Key Stats for Netflix Stock

- Past-week performance: -2%

- 52-week range: $82 to $134

- Valuation model target price: $132

- Implied upside: 47.7% over 2.0 years

Value your favorite stocks like Netflix with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Netflix (NFLX) stock fell about 2% over the past week, with shares trading near $88 on Thursday.

With much of the recent optimism around margin expansion and cash flow already reflected in the share price, buying interest faded once the stock approached prior resistance in the low $90s.

Wedbush recently lowered its price target to $115 while maintaining an Outperform rating, signaling caution amid recent stock performance.

At the same time, investor focus shifted toward whether Netflix can sustain growth beyond its recent improvements. Questions around how much additional revenue can come from advertising and pricing, without reaccelerating subscriber growth, weighed on sentiment during the week.

With no new positive developments to reset expectations and earnings approaching on January 20, selling pressure picked up as investors reduced exposure. The move reflects valuation sensitivity and uncertainty around the next leg of growth rather than a change in Netflix’s underlying business performance.

See analysts’ growth forecasts and price targets for Netflix (It’s free) >>>

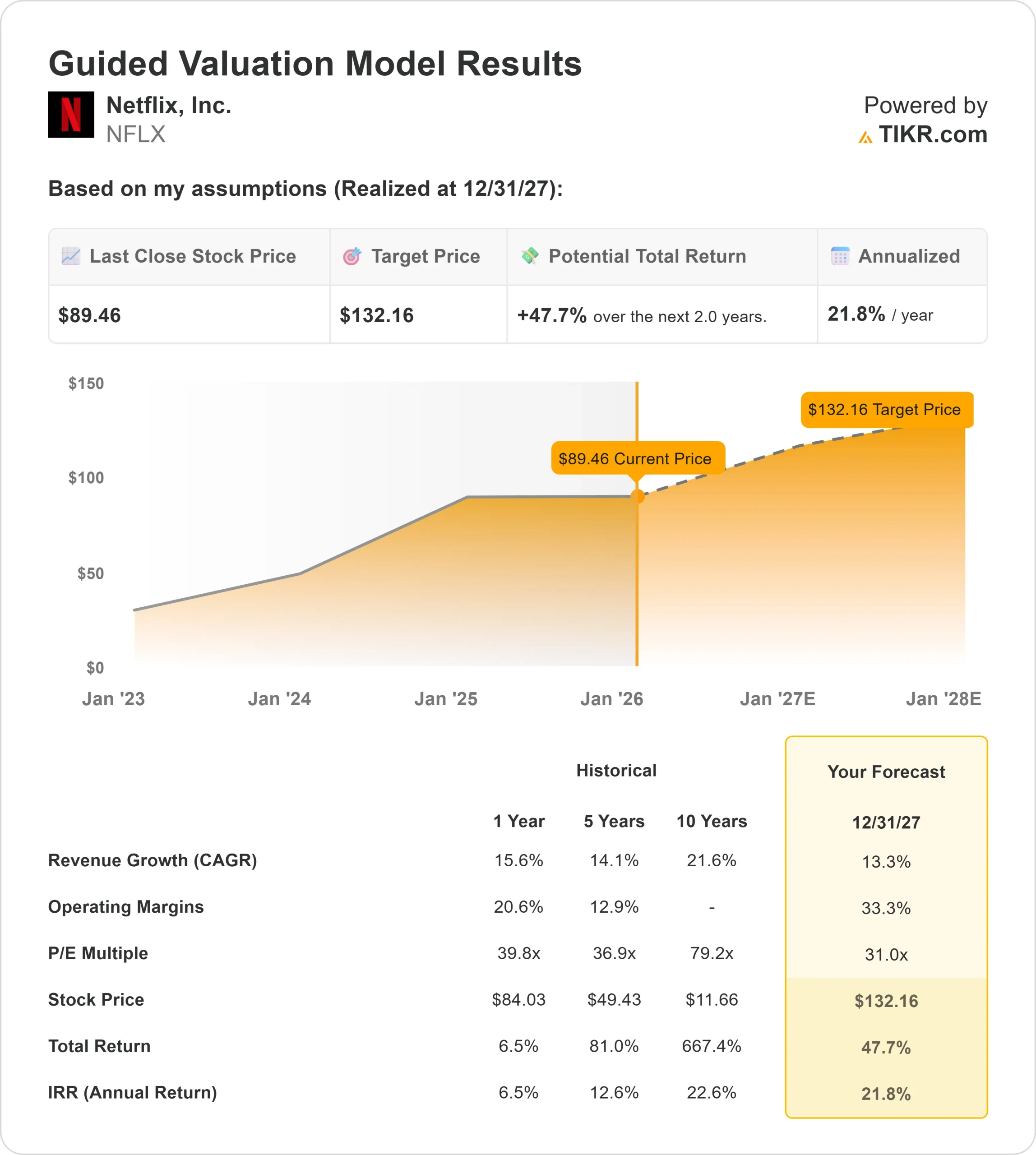

Is Netflix Undervalued?

Under valuation model assumptions realized through 12/31/27, the stock is modeled using:

- Revenue Growth (CAGR): 13.3%

- Operating Margins: 33.3%

- Exit P/E Multiple: 31.0x

Based on these inputs, the model estimates a target price of $132.16, implying a 47.7% total return from the current share price of $89.46 and an annualized return of 21.8% over the next 2.0 years.

Netflix’s results over the next year will depend on how quickly the advertising tier turns into meaningful profit, particularly whether higher ad monetization lifts revenue per user without hurting engagement.

Pricing remains a powerful lever, as recent increases have flowed through to revenue with limited churn, directly supporting margin expansion.

Content efficiency is another key driver, since sustaining watch time while keeping spending disciplined is what allows operating leverage to persist.

Password-sharing conversion also matters, because durable paid households create repeatable revenue rather than a one-time lift.

If these factors continue to work together, Netflix can grow earnings faster than revenue, supporting why the market remains comfortable with the stock’s current valuation.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>