Key Stats for Salesforce Stock

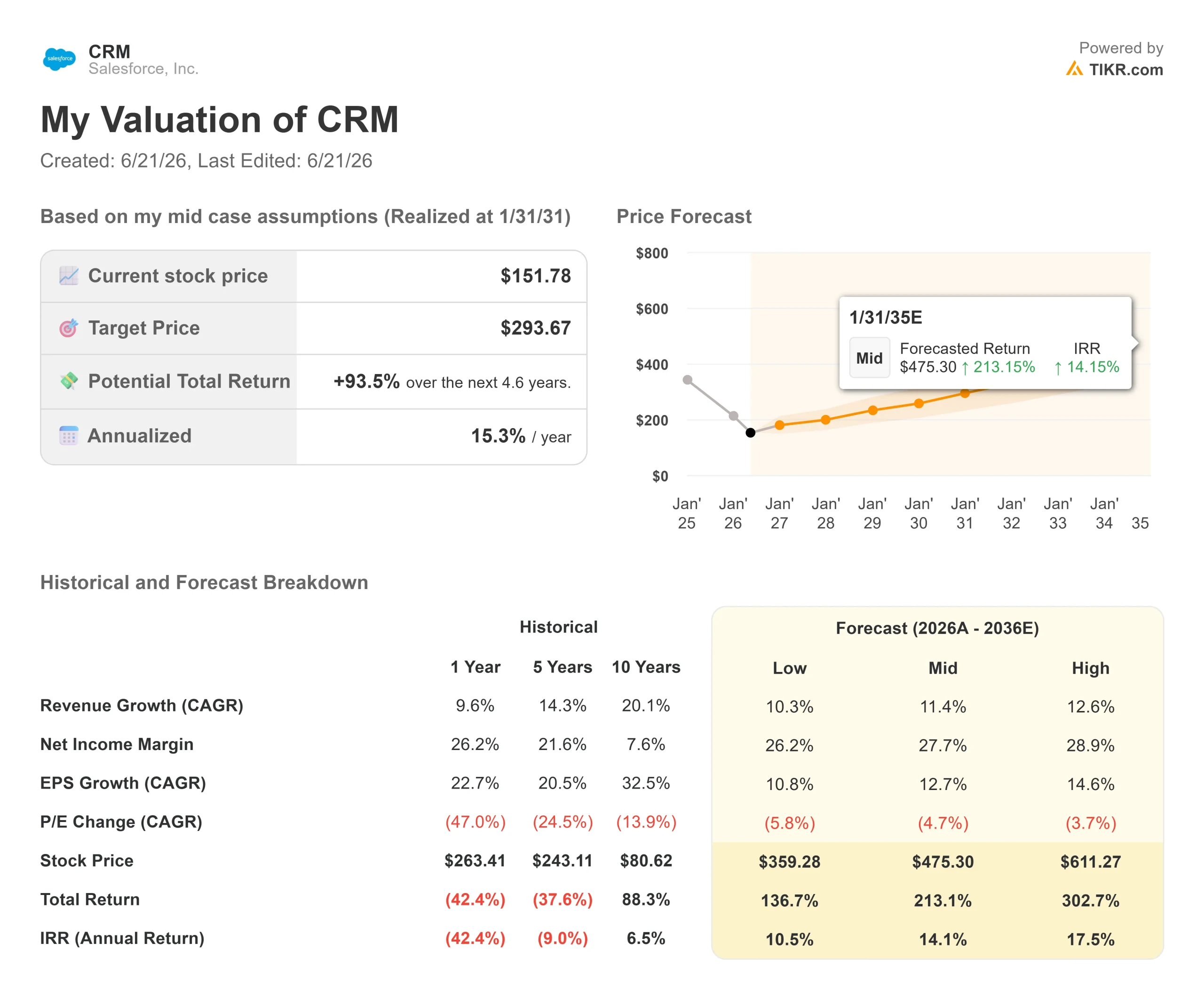

- Current Price: $151.78

- Target Price (Mid): ~$290

- Street Target: ~$250

- Potential Total Return: ~94%

- Annualized IRR: ~15% / year

- Earnings Reaction: (0.75%) (May 27, 2026)

- Max Drawdown: 44.53% (June 18, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Salesforce, Inc. (CRM) closed at $151.78 on June 18, just above its 52-week low and 45% below the $276.80 high it set a year ago. The stock has spent all of 2026 absorbing one fear: that the AI agents Salesforce now sells will quietly retire the human seats its customers have paid for since 1999. Bulls counter that the world’s largest customer relationship management (CRM) platform, the system enterprises use to track every customer interaction, becomes more valuable as agents multiply, not less. The market cannot yet decide who is right, and the gap between a beaten-down price and a still-growing business is wide enough to make the question worth answering.

What makes this moment different is that Salesforce just showed investors, through deals rather than slides, how it plans to win the argument.

Three Acquisitions in Three Weeks Reveal the Plan

In about three weeks, Salesforce signed deals for Contentful, a content platform that delivers digital content through open interfaces instead of fixed web pages, and m3ter, a billing platform built for consumption-based pricing. Each slots into a stack that already holds Informatica for data. The shares did not celebrate. CRM fell about 3.9% on June 9 as the m3ter news landed alongside fresh layoffs, because the market read billing infrastructure as plumbing, not growth.

The plumbing is the point. When one AI agent does the work of ten employees, charging for ten seats stops making sense. m3ter gives Salesforce the machinery to charge for what agents actually do, turning real-time usage into a bill. As Meredith Schmidt, EVP and GM of Agentforce Revenue Management, put it, AI is shifting the landscape “from traditional subscriptions to consumption-based models.” That reframes the bear case: Salesforce is not waiting for the seat model to break; it is building the model that replaces it.

See historical and forward estimates for Salesforce stock (It’s free!) >>>

What Management Said When the Slides Were Off

The clearest view came from a fireside chat at the Mizuho Technology Conference on June 9, where President and CMO Patrick Stokes walked through Headless 360, the company’s effort to let outside AI agents reach Salesforce data through open standards. Stokes said the company watched its own AI-lab partners stop logging into Salesforce as a website and start pulling from it through their own agents, and usage rose rather than fell.

“What we’re seeing is there’s actually an expansion of usage and expansion of consumption,” Stokes said. He signaled that “agent user licenses” will likely emerge alongside human seats, so customers can self-identify the agents running on the platform. That is the strategic answer to the seat question, delivered to the investors most worried about it. If agents become a new licensed unit feeding a metered bill, seat erosion becomes a transition, not a death sentence.

The Numbers Under the Fear

A company that has shed 45% of its value is usually one losing money. Salesforce is doing the opposite. It closed fiscal 2026 with $41.5 billion in revenue, up roughly 10%, a 77.6% gross margin, and a free cash flow margin of 34.7%. Its Q1 FY2027 report on May 27 beat on both lines, yet the stock slipped 0.75% that day. The business is converting more than a third of revenue into cash while actively shrinking its share count through an aggressive buyback.

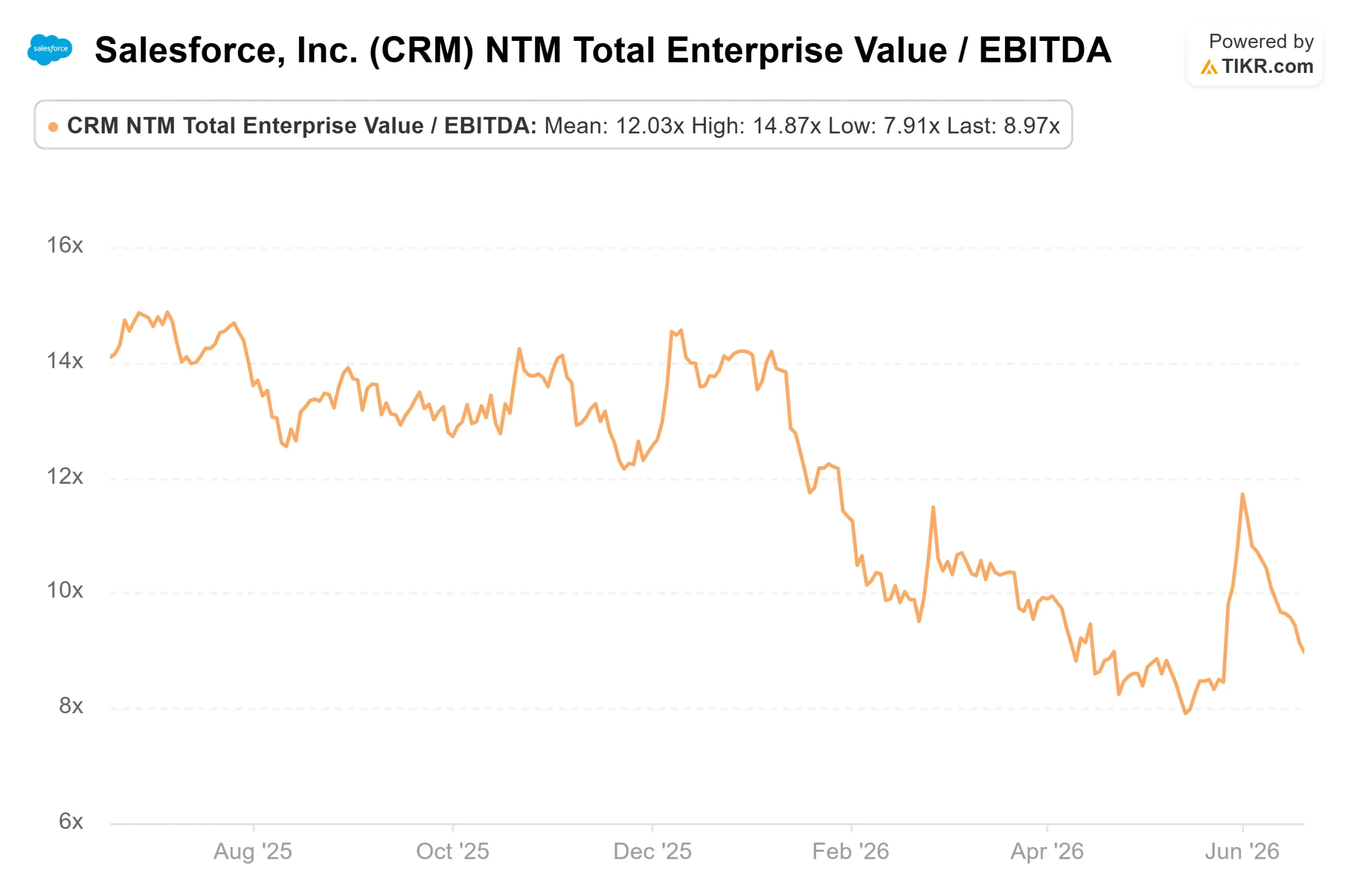

That cash engine is why the valuation looks dislocated rather than merely cheap. Salesforce trades at an NTM EV/EBITDA, a forward enterprise-value-to-earnings multiple, of 8.97x, against a software peer average near 29.87x. ServiceNow, Cadence, and CrowdStrike all trade at far richer forward multiples. The largest and most cash-generative name in the group is priced below nearly all of them, a discount that only makes sense if you believe its growth permanently stalls.

See how Salesforce performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Target Price (Mid): ~$290

- Potential Total Return:~94%

- Annualized IRR: ~15% / year (from $151.78 today)

See analysts’ growth forecasts and price targets for Salesforce stock (It’s free!) >>>

Two revenue drivers carry the forecast: continued double-digit subscription growth across the core clouds, and the ramp of Agentforce and consumption-based revenue as the m3ter billing layer comes online. The margin driver is operating leverage, with net income margin modeled to expand toward around 28% as agents scale without proportional headcount. The primary risk is that consumption revenue grows too slowly to offset seat erosion before it bites the top line.

The upside: the AI stack reignites growth, multiples normalize, and the stock roughly doubles.

The downside: the disruption fear proves real, growth slows, and the multiple stays compressed because conviction never returns.

Conclusion

The turning point will not be a product demo. It will be the Q2 FY2027 report, expected in late August, and the line that matters is organic revenue growth. Management guided H2 FY2027 to accelerate. If that reacceleration shows up in August, with Agentforce ARR climbing toward its next billion, the 45% drawdown starts to look like the bottom. If growth drifts lower while the acquisitions stay invisible in the revenue line, the market will keep treating Salesforce as a melting seat business, no matter how much cash it prints. Watch the top line in August.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Salesforce?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Salesforce, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Salesforce alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Salesforce on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!