Key Stats for Kyndryl Holdings Stock

- Past-Week Performance: -1.4%

- 52-Week Range: $10.1 to $44.2

- Current Price: $12.3

What Happened?

Kyndryl Holdings stock (KD) sits at $12.33, roughly 72% below its 52-week high of $44.20, after a single February 9 session erased more than half the company’s market value when the SEC investigation became public.

The immediate trigger was simultaneous: the SEC issued voluntary document requests, the CFO and General Counsel departed immediately, and the audit committee launched a formal review of cash management practices and internal controls, all on the same day.

Beneath the governance shock, the operating business had actually delivered: Q3 hyperscaler revenue hit $500 million, up 58% year-over-year, putting the company on track to nearly double its original $1.8 billion full-year hyperscaler revenue target to nearly $2.0 billion.

The market is now re-rating Kyndryl Holdings from a turnaround recovery story into a governance risk name, even as its gross profit book-to-bill ratio of 1.2 and $15.4 billion in trailing 12-month signings argue the underlying business remains structurally sound.

Martin Schroeter, Chairman and CEO, stated on the Q3 earnings call that “the transformation that this business has undergone, starting with nearly $4 billion in IBM spend which is now approximately $2 billion, while at the same time, going from essentially 0 in hyperscaler-related revenue to nearly $2 billion and growing, is profound,” as hyperscaler revenue surged 58% year-over-year in Q3.

Despite the collapse, Interim CFO Harsh Chugh is scheduled to present at the Morgan Stanley TMT Conference on March 3, representing the company’s first major institutional engagement since the February 9 disclosures rattled investor confidence.

Over the next 3 to 5 years, Kyndryl’s ability to grow hyperscaler revenue toward a $4.0 billion run rate, while shifting more than 90% of its P&L to high-margin post-spin contracts targeting 9% pretax margins, will determine whether the current price represents destruction or opportunity.

Wall Street’s Take on KD Stock

The SEC investigation and simultaneous CFO departure on February 9 severed investor trust overnight, but the underlying earnings trajectory, with adjusted PTI growing 5% in Q3, has not actually reversed course.

The fundamental numbers tell a recovery story the market is ignoring: EBITDA margins expand from 16.7% in FY 2025 to a forecast 17.5% in FY 2026, while normalized EPS surges 49.8% from $1.19 to $1.78.

Wall Street has fractured under the weight of the governance shock, with only 1 buy, 1 outperform, 3 holds, and 1 underperform among 6 analysts, yet the mean price target still sits at $19.0, implying 54.1% upside from $12.33.

The analyst target range spans $13.0 on the low end to $28.0 on the high end, with the high scenario requiring a clean SEC resolution and no restatement, while the low reflects a prolonged investigation that further freezes enterprise deal activity.

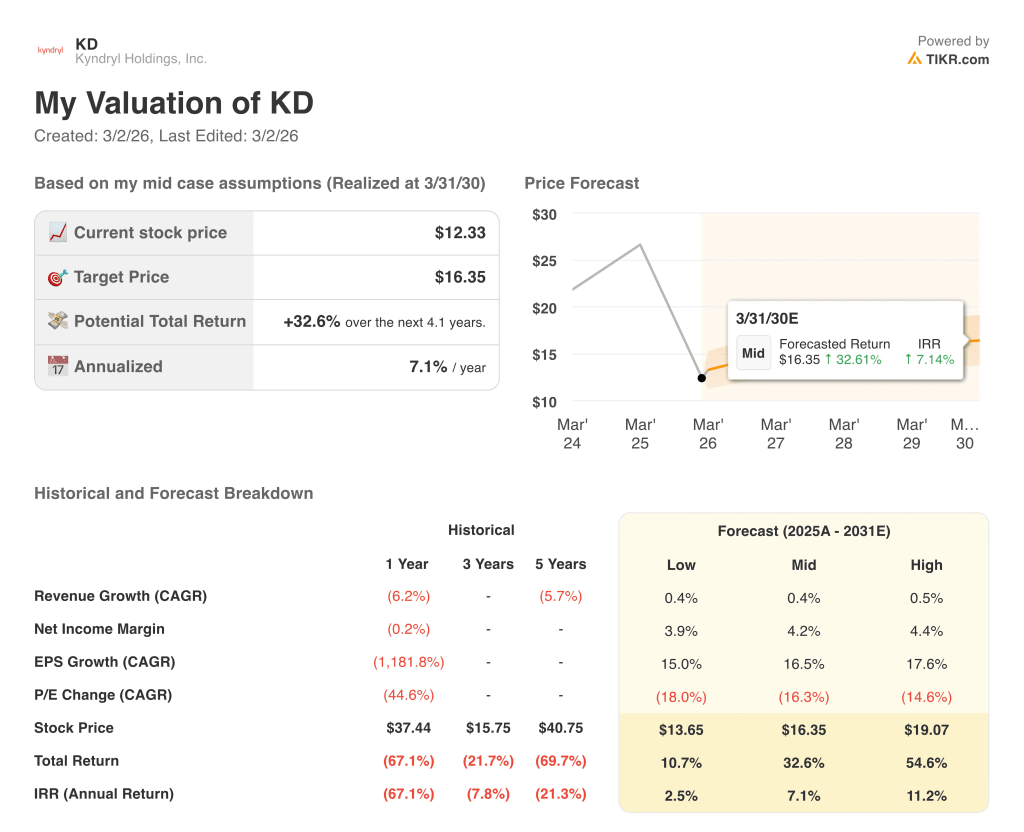

What Does the Valuation Model Say?

TIKR’s mid-case model targets $16.35 by March 2030, implying a 32.6% total return and a 7.1% IRR from current levels. The market is pricing permanent impairment; the model says the damage is temporary and recoverable.

The market is treating Kyndryl Holdings as a fraud story, but hyperscaler revenue of $500 million in a single quarter, up 58% year-over-year, proves the core growth engine is running independently of the governance issue.

The gross profit book-to-bill ratio of 1.2 over the last 12 months means Kyndryl added $4.0 billion of projected gross profit to its backlog while only consuming $3.3 billion, a compounding dynamic the current price completely ignores.

Management maintained its FY 2028 adjusted PTI target of more than $1.2 billion and explicitly stated no restatement is expected, which is the clearest signal that insiders see the investigation as procedural, not existential.

The real risk is that the SEC investigation uncovers cash management irregularities material enough to force a restatement, which would invalidate the $575 million to $600 million adjusted PTI guidance and reset the entire FY 2028 framework.

The April 13 lead plaintiff deadline and any SEC update before then will tell investors whether this is a contained governance lapse or a deepening financial scandal.

KD is deeply undervalued at $12.33 with a 54.1% mean analyst upside and a clean SEC outcome as the single gate that unlocks the recovery.

Should You Invest in Kyndryl Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KD stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Kyndryl Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KD stock on TIKR for Free →