Key Stats for Applied Materials Stock

- 52-Week Range: $154 to $511

- Current Price: $453

- Street Mean Target: $511

- Street High Target: $575

- Analyst Consensus: 28 Buy / 4 Outperform / 8 Hold

- TIKR Model Target (Dec. 2030): $536

Applied Materials Stock Drops 10% as Broadcom Spooks the Sector But the Setup Has Not Changed

Applied Materials (AMAT), the largest semiconductor equipment company in the United States, fell nearly 10% on June 5 after Broadcom’s chip sales outlook rattled the broader semiconductor sector and overshadowed what had been AMAT’s strongest fundamental setup in years.

The selloff came roughly three weeks after Applied posted record Q2 revenue of $7.91 billion, up 11% year over year, and guided Q3 to around $8.95 billion which is a figure that cleared Wall Street’s average estimate by nearly $860 million.

The company also raised its semiconductor equipment growth outlook for calendar 2026 to over 30%, up from its prior 20% guidance, citing incremental cleanroom additions and new customer orders placed across the prior quarter.

CEO Gary Dickerson framed the moment in unambiguous terms on the Q2 earnings call: “With rising demand and increasing long-term visibility from customers, we see an exceptionally strong foundation for sustained multiyear revenue and profit growth.”

The growth is concentrated in three areas — leading-edge foundry logic, DRAM, and advanced packaging which Applied expects to account for more than 80% of the year-over-year increase in total wafer fab equipment spending in 2026 and a similar share in 2027.

Applied is the number one process equipment provider in leading-edge foundry logic, the number one provider in DRAM, and the overall leader in advanced packaging, a structural position that CFO Brice Hill described at the Bank of America Global Technology Conference in June as the result of deliberate, decade-long investment cycles.

The EPIC Center, a planned $5 billion R&D facility in Silicon Valley expected to become operational by fall 2026, has already secured innovation partnerships with TSMC, Samsung, SK Hynix, Micron, Broadcom, ASU, RPI, and Stanford which a roster that reflects AMAT’s position at the center of the AI chip manufacturing ecosystem.

Applied Global Services, the company’s recurring revenue business that monitors over 35,000 connected chambers using AI-powered diagnostics, delivered record Q2 revenue of $1.67 billion, up 17% year over year, and the company raised its long-term AGS growth outlook from low double digits to mid-teens.

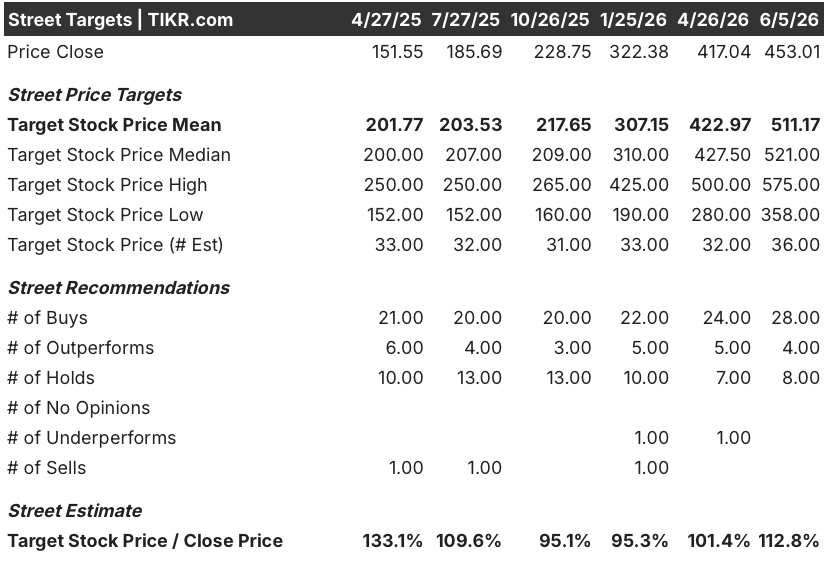

Applied Materials Stock Has 28 Buy Ratings and a $511 Mean Target. Here Is What the Earnings Numbers Say.

The Street’s conviction on Applied Materials stock has rarely been this concentrated: 28 analysts rate it a Buy, 4 rate it Outperform, and 8 rate it Hold, with a mean price target of $511 and a high target of $575.

The fundamental case rests on EPS acceleration, and the quarterly trajectory makes the argument directly.

Applied Materials stock’s normalized EPS came in at $2.86 for Q2, up 19.7% year over year on a reported actual basis, following $2.38 in Q1 and $2.17 in the October 2025 quarter.

The Q3 guide calls for normalized EPS of $3.36 which representing around 36% year-over-year growth from the prior-year $2.48 and consensus estimates have Q4 at approximately $3.59, implying a 65% year-over-year increase against the trough quarter of October 2025.

Looking into fiscal 2027, the estimates continue to climb: approximately $3.70 in the January quarter, approximately $3.98 in April, and approximately $4.26 in July — all figures reflecting a business that is structurally repricing as the AI equipment upcycle accelerates.

Applied Materials stock’s EBITDA trajectory confirms the same pattern: the January 2026 actual came in at $2.23 billion at 31.9% margins, rising to $2.67 billion at 33.8% margins in Q2 actuals, with consensus projecting approximately $3.18 billion in Q3 and approximately $3.34 billion in Q4 at margins holding near 35%.

Revenue estimates for Q3 come in at approximately $9 billion, accelerating to approximately $9.42 billion in Q4, and continuing to approximately $9.73 billion in January 2027, a trajectory anchored in the 8-quarter rolling customer forecasts that AMAT now consolidates for its 2,000 direct suppliers.

The thesis for AMAT is a structural growth compounder, not a cyclical bounce, and the current consensus reflects that: even after a near-10% decline on June 5, Applied Materials stock is trading at a level where the mean analyst target implies around 13% upside and the high target implies roughly 27%.

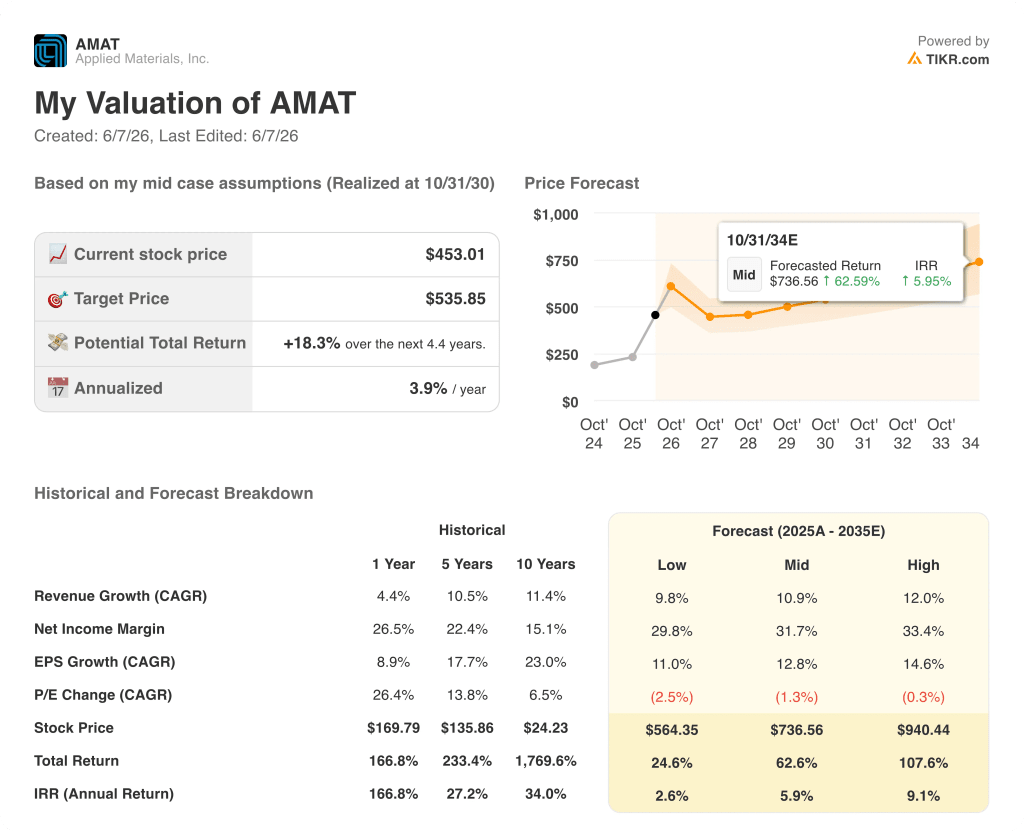

Is Applied Materials Stock Undervalued in 2026? TIKR’s $536 Model Points to Yes

TIKR’s base case values Applied Materials stock at approximately $536 by October 2030, implying around 18% total return from the current price of $453 over roughly 4 years, or approximately 4% annualized.

The base case builds on around 11% revenue CAGR through 2035, a net income margin of roughly 32%, and around 13% EPS CAGR — assumptions grounded in the demand signals AMAT is already seeing across its 8-quarter customer forecast pipeline.

The scenario spread sharpens the risk-reward picture considerably. In the low case, with revenue growth at around 10% CAGR and net income margins near 30%, the stock reaches approximately $564 by October 2030, implying around 25% total return. In the high case, with revenue CAGR near 12% and margins near 33%, the stock climbs to approximately $940 by October 2030, implying around 108% total return and around 9% annualized.

The base case annualized return of roughly 4% is modest by the standard of AMAT’s recent history, but it is built on conservative mid-cycle assumptions — the same assumptions that a 13-firm analyst upgrade cluster has already revised past following the Q2 beat. The gap between the TIKR base case and the Street’s mean target at $511 reflects the same structural undervaluation the current price is pricing in from the wrong direction.

What is the analyst consensus on Applied Materials stock?

As of early June 2026, 28 analysts rate Applied Materials stock a Buy, 4 rate it Outperform, and 8 rate it Hold, with no Sell ratings.

The mean price target is $511 and the high target is $575, implying upside of around 13% and around 27%, respectively, from the June 5 close of $453.

What is the TIKR model price target for AMAT?

TIKR’s mid-case valuation model targets approximately $536 for Applied Materials stock by October 2030, based on around 11% revenue CAGR, roughly 32% net income margins, and around 13% EPS CAGR over the forecast period.

The high case reaches approximately $940, implying around 108% total return.

Is Applied Materials a good investment for 2026?

The Street’s view is constructive: 32 of 40 analysts covering Applied Materials stock rate it Buy or Outperform, with a mean target of $511.

The TIKR base case adds approximately 18% total return through 2030 under conservative growth assumptions, though the annualized rate of roughly 4% reflects a stock that has already priced in substantial AI-cycle tailwinds through its prior run.

Should You Invest in Applied Materials, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Applied Materials, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Applied Materials, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMAT stock on TIKR for Free →