Key Stats for Monday.com Stock

- Past-Week Performance: -4%

- 52-Week Range: $68.7 to $317

- Current Price: $72.6

What Happened?

Monday.com stock (MNDAY) trades at $72.64, sitting 77.1% below its 52-week high of $316.98, after three consecutive earnings-day crashes totaling over 60% in cumulative declines stripped the stock of its premium growth valuation.

The selling accelerated after management triggered a full reset on February 9, withdrawing all 2027 financial targets, guiding 2026 revenue to $1.452 billion to $1.462 billion, and confirming the no-touch SMB channel remained persistently broken with no recovery expected.

Beneath the guidance cut, the core mechanics show a business splitting in two: the enterprise motion is genuinely accelerating with $500,000-plus ARR customers growing 74% and gross retention hitting a record 91%, while the self-serve SMB channel drags the entire top-line growth rate down from 27% to 18%.

Investors are now forcing a re-rating from a high-growth SaaS compounder to a bifurcated business story, where the premium multiple collapses until management proves the enterprise engine can fully offset the structural SMB deterioration.

Co-CEO Eran Zinman stated on the Q4 earnings call that “Monday Vibe is also off to an exceptional start,” calling it the fastest product in monday.com history to surpass $1 million in ARR, signaling a new monetization layer investors have not yet priced in.

Additionally, strategic conviction surfaced on February 25 when Guidde closed a $50 million funding round led by PSG Equity with monday.com participating directly, reinforcing the company’s commitment to expanding its AI-powered workflow ecosystem beyond its core platform.

Looking further out, monday.com’s enterprise consolidation play positions it directly against Salesforce and ServiceNow at the workflow orchestration layer, and if Vibe and AI agents scale as designed, the company could recapture premium growth multiples within the next three to five years.

Wall Street’s Take on MNDAY Stock

monday.com’s decision to withdraw all 2027 targets and reset 2026 revenue guidance to $1.452 billion directly triggered a deceleration narrative that now defines how investors price every forward quarter of this business.

Yet the fundamentals tell a more nuanced story: revenue grew 26.7% in 2025, the $500,000-plus ARR customer cohort expanded 74%, and the mid-case model projects 14.8% revenue CAGR through 2031 as enterprise momentum compounds.

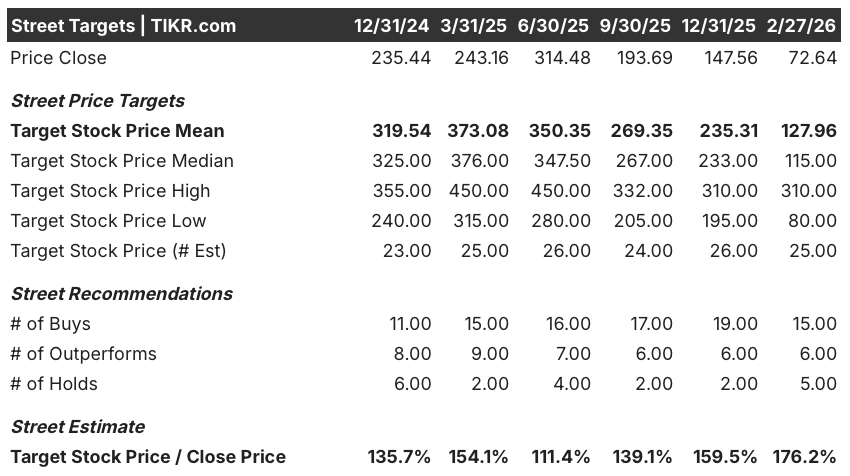

Despite the selloff, 15 analysts maintain Buy ratings, 6 rate it Outperform, and 5 hold, producing a mean price target of $127.96, implying 76.2% upside from the February 27 close of $72.64.

The analyst target range spans $80 on the low end to $310 on the high end, where SMB stabilization and Vibe ARR scaling drive the upside case while continued no-touch deterioration and margin compression anchor the downside.

What Does the Valuation Model Say?

TIKR’s mid-case valuation model targets $139.26, implying a 91.7% total return over 4.8 years at a 14.4% annual IRR. The stock trades at less than half that target today.

The market is punishing monday.com for SMB weakness, but enterprise gross retention just hit a record 91% and renewal rates sit in the high 90s, metrics inconsistent with a structurally broken business.

Monday Vibe became the fastest product in company history to surpass $1 million in ARR, a monetization signal the current $72.64 price does not reflect at all.

Management’s continued $735 million buyback authorization signals that the board views this selloff as a mispricing, not a fundamental deterioration of the underlying business model.

The thesis breaks if EPS, already forecast to contract 7.9% to $4.05 in 2026, continues declining into 2027 as SMB drag overwhelms enterprise expansion and margin recovery stalls entirely.

The Q1 2026 earnings print will reveal whether revenue breaks above the $340 million guidance ceiling and whether NDR holds at 110% or slips further, making it the single most important data point for bulls right now.

Accordingly, MNDY stock seems to be undervalued at $72.64 with 76.2% mean analyst upside and a 14.4% IRR model, but Q1 NDR stability is the number that unlocks the re-rating.

Should You Invest in Monday.com?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MNDAY stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Monday.com alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MNDAY stock on TIKR for Free →