Key Takeaways:

- Integrated Utility Scale: Enel operates one of Europe’s largest regulated utility platforms across power generation, grids, and renewables, supporting predictable cash flows across €78 billion in annual revenue.

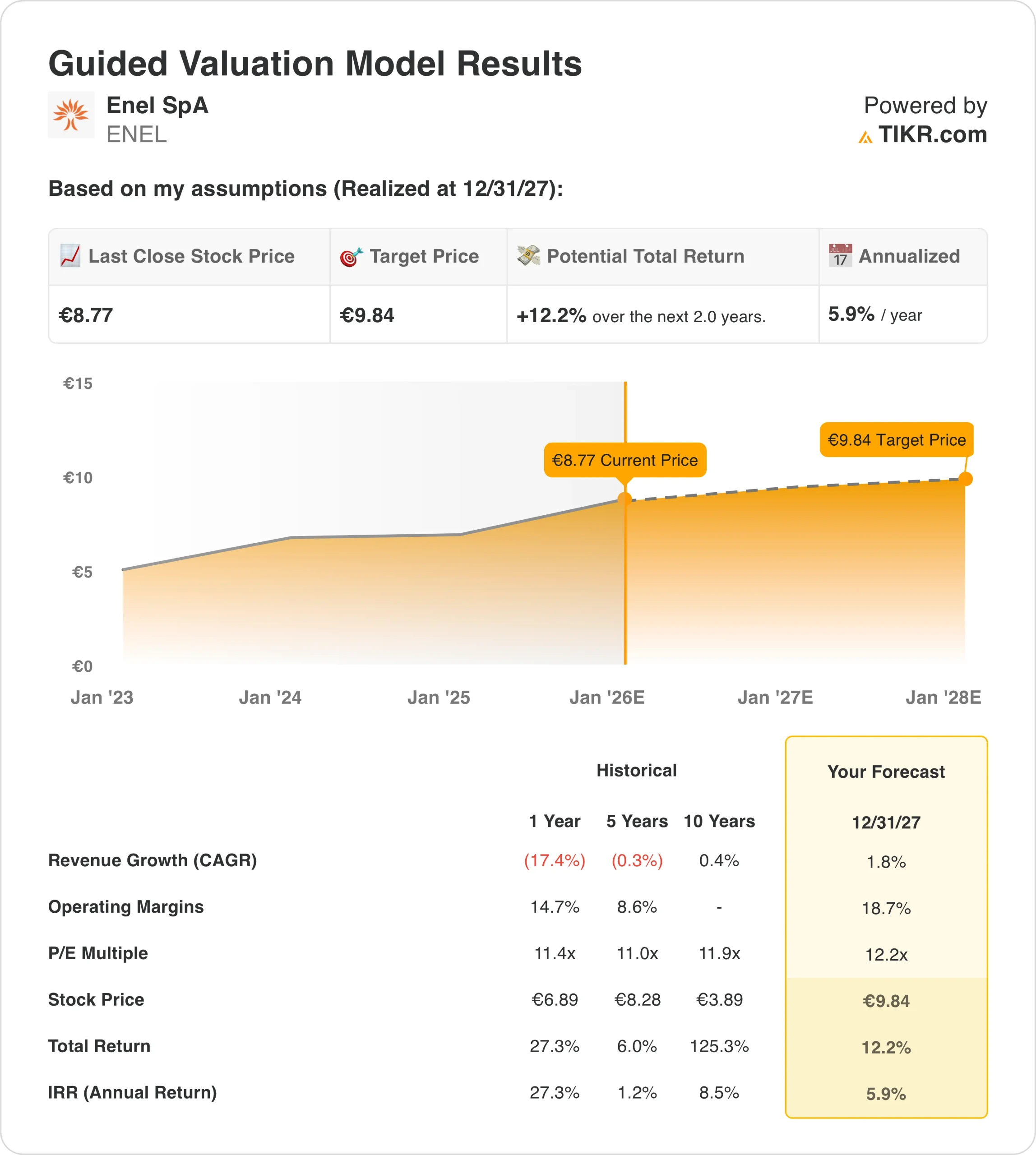

- Price Projection: Based on our valuation assumptions, Enel shares could reasonably reach €10 by December 2027.

- Potential Gains: This implies total returns of around 12% from the current price of around €9.

- Annual Return: That outcome translates to roughly 6% annualized returns over the next 2 years.

Enel SpA (ENEL) operates one of the world’s largest integrated electricity and gas platforms, spanning renewables, regulated grids, and end-user markets, with diversified exposure across Europe and Latin America supporting stable cash generation.

In December 2025, Enel approved up to €2 billion in hybrid bond issuance and acquired two German wind farms for €80 million, strengthening capital flexibility while adding 50 MW of contracted renewable capacity.

Over the last twelve months, Enel generated €78 billion in revenue, reflecting normalized energy pricing but stable demand across regulated networks and renewable generation portfolios.

EBIT reached roughly €14 billion over the last twelve months which reflects consistent operating performance as regulated returns and renewable contracts offset volatility in merchant power markets.

Operating margins expanded to roughly 18%, supported by grid investments, cost discipline, and a higher share of regulated and long-term contracted assets.

Despite steady profits and improving earnings quality, Enel trades near 12 times forward earnings, raising questions about whether the market is fully pricing in cash flow stability and dividend visibility.

What the Model Says for ENEL Stock

We analyzed Enel’s valuation using its regulated utility positioning, expanding renewables base, stable cash flows, and capital discipline supporting consistent shareholder returns.

The model assumes 1.8% annual revenue growth, 18.7% operating margins, and a normalized exit P/E multiple of 12.2x.

Based on these inputs, Enel stock could reach €9.84 per share by 2027 as earnings compound steadily and dividends support total returns.

This implies a 12.2% total return from €9, equivalent to a 6% annualized return over the next 2 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ENEL stock:

1. Revenue Growth: 1.8%

Enel’s revenue base normalized after the 2022 energy price spike, with LTM revenue at €77.8B following a multi-year period of volatility.

Recent revenue declines of 17.4% in 2024 and 0.1% in 2025 reflect normalization rather than structural demand erosion across regulated and renewables-heavy operations.

Forward estimates show revenues stabilizing and gradually recovering from €78.9B in 2025 to €82.7B by 2027 as renewable capacity additions offset price pressure.

The German wind acquisition adds approximately €10M in annual EBITDA under protected pricing which reinforced an incremental growth visibility without relying on merchant exposure.

Growth is constrained by market maturity in core European regions and deliberate portfolio optimization, prioritizing returns over volume expansion.

Revenue growth is modeled at 1.8% annually by market consensus to reflect normalization pressures offset by continued renewables build-out and stability from the regulated asset base.

2. Operating Margins: 18.7%

Enel’s operating margin expanded to 18.1% LTM, recovering from a 7.8% trough in 2022 during peak energy cost dislocations.

Historical EBIT margins averaged around 8-9% over five years, masking recent structural improvements from portfolio simplification and renewables mix.

EBIT margins reached 18.7% in 2024 as cost discipline, grid returns, and higher renewable contribution offset softer pricing.

EBITDA margins near 29% reflect Enel’s increasing exposure to regulated networks and contracted renewable generation.

Margin sustainability is supported by feed-in premiums, regulated returns, and reduced exposure to volatile thermal generation.

Downside risk stems from regulatory resets and inflation-linked operating costs, limiting further margin expansion beyond current levels.

Operating margins are assumed at 18.7%, capturing post-restructuring normalization while recognizing limited margin upside within a mature utility footprint.

3. Exit P/E Multiple: 12.2x

Enel trades near 12× forward earnings and 13×–15× trailing earnings which is very consistent with an income-oriented investor base and limited growth expectations.

The market values Enel closer to regulated utility peers rather than high-growth renewables developers, capping multiple expansion potential.

The stock’s dividend yield of above 5.5% will help to give investors stable returns.

Upside to valuation depends on sustained earnings delivery and regulatory predictability rather than cyclical or sentiment-driven expansion.

The valuation applies a 12.2× exit multiple, supported by durable cash generation and dividends, but capped by utility-like growth expectations.

What Happens If Things Go Better or Worse?

European utility outcomes depend on regulation, capital costs, and execution across grids and renewables. Here is how Enel might perform in different scenarios through 2027.

- Low Case: If the European power demand remains soft and financing costs stay elevated, revenue grows around 5%, net income margins settle near 7%, and valuation contracts modestly → 0% annual returns.

- Mid Case: If electricity demand remains stable and grid investments proceed as planned, revenue grows about 6%, margins hold near 8%, and valuation remains stable, → 5% annual returns.

- High Case: If renewable expansion executes smoothly and regulatory conditions remain supportive, revenue growth improves toward 6%, margins approach 8%, and valuation expands modestly → 9% annual returns.

Enel is operating in a more predictable earnings phase shaped by regulated assets and long-term contracts.

A €10 share price by 2027 is achievable if margin stability holds and valuation remains aligned with normalized utility earnings rather than macro uncertainty.

How Much Upside Does Enel Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!