Key Stats for Vertiv Stock

- 52-Week Range: $107 to $380

- Current Price: $301

- Street Mean Target: $377

- Street High Target: $500

- Analyst Consensus: 18 Buys, 4 Outperforms, 3 Holds, 1 Underperform

- TIKR Model Target (Dec. 2030): $421

Vertiv Stock Beats Q1 Estimates and Raises Guidance — The EMEA Recovery Is Just Starting

Vertiv Holdings Co (VRT), the global critical infrastructure provider that supplies power management, thermal management, and IT systems to AI data centers, delivered first-quarter 2026 net sales of $2.65 billion, up 30% year over year, while raising its full-year outlook for the second consecutive period.

The Americas was the engine.

Americas organic growth came in at 44%, driving $1.81 billion in segment revenue and carrying adjusted operating profit of around $490 million for the quarter.

Adjusted diluted EPS of $1.17 exceeded prior guidance by $0.19 and grew around 83% year over year.

Adjusted free cash flow reached around $653 million in Q1, up approximately 147% from the prior year, supported by operating profit growth and working capital improvement that left net leverage at a near-zero 0.2x.

The company raised full-year 2026 guidance, now projecting net sales at the midpoint of around $13.75 billion, adjusted EPS at the midpoint of $6.35, and adjusted operating profit at the midpoint of around $3.2 billion, which represents around 53% growth versus 2025.

The story investors have been waiting on is EMEA.

Management expressed growing conviction that the region, down 29% organically in Q1 due to soft orders in mid-2025, is approaching an inflection, with pipeline generation accelerating and bookings through Q1 that leadership described as strong.

CEO Gio Albertazzi was direct about the setup and clarified at the Q1 2026 earnings call: “The spring continues to uncoil. We are seeing improving market sentiment throughout the quarter with momentum building.”

The May 2026 Investor Conference reinforced what the earnings call introduced, with Chief Product and Technology Officer Scott Armul detailing a multi-path architecture evolution across power and thermal that positions Vertiv as the only supplier with end-to-end portfolio coverage as rack densities march toward 600 kilowatts and eventually one megawatt.

Vertiv has also been moving rapidly on acquisitions, closing BMarko Structures in April 2026 to add structural fabrication capacity for converged infrastructure deployments, acquiring Strategic Thermal Labs for cold-plate and server-side liquid cooling expertise, and announcing ThermoKey to extend its heat rejection portfolio.

The buildout is deliberate.

Vertiv stock has more than doubled year to date, yet the current price still sits roughly 20% below the Street mean target, and the gap to TIKR’s model is wider still.

Analysts Are Near-Unanimous on VRT Stock — The Forward EBITDA Trajectory Is Why

The analyst community has rarely been this aligned on Vertiv stock.

Of 26 analysts covering VRT, 22 carry a buy or outperform rating, 3 hold neutral positions, and 1 carries an underperform, producing a mean target of $377 against the current price near $301.

The forward EBITDA trajectory is what drives that conviction.

Actuals from the most recent quarter show EBITDA of around $580 million on revenue of $2.65 billion, with EBITDA margins at around 22%.

The consensus estimate for the June 2026 quarter projects EBITDA of around $760 million, a year-over-year increase of approximately 47%.

The December 2026 quarter estimate reaches around $1.09 billion in EBITDA, implying margins of around 27%, which would represent roughly 560 basis points of expansion relative to the comparable year-ago period.

The operating leverage story is not theoretical.

Vertiv delivered around 430 basis points of adjusted operating margin expansion in Q1 to reach 20.8%, and management guided full-year 2026 adjusted operating margins to around 23.3%, up around 290 basis points from 2025.

The mechanism behind the leverage is clear: higher volumes, productivity gains, and favorable price-cost execution, including the partial absorption of tariff headwinds the company says it has already largely mitigated.

The EMEA recovery embedded in second-half guidance adds another layer.

If EMEA returns to year-over-year growth as management guided, the second half should see further volume leverage that underpins the full-year margin target without requiring any acceleration in Americas, which management is already guiding to high-30s organic growth for the year.

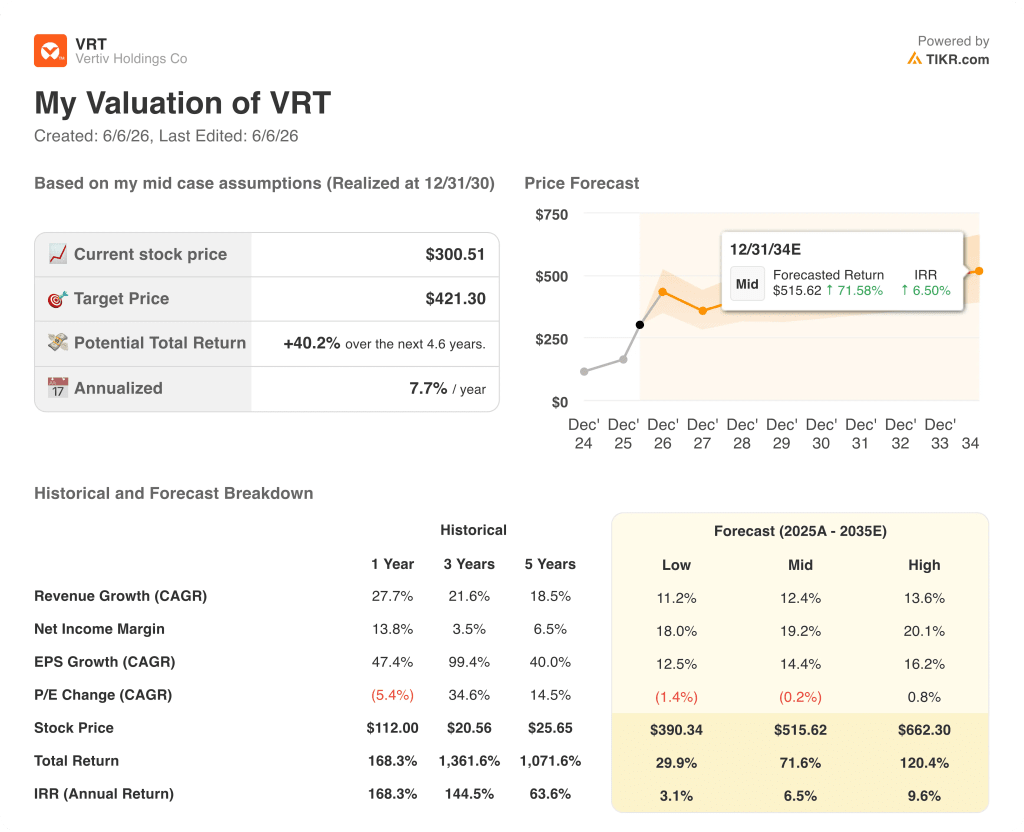

Is Vertiv Stock Undervalued in 2026? TIKR’s $421 Model Says the Market Is Underpricing the Margin Ramp

TIKR’s base case values Vertiv at approximately $421 by December 2030, implying around 40% total return from the current price of $301, or roughly 8% annualized over approximately 4.6 years.

The low case, anchored to revenue growth of around 11% annually and net income margins near 18%, points to a stock price of around $390 by 2030, a total return of approximately 30%, and an annualized IRR of roughly 3%.

The mid case assumes roughly 12% revenue compounding and net income margins expanding toward 19%, producing the $421 target at around 8% annualized, a return that trails the market historically but prices in continued execution without giving credit for EMEA upside or any reacceleration in enterprise AI adoption.

The high case, which the Investor Conference pipeline commentary begins to support, assumes around 14% revenue growth and margins approaching 20%, and produces a stock price near $662 by 2030, implying more than 120% total return and roughly 10% annualized.

The conditions already visible in the business: an EMEA recovery baked into second-half guidance, incremental 800-volt architecture revenue beginning to commercialize in 2027, and services growth compounding as installed base expands, each tilts the probability distribution toward the mid-to-high range rather than the low case the current stock price appears to reflect.

Is Vertiv Stock a Buy Right Now?

Vertiv stock trades at roughly 20% below the Street mean target of $377 and roughly 40% below TIKR’s mid-case model target of $421.

With 22 of 26 analysts carrying buy or outperform ratings, a guide raise following Q1 results, and EBITDA consensus growing approximately 47% year over year into the June 2026 quarter, the setup is constructive.

The key variable to watch is whether EMEA returns to growth in the second half as management guided.

What Do Analysts Say About Vertiv Stock?

The analyst consensus on VRT as of June 2026 is firmly bullish: 18 Buys, 4 Outperforms, 3 Holds, and 1 Underperform, with a mean price target of $377 and a Street high target of $500.

Analysts cite operating leverage, the AI data center infrastructure buildout, and Vertiv’s end-to-end portfolio as the primary reasons for the elevated conviction.

Should You Invest in Vertiv Holdings Co?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Vertiv Holdings Co stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vertiv Holdings Co alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VRT stock on TIKR for Free →