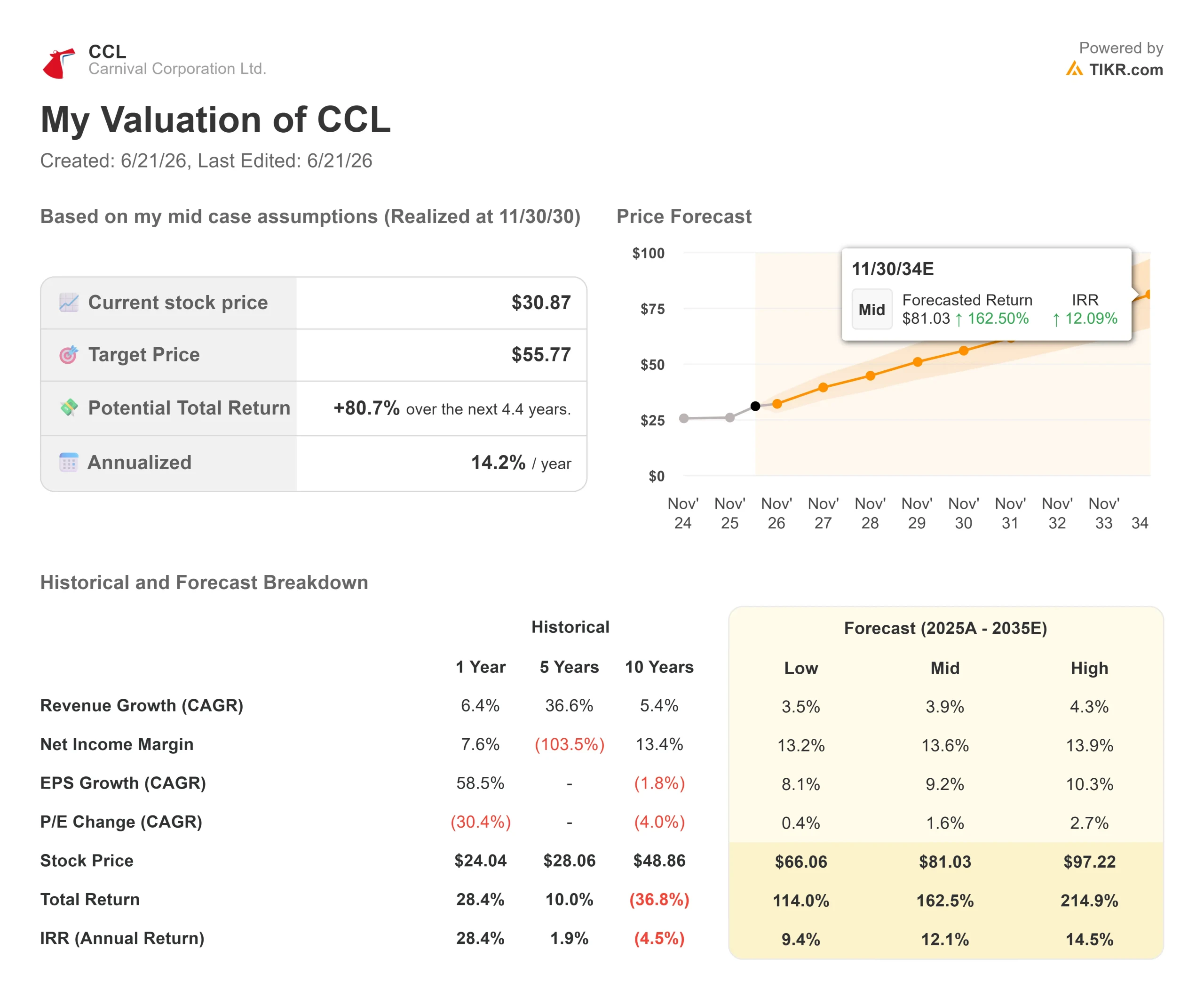

Key Stats for Carnival Stock

- Current Price: $30.87

- Target Price (Mid): ~$56

- Street Target: ~$35

- Potential Total Return:~81%

- Annualized IRR: ~14% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Carnival Corporation (CCL) reports second quarter earnings before the open on June 23, and most of its year is already sold. The world’s largest cruise operator entered the quarter with nearly 85% of 2026 on the books at historically high prices. That single fact reframes the whole report. With the year largely locked in, the number that matters is not the quarter just closed. It is what management says about yields for the rest of 2026.

Net yield, the cruise industry’s measure of revenue per available passenger day after costs, is the engine of this business. Much of Wall Street has positioned for Carnival to cut its full-year yield outlook, worried that softer European demand and a cautious consumer have caught up with the company. Stifel analyst Steven Wieczynski disagrees. On June 12, he raised his target to $36 from $35 and kept a Buy rating, arguing Carnival will beat its Q2 yield guidance and slightly raise the full-year figure. He thinks investors have braced for a cut that is not coming.

The stock reflects that unease. CCL closed at $30.87 on June 18, up 3.21% as fuel fears eased after a preliminary US-Iran deal to reopen the Strait of Hormuz, yet it is up only about 3% in 2026. Options pricing implies a swing of more than 5% on the print. The market cannot resolve the yield question until June 23.

Why the Setup Favors a Beat

Carnival enters the quarter from strength. On the first quarter call, CEO Josh Weinstein said bookings for current-year sailings rose 10% year-over-year, with customer deposits hitting a first quarter record of almost $8 billion. When most of the year is sold at known prices, a sudden yield collapse is hard to engineer.

The first quarter delivered. Revenue of $6.165 billion beat the Street by 0.43%, per TIKR, and net income of $275 million came in more than 55% above the prior year. Net yields rose 2.7% in constant currency, over 100 basis points better than guided. The stock rose 3.47% on the prior report.

Management has set a deliberately low Q2 bar. Asked why second-quarter yield growth was guided to 2% after the first quarter hit 2.7%, Weinstein said the company kept things conservative, adding, “we always try to exceed.” That is the dynamic Stifel is leaning on.

See historical and forward estimates for Carnival stock (It’s free!) >>>

The Fuel Question Cuts Both Ways

The bear case is real. Carnival does not hedge fuel, and a spike tied to the early-2026 Middle East conflict drove a roughly $500 million headwind that pushed full-year EPS guidance to $2.21, below the $2.25 posted in fiscal 2025. A 10% move in fuel cost per metric ton swings the bottom line by about $160 million, or $0.11 per share, for the rest of the year, per CFO David Bernstein.

The market underweights the offset. Weinstein argues consumption is the real lever: the company expects about $650 million in fuel-consumption savings this year versus 2019, which he said is “nicely higher” than the $500 million spike. June’s easing oil price removes some acute pressure. Fuel is the risk, but it may be near its worst.

A data breach disclosed earlier in 2026 added a smaller overhang. Carnival’s filings state that cyber-incident costs over the prior three years were not material to consolidated results, and the intrusion hit a limited part of the IT system rather than core reservations or payments. It is a contained risk, not a thesis-breaker.

Where Carnival Sits Against Its Peers

Carnival trades at 9.43x NTM EV/EBITDA, per TIKR, against Royal Caribbean (RCL) at 13.58x and Norwegian Cruise Line Holdings (NCLH) at 9.96x. On NTM price-to-earnings, CCL sits at 14.06x versus Royal Caribbean’s 17.81x. Carnival is the cheaper large-cap cruise name on earnings.

Some discount is fair. Carnival carries more leverage, with LTM net debt to EBITDA of 3.27x, and runs an older fleet. But the gap is wide for a company posting record bookings and a roughly $7 billion EBITDA run rate. PROPEL, its plan unveiled in March, targets return on invested capital above 16%, EPS growth of more than 50% versus 2025, and roughly $14 billion returned to shareholders by 2029, starting with a $2.5 billion buyback.

See how Carnival performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

The TIKR Valuation Model, on its mid-case assumptions realized 11/30/30 (about 4.4 years out), points to a target of around $56. That implies a potential total return of about 81% and an annualized IRR of around 14% per year from $30.87.

See analysts’ growth forecasts and price targets for Carnival stock (It’s free!) >>>

Two revenue drivers anchor the case. First, steady net yield growth is the commercial engine management calls its biggest lever. Second, measured capacity growth, with only about three ships entering service through 2029, keeps supply tight against demand. The margin driver is cost discipline, with yields guided to outpace costs without fuel. The primary risk is fuel, since a sustained spike compresses the margins the model relies on.

The upside: if yields keep beating and fuel normalizes, the model’s high case implies meaningfully more.

The downside: a sustained fuel shock or a real demand crack, where even the low case still produces a high single-digit IRR off a price near the stock’s recent floor.

Conclusion

Everything narrows to one line in the June 23 release: the full-year net yield outlook, guided to about 2.75% in March. Hold or raise it, and Stifel’s call is validated, the demand fears ease, and the discount to Royal Caribbean gets harder to defend. Cut it, and the bears who bet on fading pricing power are right. Watch the yield guide first and the EPS headline second, because at 85% booked, the forward number tells you more than the quarter just closed. The answer comes before the opening bell on Tuesday, June 23.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Carnival?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Carnival, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carnival alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Carnival on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!