Key Stats for ServiceNow Stock

- Recent Performance: -6% Friday move

- 52-Week Range: $81 to $211

- Valuation Model Target Price: around $143

- Implied Upside: 27%

Analyze your favorite stocks like ServiceNow with TIKR (It’s free) >>>

What Happened?

ServiceNow Inc. stock fell about 6% Friday, closing near $112 per share as investors pulled back from high-growth software names during a broad tech selloff. The move came as the S&P 500 fell about 3%, the Nasdaq dropped about 4%, and stronger jobs data pushed bond yields higher, which pressured growth stocks whose valuations depend heavily on future earnings.

The stock moved lower because investors were weighing ServiceNow’s strong Q1 results against three specific concerns: margin pressure from the $7.75 billion Armis acquisition, delayed Middle East deals, and the risk that AI could pressure traditional software budgets.

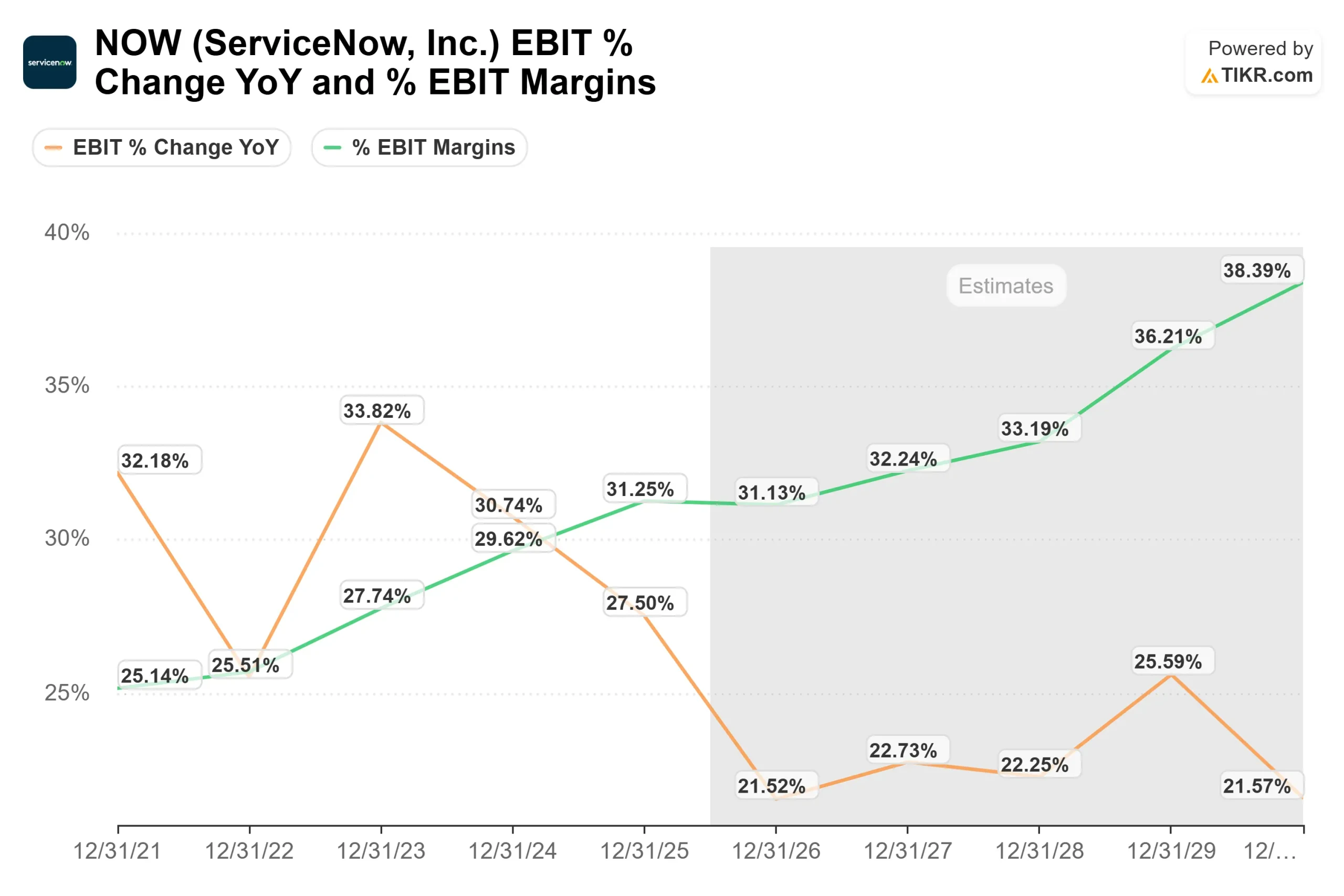

ServiceNow reported Q1 revenue of $3.77 billion, up 22% year over year, and adjusted EPS of $0.97, while delayed Middle East deals created a 75-basis-point headwind to subscription revenue growth. Armis is expected to pressure full-year operating margin by about 75 basis points, Q2 operating margin by about 125 basis points, and full-year free cash flow margin by about 200 basis points in 2026.

This week, ServiceNow used its Evercore TMT Conference appearance to frame Data and Analytics as a fast-ramping AI growth engine, with EVP and GM Gaurav Rewari saying the business is “on track to break $1 billion plus in ARR” in just a few quarters. The company highlighted RaptorDB Pro, which helps workflows and analytics run faster on the same data, and Workflow Data Fabric, which helps companies connect and govern data for AI agents, with more than 6,000 customers already using the product.

Analyst updates showed why the stock remains a split debate. Bank of America recently reinstated ServiceNow with a Buy rating and a $130 price target, arguing the company could benefit from AI workflow automation, while UBS downgraded the stock to Neutral and cut its target from $170 to $100 because of AI disruption and softer non-AI software spending concerns. The competitive setup is also tougher: Salesforce fell about 2% Friday, Oracle dropped about 10%, and Synopsys fell about 6%, showing that ServiceNow’s weakness came during a broader enterprise software and technology reset rather than from one company-specific issue alone.

ServiceNow also competes with Salesforce in customer workflows, Microsoft and Oracle in enterprise platforms, Workday in HR workflows, and Snowflake and Databricks in data infrastructure, where the key question is whether AI expands demand for ServiceNow’s workflow layer or shifts more spending toward competing AI and data platforms.

Value ServiceNow instantly (Free with TIKR) >>>

Is ServiceNow Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth: around 20%

- Operating Margins: around 33%

- Exit P/E Multiple: 20x

ServiceNow appears moderately undervalued based on the model, with the target price around $143 compared with the recent price near $112, implying about 27% upside.

The revenue growth assumption looks reasonable if ServiceNow can keep expanding beyond IT service management into HR, customer service, security, finance, and developer workflows, because each added product gives large customers more reasons to spend on the same platform.

See analysts’ growth forecasts and price targets for ServiceNow (It’s free) >>>

The margin assumption also looks more grounded because EBIT margins are already expected to move into the low-30% range over the next few years, which means the model does not require a sudden jump in profitability.

AI could become the biggest swing factor if Now Assist, Workflow Data Fabric, and RaptorDB Pro help customers manage AI agents, automate tickets, and use real-time data inside business workflows instead of relying on disconnected tools.

At current levels, ServiceNow looks undervalued, but not without execution risk, with future performance likely driven by AI workflow adoption, enterprise renewals, broader platform expansion, and proof that revenue growth can stay near 20% while margins recover.

How Much Upside Does NOW Stock Have From Here?

Investors can estimate ServiceNow’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value ServiceNow in under 60 seconds with TIKR (It’s free) >>>