Key Stats for Valero Energy Corporation Stock

- Past-Week Performance: ~12.1%

- 52-Week Range: $99 to $192

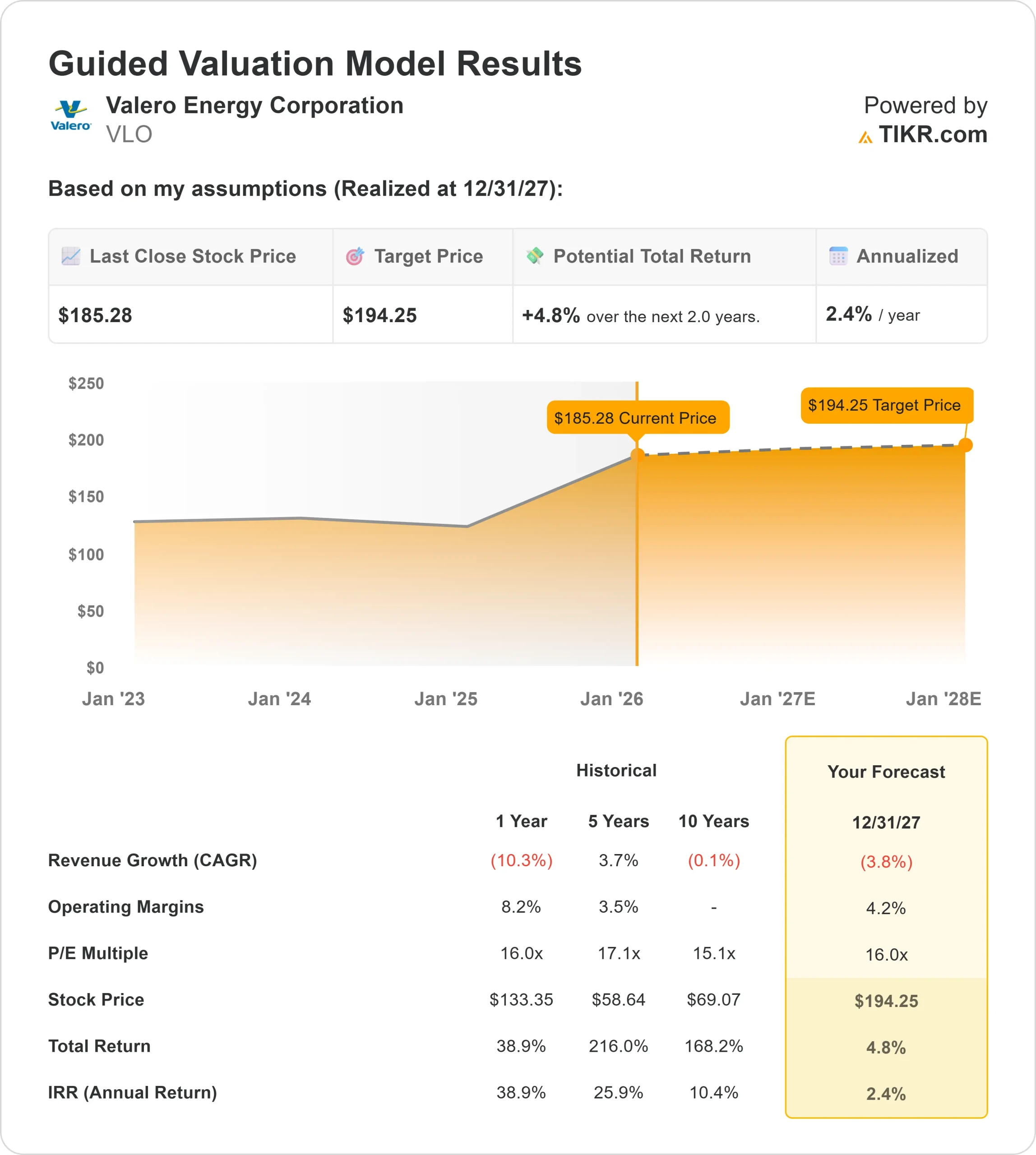

- Valuation Model Target Price: $194

- Implied Return: +4.8% over ~2.0 years

Value your favorite stocks like Valero Energy with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Valero Energy stock (VLO) rose about 12% over the past week on hopes of a regime change in Venezuela, moving toward the upper end of its recent range and briefly trading near $190, close to its 52-week highs.

During the week, Goldman Sachs reiterated a constructive view on U.S. refiners, pointing to resilient downstream margins and continued strong cash generation as reasons earnings remain more durable than expected.

While Valero’s Gulf Coast refineries are well-suited for heavy Venezuelan crude, any meaningful increase in supply would likely happen slowly and in fairly limited volumes, making it hard to justify such a sharp rally today.

Shares of other refining peers also moved higher, reinforcing that this was a sector-wide move.

See analysts’ growth forecasts and price targets for Valero Energy (It’s free) >>>

Is Valero Energy Fairly Valued?

Valero’s valuation assumes refining margins come down from recent highs but stay healthy over the next few years. Our model through 2027 is based on the following assumptions:

- Revenue growth (CAGR): -3.8%

- Operating margins: 4.2%

- Exit P/E multiple: 16.0x

Based on these inputs, the model estimates a target price of $194, implying a +4.8% total return from the current share price of $185, or about 2.4% per year over the next two years.

What ultimately drives results over the next 12 months is whether Valero can keep margins closer to current levels than the model assumes, especially through the spring and summer driving season when gasoline demand typically strengthens.

Gasoline and distillate crack spreads matter most, because even small changes flow directly into earnings and free cash flow given Valero’s scale and high utilization rates.

Operational execution adds another layer, as disciplined maintenance timing, steady throughput, and access to advantaged feedstocks lift per-barrel profitability without requiring higher fuel prices.

When these factors hold together, free cash flow stays strong enough to support buybacks and dividends, which helps explain why the stock continues to trade closer to cycle highs despite conservative long-term assumptions.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>