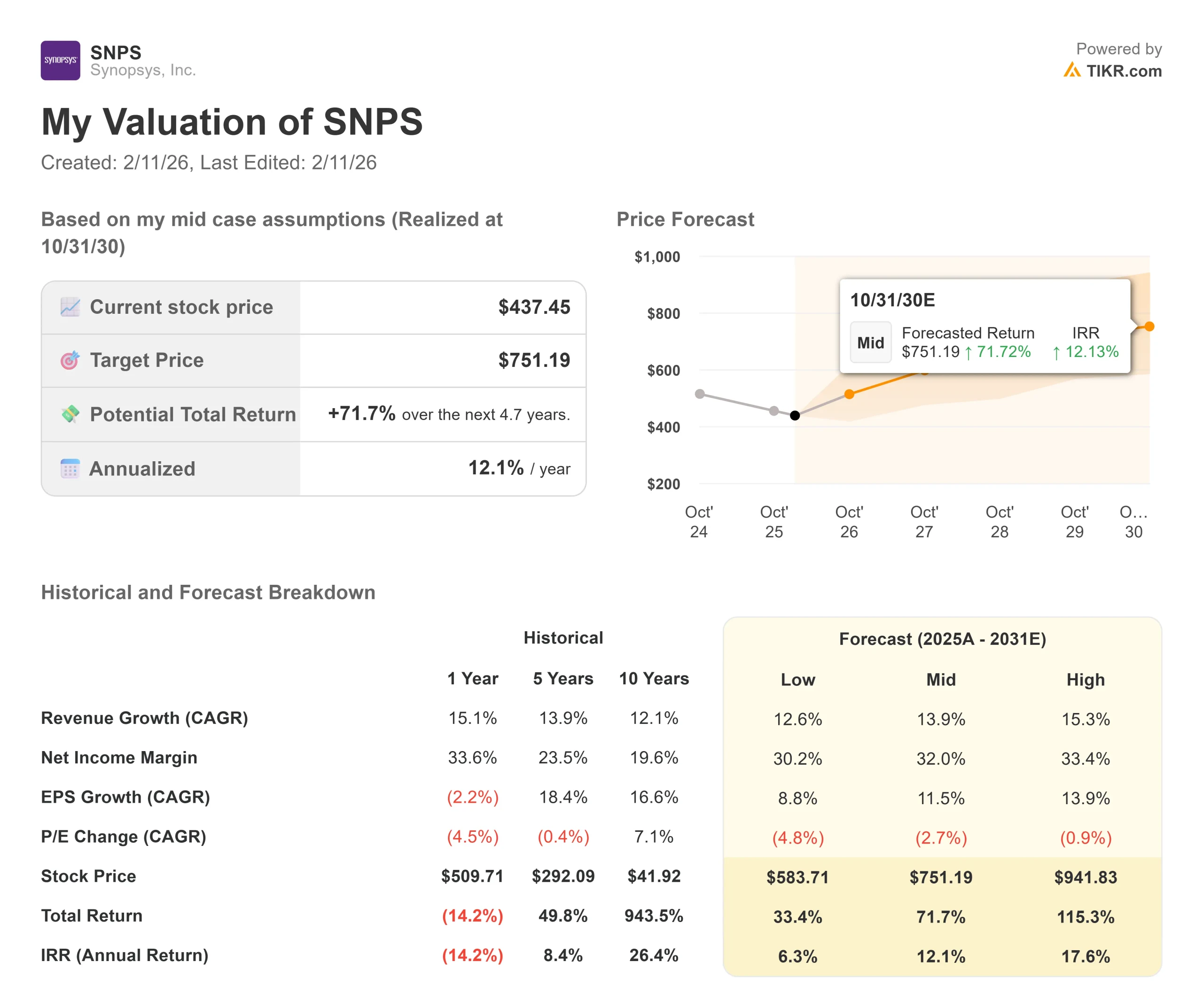

Semiconductor tool companies face technology transitions and geopolitical complexity. Here’s how Synopsys stock might perform under different scenarios through October 2030:

- Low Case: If revenue growth moderates to 12.6% and net income margins compress to 30.2%, investors still see a 33% total return (6.3% annually).

- Mid Case: With 13.9% growth and 32% margins, we expect a total return of 72% (12.1% annually).

- High Case: If AI complexity drives 15.3% revenue growth while Synopsys maintains 33.4% margins, returns could hit 115% total (17.6% annually).

See what analysts think about SNPS stock right now (Free with TIKR) >>>

The range reflects execution on joint Synopsys-Ansys solutions, successful navigation of China challenges, and the IP business returning to mid-teens growth.

In the low case, China deteriorates further, or IP recovery stalls.

In the high case, agentic AI transforms workflows faster than expected, and joint solutions command premium pricing as customers rush to solve multi-domain design challenges.

How Much Upside Does Synopsys Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!