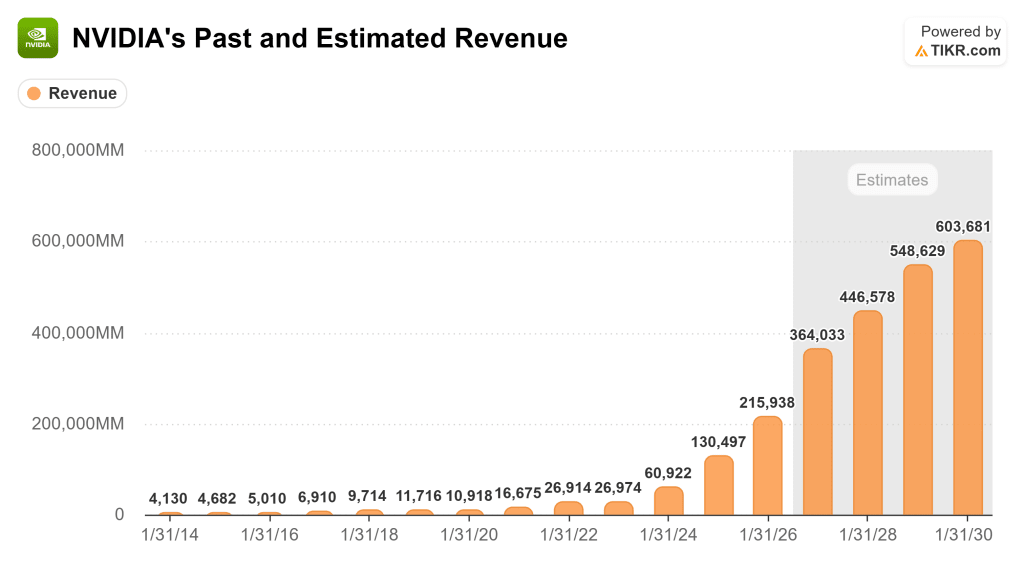

NVIDIA reported Q4 fiscal 2026 earnings this week, posting $68 billion in revenue (up 73% year-over-year) and guiding Q1 to $78 billion.

Despite the blowout results and strong forward guidance, the stock has sold off since the report. For long-term investors, the price action matters less than what management actually said on the call.

Here are the four most important quotes from the earnings call and what each one means for the business going forward. (You can read the full call for free with a TIKR account).

On Why Customer CapEx Will Keep Growing

“I am confident in their cash flow growing. And the reason for that is very simple. We have now seen the inflection of agentic AI and the usefulness of agents across the world and enterprises everywhere. You’re seeing incredible compute demand because of it. In this new world of AI, compute is revenues. Without compute, there’s no way to generate tokens. Without tokens, there’s no way to grow revenues. So in this new world of AI, compute equals revenues.”

Jensen Huang, CEO, responding to a question about whether NVIDIA can continue growing if customer CapEx plateaus.

This is the most important conceptual framework Jensen laid out on the call. He is arguing that CapEx spending by cloud providers is no longer discretionary or speculative. It is directly tied to revenue generation. In this framing, every dollar spent on compute infrastructure translates into token output, and tokens are now monetized. The implication is that CapEx is not a cost center but a revenue engine, which fundamentally changes how investors might evaluate hyperscaler spending levels.

The risk embedded in this view is that it depends on sustained and growing demand for AI tokens at current or improving economics. If token pricing compresses faster than compute efficiency improves, or if enterprise adoption of agentic AI stalls, the “compute equals revenues” thesis weakens. But for now, the evidence Jensen points to, including the rapid growth at Anthropic (10x revenue in a year) and the proliferation of coding agents, supports his argument.

On Revenue Visibility and the Size of the Opportunity

“We look ahead, we expect sequential revenue growth throughout calendar 2026, exceeding what was included in the $500 billion Blackwell and Rubin revenue opportunity we shared last year. We believe we have inventory and supply commitments in place to address future demand, including shipments extending into calendar 2027.”

Colette Kress, EVP and CFO, discussing forward revenue visibility and supply positioning.

This is a significant statement because it raises the long-term revenue opportunity above the $500 billion figure management had previously anchored to. It also extends the visibility window into calendar 2027, which is unusual for a semiconductor company and reflects the depth of contractual commitments NVIDIA has secured from its customers.

The supply commitment language is worth paying close attention to. NVIDIA has been locking in capacity and inventory further out than typical, which suggests both confidence in demand durability and a strategic effort to prevent competitors from gaining share through supply availability. It also means NVIDIA is taking on more balance sheet risk with elevated purchase commitments, something investors should monitor if demand were to soften unexpectedly.

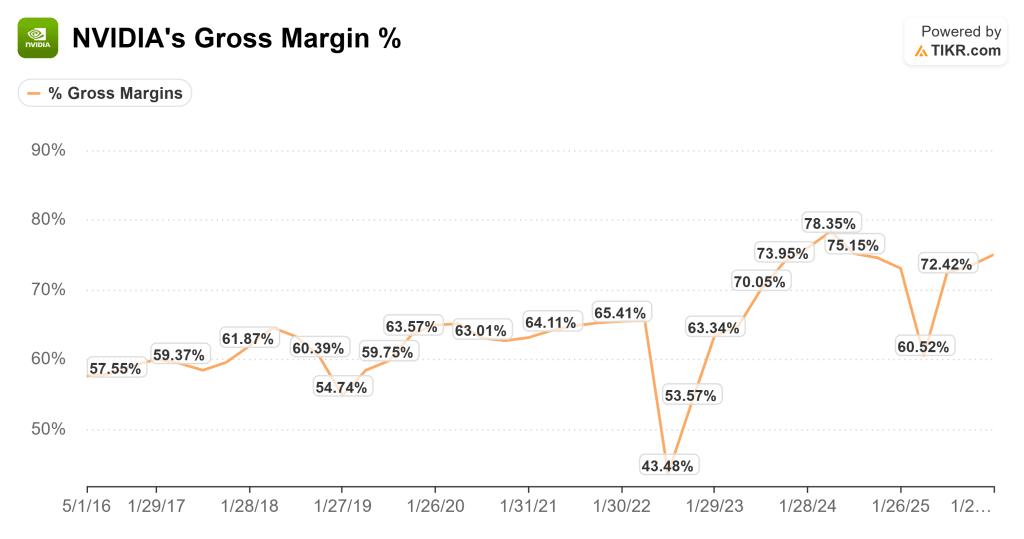

On Gross Margin Sustainability

“The single most important lever of our gross margins is actually delivering generational leads to our customers. That is the single most important thing. If we could deliver generationally performance per watt that exceeds dramatically what Moore’s Law can do. If we can deliver performance per dollar dramatically more than the cost of our systems than the price of our systems, then we can continue to sustain our gross margins.”

Jensen Huang responding to a question about gross margin sustainability.

This is Jensen articulating NVIDIA’s pricing power thesis in its simplest form. Gross margins in the mid-70s are sustainable as long as each new architecture delivers a step-function improvement in customer economics. If NVIDIA can consistently offer 10x or more improvement in performance per watt and performance per dollar, customers will pay premium prices because the total cost of ownership is still dramatically better than the alternative.

This is a moat built on engineering velocity, not market structure. NVIDIA is essentially saying that its margin defense comes from running faster than physics and competition would otherwise allow. The annual cadence of new architectures (Blackwell, Blackwell Ultra, Vera Rubin, and beyond) is designed to maintain this generational leap.

On Why This Computing Shift Is Permanent

“Now why is it so certain that this is the future of computing? And the reason for that is because the way we used to do software was prerecorded, everything was captured a priori. We pre-compile the software. We pre-write the content. We prerecord the videos. But now everything is generative in real time. And when it’s generated in real time, you could take into context of the person, the situation, the query and the intentions could all be taken into consideration to generate the outcome of this new software called, we call AI, agentic AI.”

Jensen Huang responding to a question about the path to $3-4 trillion in data center CapEx by 2030 and which applications will drive it.

This is the most important long-term framing on the call. For the past year-plus, Jensen has been drawing a line between the old computing paradigm (pre-compiled, static, stored) and the new one (generative, real-time, contextual). The analogy to a DVD player versus a live computer is simple but powerful. Pre-recorded software required minimal ongoing compute. Generative software requires continuous compute to produce every output in real time, personalized to the user and situation.

If you accept this framing, the implications for infrastructure spending are enormous. The world spent roughly $300-400 billion annually on classical computing infrastructure. If the new paradigm requires orders of magnitude more compute per unit of output, then the total addressable market for AI infrastructure is not a temporary spike but a permanent and growing structural shift. Jensen’s $3-4 trillion figure for 2030 data center CapEx follows logically from this argument.

The bear case would be that not all software needs to be generative, or that efficiency gains in model architecture and inference reduce the compute required per token faster than demand grows. But the trend lines Jensen describes, where agentic AI is consuming exponentially more tokens and delivering measurable ROI (as seen in Meta’s ad performance improvements and Anthropic’s revenue trajectory), suggest the demand side of this equation is accelerating. For long-term investors, the question is not whether this transition happens, but how fast and how large the opportunity becomes.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.