Key Takeaways:

- Engie SA (ENGI) is reshaping its portfolio toward regulated and contracted energy infrastructure, which could support more stable cash flows over time.

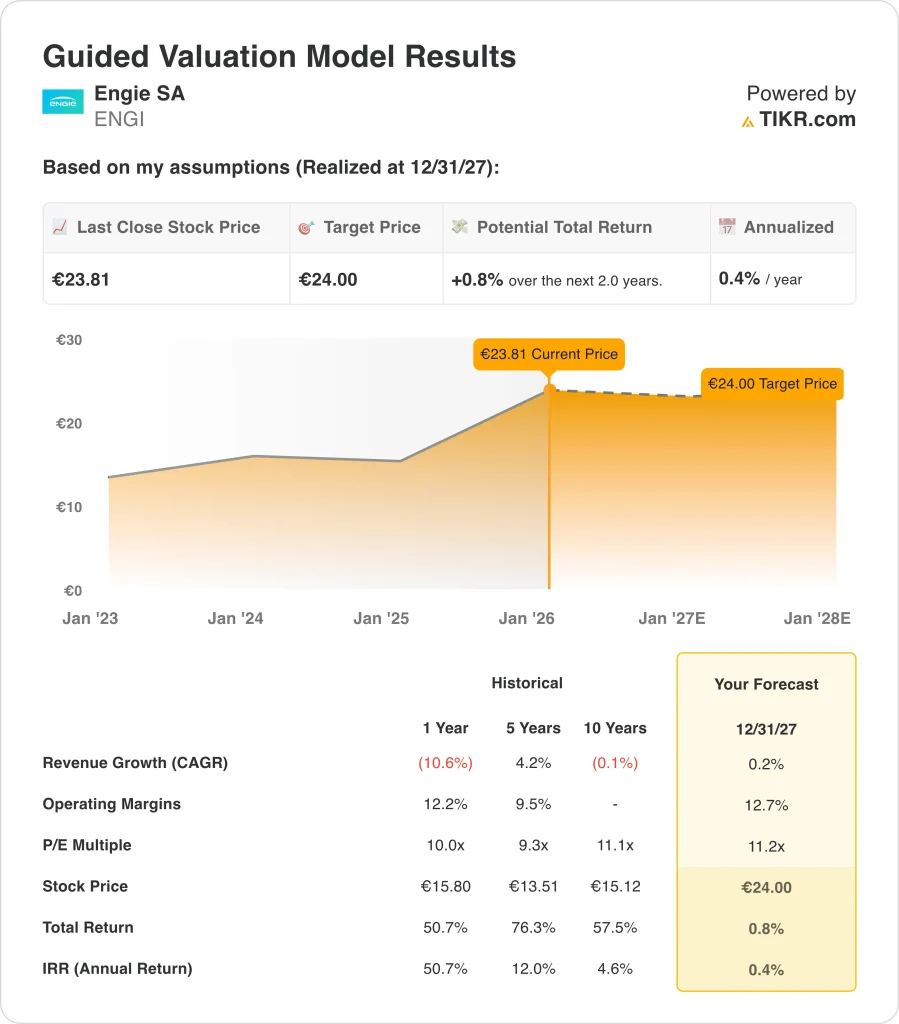

- ENGI stock could reasonably reach €24 per share by December 2027 and €25 per share by December 2029, based on our valuation assumptions.

- This implies a total return of 0.8% through 2027 and 3.5% through 2029 from today’s price of €23, with annualized returns of 0.4% and 0.9% over the next 2.0 and 4.0 years, respectively.

Engie SA (ENGI) is a major European utility that generates and distributes electricity and natural gas while providing energy services and facility management solutions across Europe and other regions. The group has been exiting more volatile upstream activities and reinvesting into networks, renewables, and long‑term contracted assets, aiming to improve the visibility and resilience of its earnings profile.

The company’s recent performance reflects this repositioning: despite a 10.6% revenue decline over the last year, Engie has delivered solid shareholder returns as margins improved and the share price rebounded from prior lows. Over the past 5 and 10 years, revenue growth has averaged about 4.2% and -0.1% respectively, highlighting how the business has been stabilizing after a long period of restructuring.

Here’s why Engie SA stock may offer only modest total returns through 2029 as the market already prices in much of its transition progress, according to TIKR’s valuation models.

What the Model Says for Engie SA Stock

We analyzed the potential for Engie SA stock using valuation assumptions that reflect its shift toward regulated networks, renewable generation, and long‑term energy contracts rather than aggressive growth bets.

Based on estimates of around 0.2% annual revenue growth, operating margins approaching 12.7%, and a normalized P/E multiple of about 11.2x, the model projects Engie SA stock could move from €23 to roughly €24 per share by December 2027.

That would translate into a 0.8% total return, or a 0.4% annualized return over the next 2.0 years.

This model does not count dividends, but with a 5.6% current yield, the return prospects still don’t look very promising:

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Engie SA stock:

1. Revenue Growth: 0.2%

Engie’s revenue has been volatile in recent years, with the most recent 1‑year period showing a 10.6% decline, largely offsetting the stronger 5‑year CAGR of 4.2%.

Based on analysts’ consensus estimates, the model assumes a forward revenue growth rate of roughly 0.2% annually, which is consistent with a mature, regulated utility that is no longer shrinking but is not expected to deliver high‑single‑digit expansion either.

2. Operating Margins: 12.7%

Historically, Engie’s operating margins have hovered in the high single‑ to low double‑digit range, with a recent 1‑year margin of about 12.2% and a 5‑year average near 9.5%.

Based on analysts’ consensus estimates, the forecast assumes margins trend slightly higher to around 12.7% by 2027–2029, reflecting the increasing weight of regulated networks and contracted renewables, which generally carry steadier profitability than more commodity‑exposed activities.

3. Exit P/E Multiple: 11.2x

Engie has historically traded around 9–11x earnings, with the 10‑year average near 11.1x and the most recent 1‑year multiple about 10.0x.

Based on analysts’ consensus estimates, we used an exit P/E multiple of roughly 11.2x, implying only a modest re‑rating from current levels as investors balance Engie’s improved stability against its relatively low structural growth profile.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for ENGI stock through 2030 show how sensitive potential returns are to small changes in growth, margins, and valuation multiples (these are estimates, not guaranteed returns).:

- Low Case: Modest growth of about 1.7% with softer margins and a lower implied price → -3.8% annual returns

- Mid Case: Revenue grows near 1.9% with margins normalizing and the P/E multiple around 11.2x → 0.9% annual returns

- High Case: Revenue approaches 2.1% annually with healthier profitability and a higher implied price near €27 → 3.5% annual returns

Even in the more cautious case, Engie SA stock is supported by its regulated and contracted asset base, improving earnings mix, and disciplined capital allocation, although the modeled range of outcomes suggests only limited upside for long‑term shareholders under current assumptions.

This model does not count dividends, but with a 5.6% current yield, the return prospects still don’t look very promising:

See what analysts forecast for ENGI stock over the next 5 years (Free with TIKR) >>>

How Much Upside Does Engie SA Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!