Key Takeaways:

- Telehealth Evolution: Hims & Hers is expanding beyond stigmatized conditions to offer proactive health management, including diagnostics, weight-loss support, and hormone health.

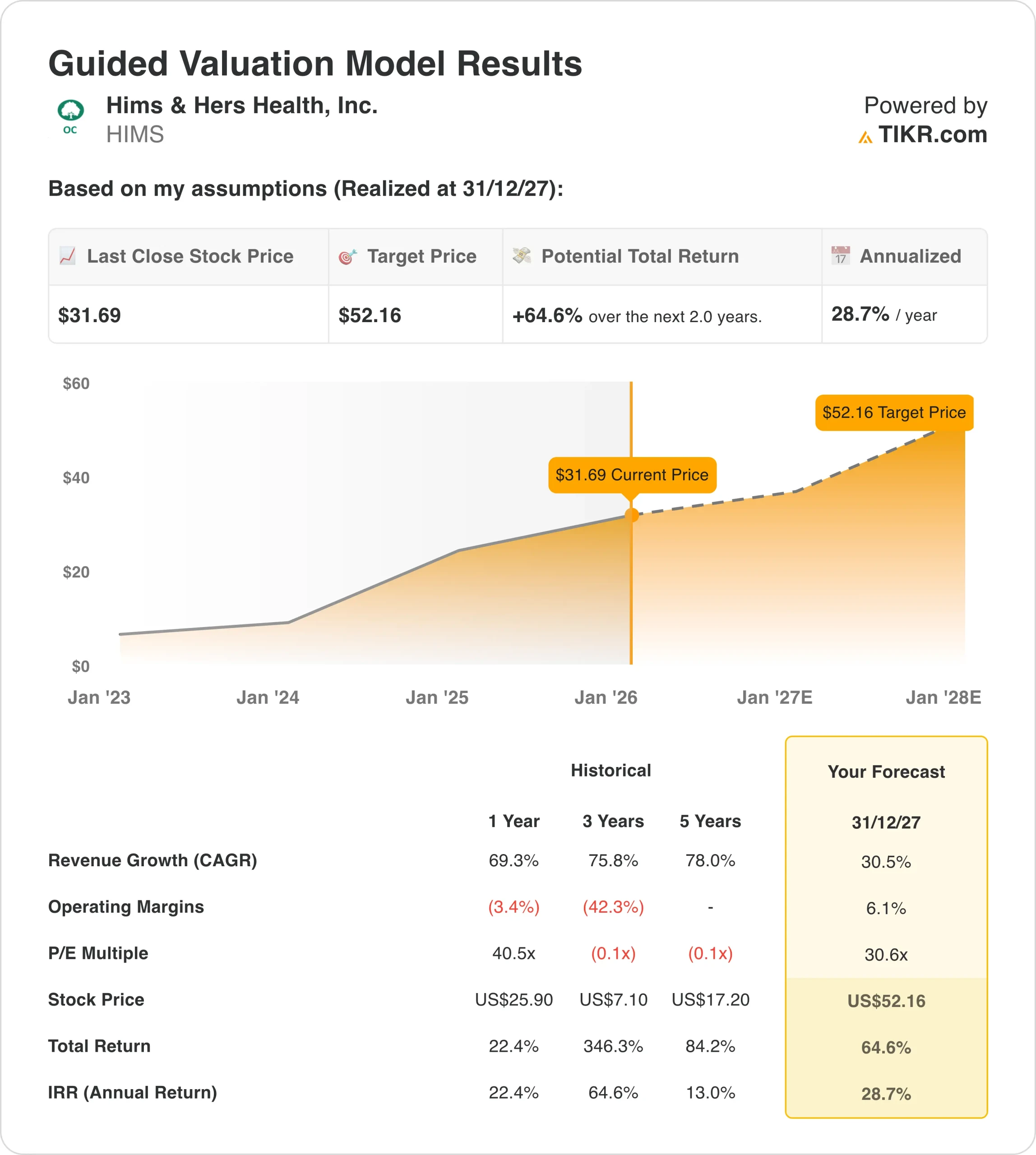

- Price Projection: Based on the current trajectory, the stock could reach $52 by December 2027.

- Potential Gains: This target implies a total return of 65% from the current price of $32.

- Annual Return: Investors could see roughly 29% growth per year over the next 2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Hims & Hers (HIMS) is building a comprehensive consumer health platform that’s changing how millions access personalized care.

With Q3 revenue hitting $600 million (up 49% year-over-year) and ambitious plans to reach $6.5 billion by 2030, the company is executing on a vision that goes far beyond its stigmatized-condition roots.

The numbers validate the strategy.

- Subscribers using personalized solutions grew 50% year-over-year.

- The Hers brand is on track to reach $1 billion in annual revenue by 2026.

- Weight-loss offerings are on track to reach $725 million this year.

- The company just expanded its footprint to 200 million adults across five European countries through the Zava acquisition.

Despite raising guidance and launching into new categories like testosterone, menopause, and diagnostics, HIMS stock is trading at $32, creating an opportunity for investors who grasp the platform’s expansion potential.

See analysts’ full growth forecasts and estimates for HIMS stock (It’s free) >>>

What the Model Says for HIMS Stock

We analyzed Hims & Hers through the lens of its platform-expansion and margin-improvement journey.

By transitioning from acute-condition treatment to proactive health management while verticalizing operations, the company is positioned to sustain high growth while improving profitability.

Using a forecast of 30.5% annual revenue growth and 6.1% operating margins, our model projects the stock will rise to $52 within 2 years. This assumes a 30.6x Price-to-Earnings (P/E) multiple.

The company’s premium valuation reflects its exceptional growth profile and the massive addressable market for direct-to-consumer healthcare.

As operations scale and margins expand, this multiple should hold.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for HIMS stock:

1. Revenue Growth: 30.5%

Hims & Hers has multiple growth engines firing simultaneously, reducing reliance on any single category.

Weight Loss Expansion: The company reduced compounded GLP-1 prices by up to 20% in Q4, extending accessibility. Management expects weight loss revenue of at least $725 million in 2025. The verticalization of sterile compounding facilities is establishing what management calls “a new gold standard” for quality and affordability.

New Specialty Launches: Testosterone and menopause offerings are showing immediate product-market fit. Nearly 1.3 million women enter menopause annually in the U.S., yet only 30% of OB/GYN programs offer formal training on treatment. The Hers brand now has four distinct growth engines across dermatology, weight loss, hormone health, and soon diagnostics.

International Expansion: The Zava acquisition provides infrastructure across the U.K., Germany, France, Ireland, and Spain. Canada launches soon, with access to generic semaglutide planned for 2026. Management sees international markets representing over $1 billion in potential annual revenue.

2. Operating margins: 6.1%

Hims & Hers’ margin profile reflects heavy investment in future capabilities while demonstrating improving unit economics.

Verticalization Payoff: The company entered 2025 with 400,000 square feet of facility space and expects to exit 2025 with over 1 million square feet. This expansion unlocks new form factors like gummies, increases sterile fulfillment capacity, and enables margin expansion through vertical integration.

Marketing Efficiency: Marketing as a percentage of revenue was 39% in Q3, representing over 6 points of leverage year-over-year. Higher retention from personalized offerings and acquisition gains through lower-cost channels are driving leverage as revenue growth outpaces marketing investment.

Strategic Investment Phase: Management expects a “temporary pause in year-over-year margin expansion” through 2026 as the company invests in new specialties, international markets, and technology capabilities. This mirrors the 2023 investment period that preceded rapid margin expansion.

3. Exit P/E Multiple: 30.6x

The market values Hims & Hers at 30.6x earnings today. We maintain this multiple, given the company’s growth trajectory.

Hypergrowth Premium: The company is growing revenue by 49% year-over-year while expanding into massive markets such as weight loss, hormone health, and diagnostics. Few healthcare companies combine this growth rate with improving unit economics.

Platform Transformation: The shift from stigmatized conditions to proactive health management significantly expands the addressable market. Comprehensive lab testing launches before year-end, followed by a longevity specialty in 2026 featuring peptides, coenzymes, and metabolic treatments.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

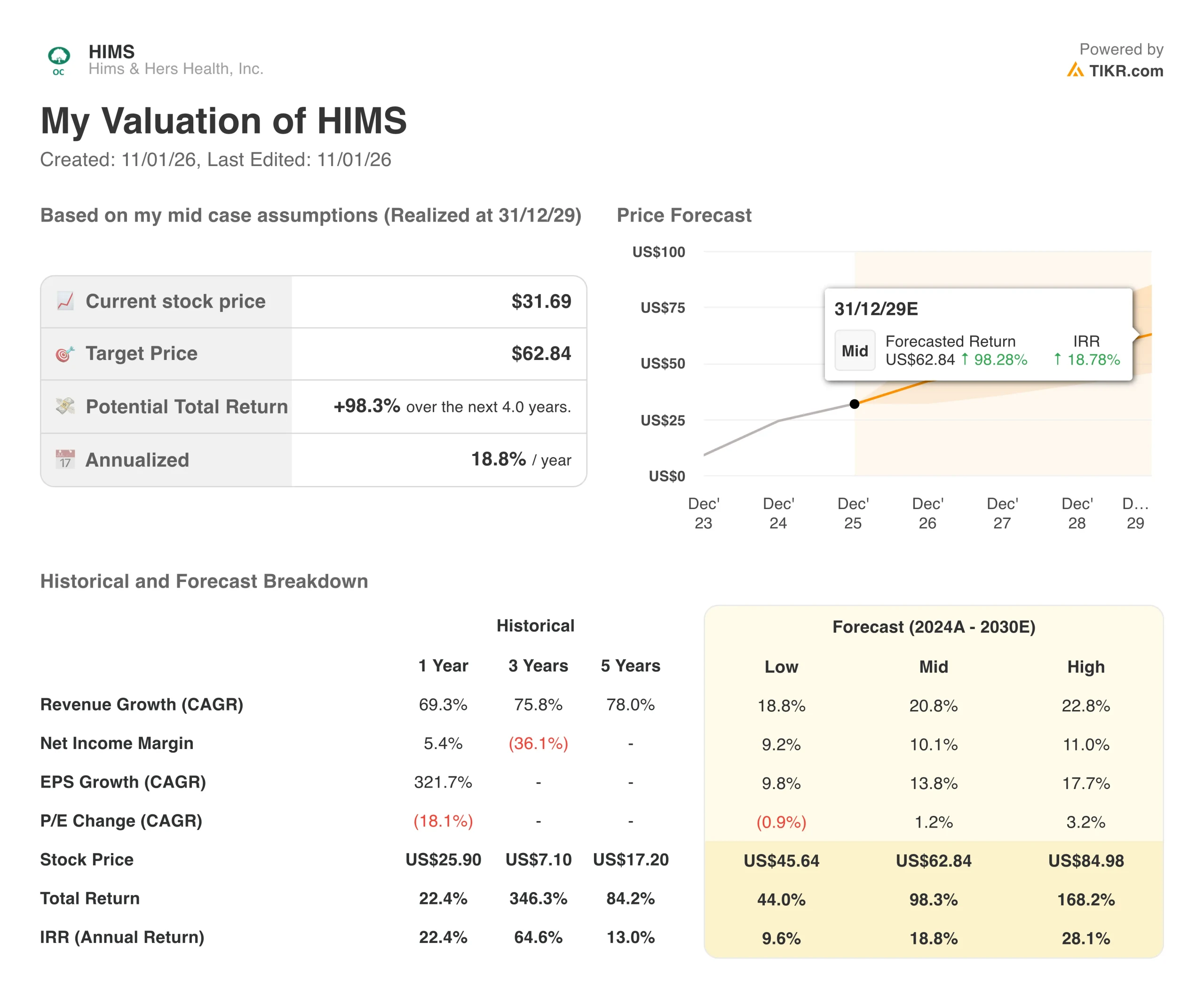

Telehealth platforms face regulatory risk and execution challenges in new categories. Here is how Hims & Hers stock might perform in different scenarios through 2029:

- Low Case: If revenue growth slows to 18.8% and margins compress to negative territory at -4.1%, the stock still offers a 10% annual return.

- Mid Case: With 30.5% growth and 6.1% margins (our base assumptions), we expect a 19% annual return.

- High Case: If execution remains strong and the company captures 11% margins while growing at 22.8%, returns could hit 28% annually.

See what analysts think about HIMS stock right now (Free with TIKR) >>>

The range reflects different execution scenarios. In the low case, new specialty launches disappoint, or regulatory headwinds intensify around compounded medications. In the high case, verticalization benefits materialize faster, and international expansion exceeds expectations.

How Much Upside Does HIMS Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!