Key Takeaways:

- Transformation Progress: PayPal has shifted from negative transaction margin growth to 6-7% growth in 2025.

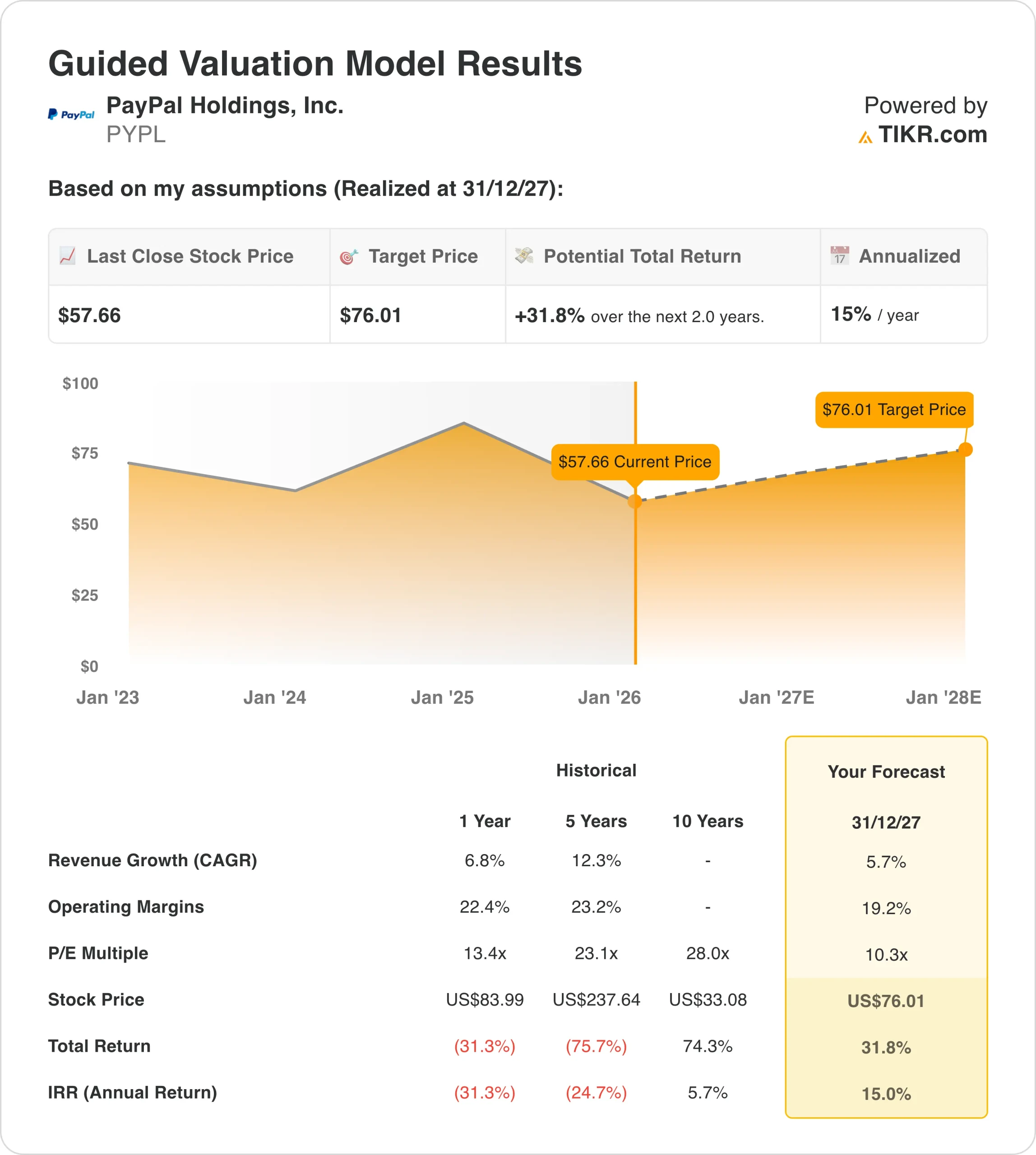

- Price Projection: Based on current momentum, the stock could hit $76 by December 2027.

- Potential Gains: This target implies a total return of 32% from the current price of $57.66.

- Annual Return: Investors could see roughly 15% growth per year over the next 24 months

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

PayPal (PYPL) is in the middle of a turnaround that’s starting to show real results. After years of stagnant growth and pressure from fintech competitors, CEO Alex Chriss has spent the past two years rebuilding the company’s foundation.

In Q3 of 2025, transaction margin dollars grew 7% excluding interest income, a sharp reversal from negative growth just two years ago. Revenue is accelerating, and the company is on track to deliver at least 15% earnings-per-share growth this year.

Despite these improvements, PYPL stock is down 31% over the past year and over 80% from all-time highs.

The market hasn’t fully priced in the company’s transformation into a profitable growth machine. This disconnect creates an opportunity for patient investors willing to bet on PayPal’s execution.

See analysts’ full growth forecasts and estimates for PayPal stock (It’s free) >>>

What the Model Says for PayPal Stock

We analyzed PayPal’s future by focusing on three key shifts: the company’s push into buy-now-pay-later, Venmo’s monetization ramp, and the rollout of agentic commerce through AI partnerships with OpenAI and Google.

Using conservative assumptions of 5.7% annual revenue growth and 19.2% operating margins, our model projects the stock will reach $76 within two years. This assumes a 10.3x price-to-earnings multiple at exit.

That valuation might seem low compared to PayPal’s historical average of 28x over the past decade. But it reflects the company’s shift from a pure growth story to a more mature, profitable business.

The 10.3x multiple is roughly in line with the current market valuation, making it a reasonable base case.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PayPal stock:

1. Revenue Growth: 5.7%

PayPal’s growth has slowed from double-digit rates, but there are clear signs of stabilization. The company is winning in several high-growth areas:

Buy Now, Pay Later (BNPL): Volume is growing over 20% each quarter, putting PayPal on track for nearly $40 billion in BNPL transactions in 2025. The Net Promoter Score for this product sits at 80, indicating strong customer satisfaction. PayPal plans to move BNPL “upstream” by showing payment options earlier in the shopping journey, which should accelerate adoption.

Venmo’s Inflection: After years of promise without profit, Venmo is finally delivering. The platform is on pace to generate $1.7 billion in revenue this year, up 20% from two years ago. More importantly, only 5-10% of Venmo’s users currently use the debit card or Pay with Venmo features. Accounts that adopt these products generate 4x higher revenue per user.

Omnichannel Expansion: PayPal Everywhere launched in September 2024 to move beyond online checkout. The strategy is working, given that U.S.-branded experiences volume grew 10% in Q3, double the growth rate from a year ago. Debit card and tap-to-pay spending jumped 65% year-over-year.

2. Operating margins: 19%

PayPal has made significant progress in improving profitability. The company turned around its money-losing payment processing business by renegotiating contracts with large merchants and focusing on value-added services like payouts and fraud protection.

The current EBIT margin of 18.4% over the past twelve months demonstrates operational efficiency. Our forecast of 19.2% assumes modest margin expansion as higher-margin products like BNPL and Venmo grow as a percentage of total revenue.

Management indicated they’ll invest more heavily in 2026 to win market share in BNPL and agentic commerce. These investments will pressure margins in the near term but should pay off with faster revenue growth over time.

3. Exit P/E Multiple: 10x

Our exit multiple of 10.3x reflects several considerations:

Slower Growth Profile: PayPal is no longer a hypergrowth fintech. Revenue growth in the mid-single digits commands a lower multiple than the 20%+ growth rates PayPal posted in earlier years.

Macro Headwinds: Management noted pressure on consumer discretionary spending, particularly among middle and lower-income customers. This weakness showed up in September and persisted through October, creating uncertainty about holiday spending.

Multiple Expansion Opportunity: If PayPal successfully scales BNPL and Venmo while maintaining profitability, the stock could command a higher multiple. But we’re staying conservative until the company demonstrates consistent execution.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

PayPal’s transformation is still in progress, and outcomes could vary widely depending on execution and macro conditions. Here’s how different scenarios might play out through 2029:

- Low Case: If consumer spending remains weak and PayPal’s growth initiatives take longer than expected, revenue growth could slow to 4.9% annually. Combined with margin compression to 14.1%, the stock would still deliver a 17% total return, or about 4% annually.

- Mid Case: Our base case assumes 5.5% revenue growth and 15.1% margins. This scenario delivers a 47% total return over two years, or 10% annually. This is the most likely outcome if management executes on the plan.

- High Case: If BNPL takes off faster than expected and Venmo monetization accelerates, revenue growth could reach 6% with margins expanding to 16%. A higher growth profile would deliver 79% total returns over four years, or about 16% annually.

See what analysts think about PayPal stock right now (Free with TIKR) >>>

The range of outcomes is relatively narrow, reflecting PayPal’s position as a mature company with multiple growth drivers. Unlike a single-product startup, PayPal has diversified revenue sources that reduce risk.

PayPal has moved from a crisis to a credible turnaround. The company is growing transaction margins, scaling new products like BNPL and Venmo, and positioning itself for the AI-driven commerce shift.

Trading at 10.3x earnings with improving fundamentals, the stock offers a reasonable risk-reward for investors who believe in the transformation.

How Much Upside Does PayPal Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!