Key Takeaways for Spotify Stock as of June 2026

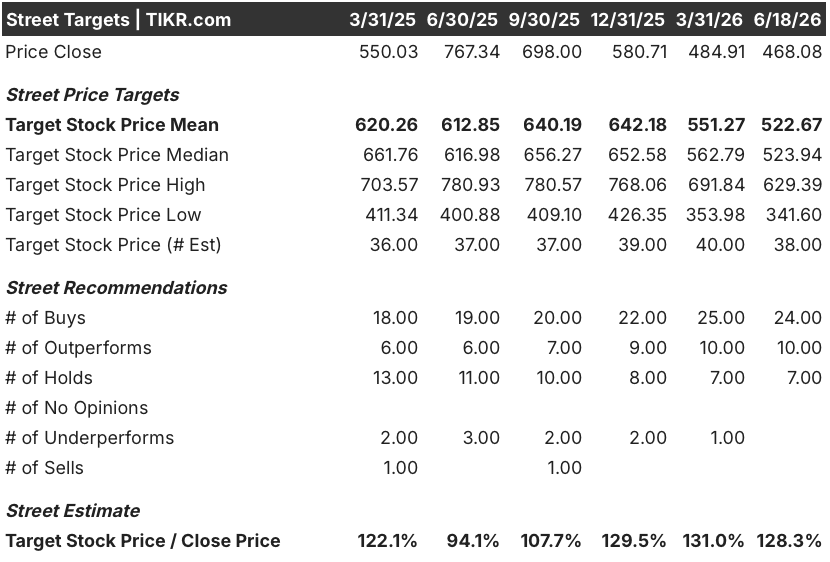

- Analysts rate Spotify stock 24 Buys / 10 Outperforms / 7 Holds with a street mean target of $523, implying 12% upside from the current price of $468.

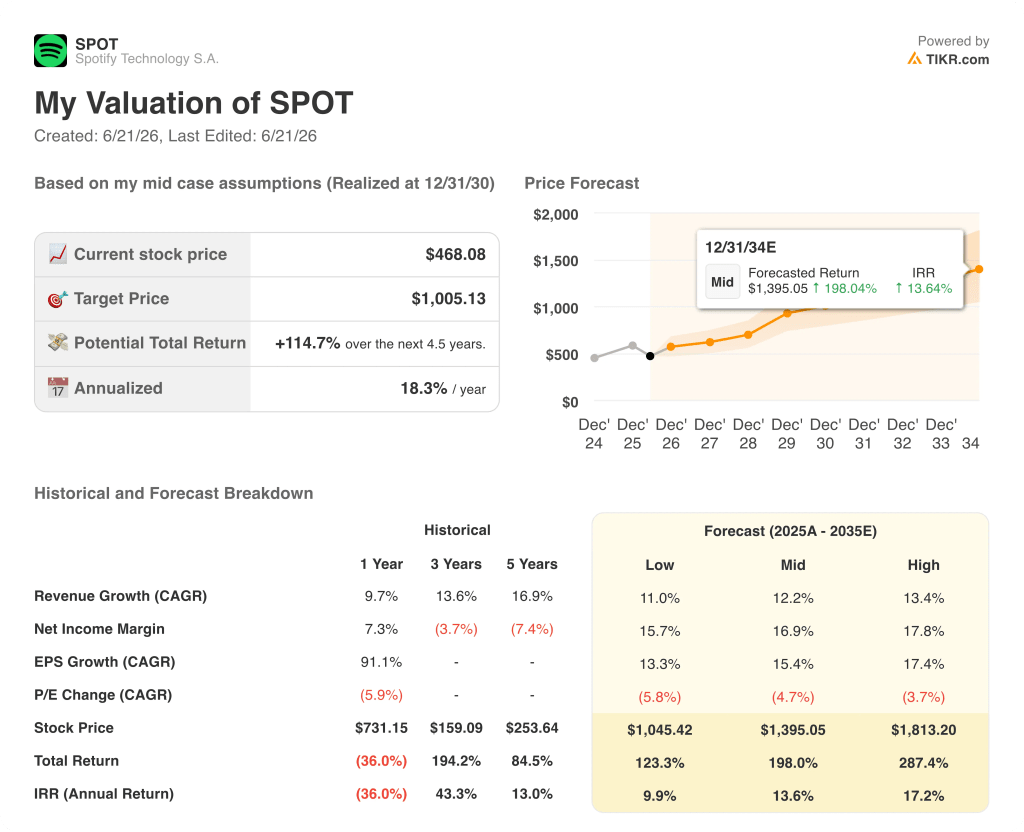

- TIKR’s mid-case model values Spotify at $1,005 by December 2030, implying 115% total return from current levels, or 18% annualized.

- Spotify stock’s Q1 2026 operating income reached €715 million, a record first-quarter result that beat the Street’s €681 million estimate by 5%, while management’s Q2 guide of €630 million triggered the selloff that now creates the entry point.

Spotify Stock Sold Off on a One-Quarter Spending Guide, Not a Business Problem

The market punished Spotify stock for a deliberate investment decision, not a deteriorating business.

Spotify Technology (SPOT) posted Q1 2026 revenue of €4.53 billion following its April 28 earnings call, growing 14% year-over-year on a constant currency basis and clearing the Street’s €4.52 billion consensus.

Operating income reached €715 million, a 15.8% margin and a Q1 record, with the beat driven largely by lower social charges (payroll taxes tied to share price) that came in €49 million better than management had guided.

Gross margin hit 33%, a first-quarter record and 133 basis points above the prior year, surpassing guidance by 20 basis points.

Monthly active users (MAUs) reached 761 million, up 12% year-over-year and 2 million ahead of guidance, with premium subscribers rising 9% to 293 million.

Free cash flow reached €824 million in the quarter, lifting the last-twelve-month total to €3.2 billion, Spotify’s highest ever trailing FCF figure.

The selloff trigger was Q2 guidance: management guided operating income to €630 million against analyst consensus of €684 million, a gap of roughly 8%.

Co-CEO Gustav Söderström explained the rationale on the Q1 earnings call: “We are not sitting around waiting for this opportunity to go past us. We are taking the opportunity.”

The spending increase, roughly €200 million spread across marketing and AI-related R&D, connects directly to a dense product launch schedule that management detailed at its May 21 Investor Day in New York, where co-CEO Alex Norström set 2030 targets of mid-teens revenue CAGR, 35% to 40% gross margin, and operating margin above 20%.

Management guided explicitly that the elevated OpEx persists through Q3 before moderating into Q4, making the earnings impact of the AI compute and marketing step-up a two-quarter event, not a structural reset.

Spotify also guided Q2 revenue to approximately €4.8 billion and Q2 MAUs to 778 million, both in line with analyst expectations, signaling no deterioration in top-line trajectory.

Spotify Stock’s 34 Buy-Side Ratings Reflect Conviction in the EBITDA Expansion Story

Wall Street expects Spotify stock to convert its 2030 roadmap into measurable EBITDA growth over the next several quarters, with 34 of 41 covering analysts rated at buy or outperform as of June 2026.

The mean target of $523 implies 12% upside from $468, though the street high of $629 signals that the most bullish analysts expect a faster re-rating once the near-term spending headwind clears.

Consensus estimates project Q2 2026 revenue of €4.79 billion, growing 14% year-over-year, confirming that analysts view the top-line acceleration as intact.

Q2 EBITDA consensus stands at €670 million, down from Q1’s €740 million actual but consistent with the spending cadence management guided.

Spotify stock’s FCF consensus for Q2 2026 reaches €860 million at a 18% FCF margin, a trajectory that management reinforced at Investor Day when CFO Christian Luiga stated the company plans to begin returning excess capital to shareholders beyond its anti-dilution buyback program as FCF compounds through 2030.

The 10 analysts holding Holds see the near-term spending guide as a sign of recurring investment cycles rather than a finite step-up, and the 2030 margin targets depend on the large taste model (Spotify’s proprietary AI personalization system trained on 3.4 trillion daily behavioral signals) delivering the engagement gains that management outlined.

The Street’s open question centers on whether Spotify’s EBITDA margin visibly inflects in Q4 2026 as management guided, or whether the cost moderation proves more gradual and pushes the 35% to 40% gross margin target closer to 2029 than 2030.

Is Spotify Stock Undervalued in 2026? TIKR’s $1,005 Model Says Yes

TIKR’s mid-case values Spotify at $1,005 by December 2030, implying 115% total return from the current price of $468, or 18% annualized over 4.5 years.

The path to that target runs through the margin expansion cycle Spotify has already demonstrated: gross margin expanded from 25% in 2022 to 33% in Q1 2026, and management’s 2030 gross margin target of 35% to 40% requires continuation of the same dynamic, not a step change in kind.

Spotify stock’s EBITDA trajectory supports the model’s revenue growth assumptions, with consensus projecting 14% year-over-year revenue growth in Q2 2026 and 15% in Q3, and those estimates embed the premium subscriber growth and ARPU expansion Spotify is already producing, with Q1 ARPU up 6% year-over-year.

The condition the model requires is that the €200 million OpEx increase proves temporary, as management guided, so that FCF and EBITDA margins begin visibly recovering in Q4 2026 and carry into 2027 as the large taste model reduces AI compute costs per interaction over time.

Should You Invest in Spotify Technology S.A.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Spotify Technology S.A. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Spotify Technology S.A. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SPOT stock on TIKR for Free →

What is driving Spotify stock down in 2026 despite record profitability?

Management’s Q2 guidance of €630 million in operating income, 8% below the €684 million consensus, triggered a mechanical selloff. The step-up is deliberate AI compute and marketing spending, guided to moderate into Q4 2026, not a structural margin reset.

Can Spotify reach 1 billion subscribers, and what does that mean for SPOT stock?

The 1 billion subscriber target is management’s stated 2030 goal. With 761 million MAUs and 293 million premium subscribers at Q1 2026, Spotify stock’s path requires continued conversion in India and Brazil, where management reports accelerating subscriber intake from large and growing free user bases.