Key Takeaways for News Corporation Stock as of June 2026

- Analysts rate News Corporation stock 5 Buys, 2 Outperforms, and 1 Hold with a street mean target of $35, implying 39% upside from the current price of $25.

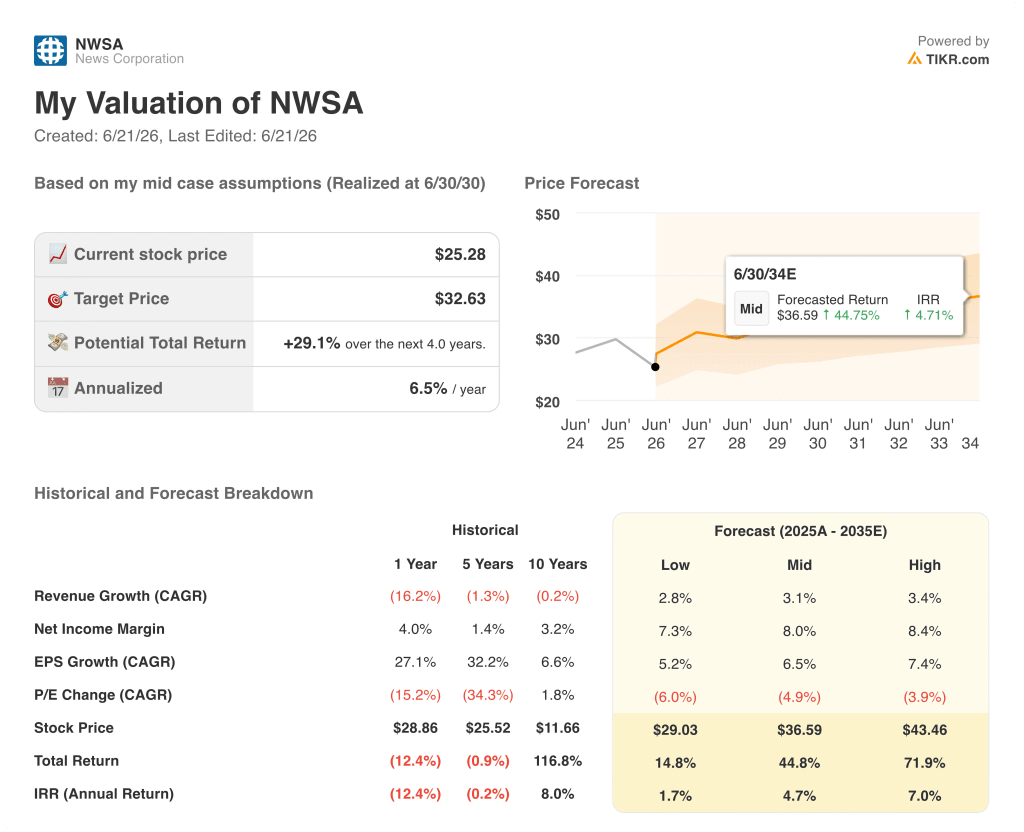

- TIKR’s mid-case model values News Corporation at $33 by June 2030, implying 29% total return from current levels, or 7% annualized.

- News Corporation stock’s Q3 2026 total segment EBITDA rose 18% year-over-year to $343 million, marking the company’s 12th consecutive quarter of EBITDA growth on a continuing operations basis.

News Corporation Posts 18% EBITDA Growth in Q3, Its 12th Straight Profitable Quarter

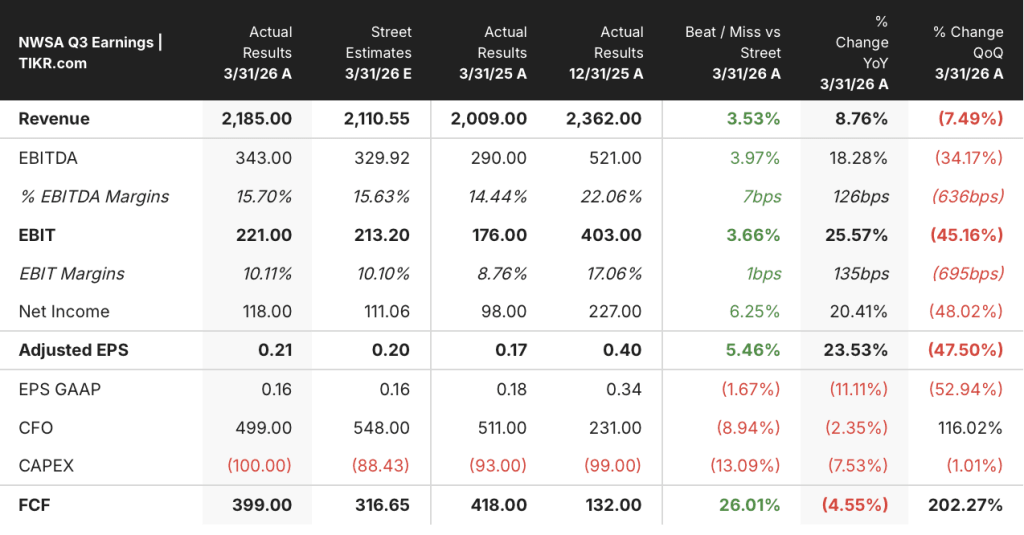

The market is still pricing News Corporation stock as a legacy media business, but the company reporting its 12th consecutive quarter of EBITDA growth is not legacy media. News Corporation (NWSA) posted Q3 fiscal 2026 revenue of $2.19 billion following its Q3 earnings call, beating the Street’s $2.11 billion estimate by 4%.

Total segment EBITDA climbed 18% to $343 million, expanding the margin from 14.4% to 15.7%.

The three segments management has identified as its core growth engines — Dow Jones, Digital Real Estate Services, and Book Publishing — each delivered double-digit EBITDA growth and drove the full-company beat.

Dow Jones, which houses the Wall Street Journal, Barron’s, and a fast-growing professional information business, posted Q3 revenue of $619 million, up 8%, with segment EBITDA expanding 11% to $147 million at a 23.7% margin, its 13th consecutive quarter of EBITDA growth.

Within Dow Jones, the Risk and Compliance unit, which provides enterprise clients with regulatory risk monitoring and compliance data grew 19% to $100 million, while Dow Jones Energy rose 12% to $77 million.

Digital Real Estate Services generated $473 million in revenue, up 17%, with segment EBITDA surging 25% to $155 million and margins widening from 31% to 33%, driven by REA Group’s 20% revenue gain in Australia and Realtor.com’s 10% revenue increase in the U.S. despite 30-year mortgage rates holding above 6%.

HarperCollins posted Q3 revenue of $555 million, up 8%, with segment EBITDA growing 14% to $73 million, as e-books surged 17% and audiobooks rose 7%.

CEO Robert Thomson said on the Q3 2026 earnings call:

“We are an AI inputs company, and that fact is reflected in our recent deal with Meta, which complements our partnership with OpenAI. We are negotiating several further deals with companies who recognize the preciousness of our provenance and which should have a positive impact on our revenue and profitability.”

The one offset was News Media, where segment EBITDA fell $18 million year-over-year as launch and marketing costs for the California Post investment weighed, but CFO Lavanya Chandrashekar was direct in providing context: News Media EBITDA fell $18 million while the total company EBITDA rose 18%.

Management guided to a strong fiscal Q4 finish and expects strong free cash flow growth for the full fiscal year, a signal that the cash generation trajectory visible in Q3’s $399 million FCF, which beat the Street’s $317 million estimate by 26% continues into the final period.

Analysts Rate News Corporation Stock 7 Buy-Side Ratings and Zero Sells After the Q3 Beat

Eight analysts cover News Corporation stock following the Q3 2026 results, with 5 Buy ratings, 2 Outperforms, and 1 Hold, with zero underperforms or sells.

The street mean target of $35 implies 39% upside from the current price of $25, with the high target at $43 implying 70% upside as of June 2026.

News Corporation stock’s three growth segments delivered collective EBITDA growth of 17% in Q3 fiscal 2026, accelerating from Q2’s pace, which tells the Street the transformation story is not stalling.

The quarter ending June 2026 carries a consensus EBITDA estimate of $370 million, implying 16% year-over-year growth at a margin of 17%, extending the trajectory set in Q3.

News Corporation stock’s FCF of $399 million in Q3 beat the $317 million Street estimate by 26%, and management expects strong full-year FCF growth despite modestly higher capital expenditures.

UBS specifically highlighted News Corporation stock as a preferred name in the Australian media space, noting that Dow Jones’s dominance in compliance and commodity data positions it to benefit from geopolitical volatility that drives corporate risk-monitoring demand.

The 5 Buys and 2 Outperforms against 1 Hold reflect a concrete disagreement: bulls see the Dow Jones $1 billion EBITDA target, set for achievement within five years, as a re-rating catalyst the market has not yet priced, while the Hold camp treats the AI licensing revenue contribution as incremental until actual deal economics flow through reported results and confirm the scale of the uplift.

NWSA Stock Generates More EBITDA Than NYT, But TRI Shows How Far the Re-Rating Can Go

News Corporation stock posted $340 million in EBITDA for the quarter ending March 2026, more than double The New York Times Company’s (NYT) $110 million over the same period, yet the market prices them as peers in the same legacy media category.

Thomson Reuters (TRI), whose professional information and compliance business most closely resembles what Dow Jones is becoming, generated $860 million in EBITDA for the quarter ending March 2026, a figure that illustrates the re-rating gap: TRI trades as a B2B data compounder, NWSA still trades as a newspaper company.

The forward estimates widen the case further, with NWSA’s EBITDA projected to reach $570 million in the quarter ending December 2026 against NYT’s $210 million, while TRI is expected to deliver $890 million in that same period, showing that the compounding gap between a re-rated data business and a media business compounds in both directions.

Is News Corporation Stock Undervalued in 2026? TIKR’s $33 Mid-Case Target Says Yes

TIKR’s mid-case values News Corporation at $33 by June 2030, implying 29% total return from the current price of $25, or 7% annualized over 4 years.

The EBITDA expansion cycle already underway at Dow Jones anchors TIKR’s target: Risk and Compliance grew 19% in Q3 and management placed it inside a $3.7 billion market growing at 11% to 13% annually, meaning the revenue runway that produces Dow Jones’s path to $1 billion in segment EBITDA is visible in current customer growth, not in a forecast assumption.

News Corporation stock’s Realtor.com business adds a second leg to the model: revenue per existing home sale now runs 20% above the Q3 2022 level despite historically low existing home sales volumes near 3.98 million, which means any housing market recovery compounds Realtor.com’s current revenue base at a yield that has already been proven through a suppressed cycle.

The TIKR target requires margin continuation across all three growth segments: Dow Jones holding or expanding its 23.7% EBITDA margin, Digital Real Estate sustaining the 32.8% margin delivered in Q3, and HarperCollins maintaining the operating discipline that produced its highest third-quarter segment EBITDA since fiscal 2021.

Should You Invest in News Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up News Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track News Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NWSA stock on TIKR for Free →

What does News Corporation stock’s Q3 FCF beat signal about shareholder returns?

News Corporation stock’s Q3 FCF of $399 million beat the Street’s $317 million estimate by 26%, and management accelerated buybacks to $193 million in Q3 alone. Fiscal year-to-date repurchases reached $459 million, funded by the Foxtel loan repayment and free cash flow, with the board calling the stock materially undervalued.