Key Stats for Costco Wholesale Stock

- Current Price: ~$995 (May 28, 2026)

- Q3 FY2026 EPS: $4.93, +15% YoY

- Q3 FY2026 Net Sales: $69.15B, +11.6% YoY

- Q3 FY2026 Comparable Sales (ex-gas, ex-FX): +6.6%

- Q3 FY2026 Membership Fee Income: $1.37B, +10.7% YoY

- Q3 FY2026 Digitally Enabled Comparable Sales: +21.5% YoY

- TIKR Model Price Target: ~$1,409

- Implied Upside: ~42%

Costco Stock Delivers Record Gas Volumes and 15% EPS Growth as Value Thesis Strengthens

Costco Wholesale (COST) posted Q3 fiscal 2026 earnings of $4.93 per diluted share on May 28, up 15% from $4.28 a year earlier, as record-breaking gas volumes and broad-based merchandise strength drove the warehouse retailer’s strongest traffic performance in recent memory.

The gas business was the quarter’s defining story: every one of the three four-week fiscal periods set successive all-time company volume records, and the final five weeks became Costco’s top five volume weeks ever as Middle East tensions pushed gas prices sharply higher.

Net income reached $2.192 billion for the 12 weeks ending May 10, while total revenue including membership fees climbed to $70.53 billion against a Street consensus of $69.5 billion, a beat of approximately 1.5%.

Ron Vachris, President and CEO, stated on the Q3 2026 earnings call that “our focus is providing quality goods and services at the lowest possible price continues to resonate strongly with our members,” adding that the gas crisis introduced thousands of first-time gas station users who, historically, go on to spend more across the warehouse and renew at higher rates.

The membership engine continued to compound underneath the headline: paid executive memberships hit 41.2 million, up 9.6% year over year, with China launching its executive tier this quarter and seeing adoption ahead of management’s expectations.

Comparable sales of 9.8% company-wide (6.6% adjusted for gas inflation and foreign exchange) reflected demand that extended well beyond fuel: fresh comps were up high single digits led by meat and bakery, non-foods comps were also up high single digits with gold and jewelry, health and beauty, and small appliances as standouts, and ancillary business comps surged mid-20s with pharmacy leading on GLP-1 drug demand and the inclusion of Wegovy and Ozempic in the member prescription program.

Digitally enabled comparable sales grew 21.5% in the quarter, supported by a 37% increase in site and app traffic, while personalized product recommendation carousels delivered conversion rates three times better than standard Costco benchmarks and contributed just under $500 million of e-commerce sales.

The company also advanced its AI search strategy in Q3, recording triple-digit growth in AI-generated site traffic, which carries the highest conversion rate of all traffic sources to Costco.com, as the company updated product pages to surface the full value proposition (delivery, installation, haul-away pricing) to large language models.

Capital expenditure for the quarter was $1.41 billion, with full-year CapEx guidance of approximately $6.5 billion supporting an accelerated warehouse pipeline, depot network expansion, and digital infrastructure, as management targets 30-plus net new openings annually in the coming years.

Costco Q3 2026 Financials: SG&A Leverage Holds as Gas Mix Compresses the Reported Gross Margin

Costco’s net sales of $69.15 billion for the 12 weeks ending May 10 represented an 11.6% increase from $61.96 billion in Q3 2025, continuing a streak of quarter-on-quarter acceleration visible in the trailing income statement: revenue growth has tracked at 8%, 8.1%, 8.3%, and now 9.2% and 11.6% in the two most recent periods, reflecting the combined tailwind from gas price inflation and underlying merchandise momentum.

The reported gross margin rate of 11.04% came in 21 basis points below Q3 2025’s 11.25%, but excluding gas inflation, the rate was flat to marginally positive at plus 1 basis point, with core-on-core merchandise margins down only 9 basis points as Costco deliberately invested lower prices in eggs, beef, and several Kirkland Signature everyday items while cycling a large prior-year LIFO charge.

Operating income reached $2.53 billion in Q3, up 15.2% from $2.20 billion in Q3 2025, continuing the trajectory of operating income growth accelerating ahead of revenue growth across the past six quarters (11.1%, 9.4%, 10.7%, 12.3%, 15.2% year over year in sequence).

SG&A of 8.96% improved 20 basis points year over year (better by 2 basis points excluding gas inflation), though underlying operations leverage of roughly mid-single-digits was partially offset by higher healthcare costs and a pair of legal settlements in the central segment, items CFO Gary Millerchip characterized as non-recurring.

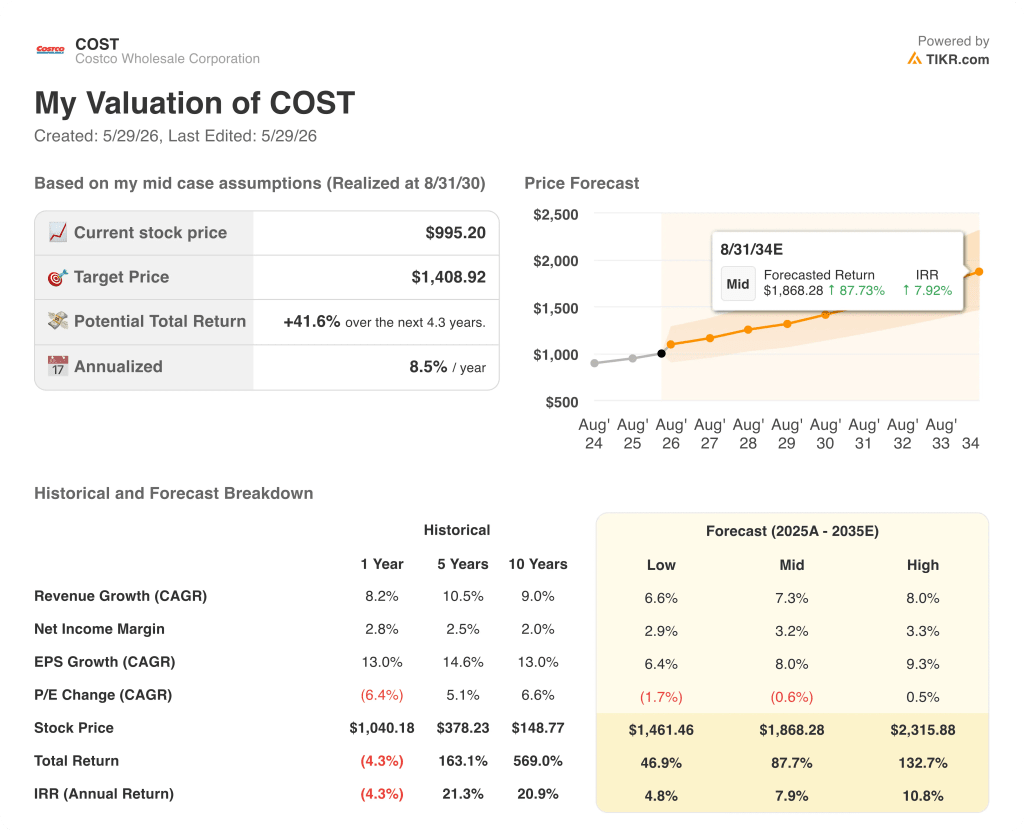

Is Costco Stock Undervalued? What the TIKR Model Says at $995

TIKR’s base case values Costco stock at approximately $1,409 by August 2030, implying around 42% total return from the current price of approximately $995, or roughly 9% annualized over 4 years.

If Costco sustains revenue growth in the 7% range with net income margins expanding modestly toward 3.2%, the mid-case path reaches approximately $1,409 by August 2030 at around 8% annualized.

A more conservative scenario, where revenue CAGR holds closer to 6.6% and margins stay nearer to 2.9%, still produces a stock price of approximately $1,461 by August 2030, or roughly 5% annualized, reflecting the business’s structural floor.

If executive membership penetration, the AI-driven e-commerce acceleration, and international warehouse density compound at the high end of management’s framework, the model reaches approximately $2,316 by August 2034 at around 11% annualized.

How Did Costco Perform in Q3 2026 Earnings?

Costco delivered EPS of $4.93 in Q3 fiscal 2026, beating the $4.91 Street consensus by approximately $0.02 and growing 15% from $4.28 a year earlier.

Total revenue of $70.53 billion topped the $69.5 billion estimate by roughly 1.5%, while net sales of $69.15 billion grew 11.6% year over year.

Record-breaking gas volumes across all three four-week fiscal periods, combined with high-single-digit non-food and fresh merchandise comps, drove the outperformance.

Membership fee income of $1.373 billion rose 10.7% year over year, with the worldwide renewal rate holding steady at 89.7%.

Is Costco Stock Undervalued in 2026?

TIKR’s base case values Costco stock at approximately $1,409 by August 2030, implying around 42% total return from the current price of approximately $995, or roughly 9% annualized.

Costco’s operating income has grown between 9% and 15% in each of the past six consecutive quarters, providing consistent evidence that the business is compounding faster than the top line alone suggests.

The key variable is membership density: if paid executive memberships (up 9.6% year over year in Q3) continue outpacing total paid member growth, the implied revenue-per-member trajectory supports the base case; sustained deceleration would pressure it.

Should You Invest in Costco Wholesale Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Costco Wholesale Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Costco Wholesale Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze COST stock on TIKR for Free →