Key Stats for Logitech Stock

- This Week Performance: +3%

- 52-Week Range: $63.7 to $122.5

- Current Price: $91.9

What Happened?

Logitech (LOGN) shattered its own profitability ceiling when it delivered $312 million in non-GAAP operating income for Q3, the best quarterly result in the company’s history outside pandemic peaks, validating the $91.9 stock price as a reflection of genuine earnings power rather than market optimism.

Driving the re-rating, CFO Matteo Anversa took center stage at the Goldman Sachs European Technology Conference on February 25, directly addressing investor concerns about PC demand, memory shortages, and tariff exposure with data-backed confidence that visibly reinforced institutional conviction in the name.

The engine behind Logitech’s momentum is a three-part profitability machine: the MX Master 4 launch drove Pointing Devices up 9%, manufacturing diversification slashed U.S.-China sourcing from 40% to under 10%, and a 10% U.S. price hike collectively neutralized all tariff headwinds while expanding non-GAAP gross margin to 43.5%.

Beyond the numbers, the market is actively re-rating Logitech from a mature peripherals hardware company into a durable, margin-rich platform business, as B2B now outpaces B2C, AI-enabled video collaboration grows double digits in EMEA and Asia Pacific, and vertical expansion into education drives B2B sell-through up mid-teens.

CEO Hanneke Faber stated on the Q3 earnings call that “with the exception of pandemic peaks, we drove record operating income despite tariff headwinds,” a declaration that reframed Logitech’s tariff narrative from a margin risk story into a proof-of-execution story for institutional audiences.

Further reinforcing professional conviction, Anversa confirmed at the Goldman Sachs conference that Logitech’s $2 billion, three-year share repurchase program remains fully on track, signaling that management views the current price as an attractive entry point supported by a balance sheet holding $1.8 billion in cash.

Looking ahead, Logitech’s China-for-China strategy, installed base opportunity across 1.5 billion PCs globally, and aspiration to shift its B2B-B2C split toward 50-50 position the company to sustain 300 to 500 basis points of outperformance versus PC unit growth for the next three to five years regardless of macro conditions.

Wall Street’s Take on LOGN Stock

Logitech’s record Q3 non-GAAP operating income of $312 million, driven by the MX Master 4 launch and completed manufacturing diversification, directly strengthens the FY2026 earnings trajectory and validates accelerating EPS estimates heading into FY2027.

Underpinning that momentum, analysts project FY2026 revenue growing 6.2% to $4.8 billion alongside EPS expanding 16.2% to $5.6, confirming that Logitech’s margin recovery is accelerating rather than plateauing after two years of post-pandemic normalization.

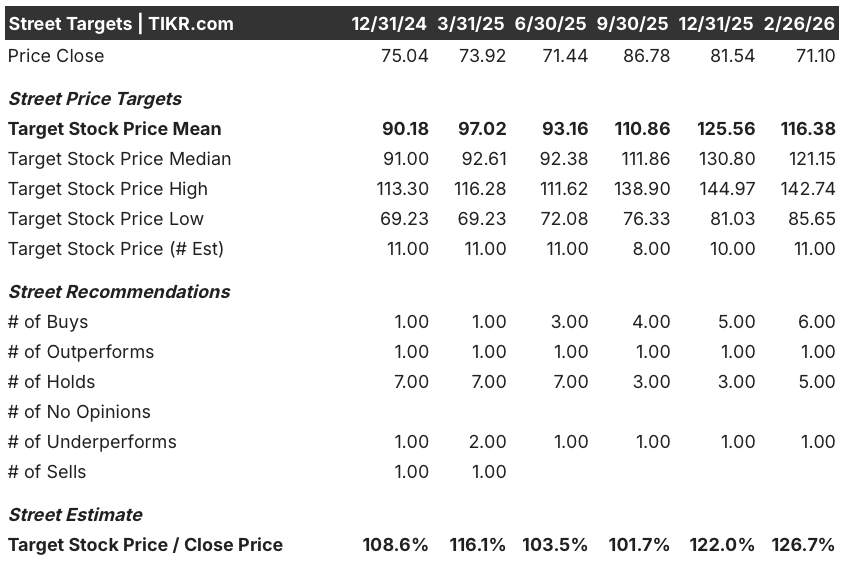

Wall Street currently reflects growing conviction, with 6 buys, 1 outperform, 5 holds, and 1 underperform, producing a mean price target of $116.4 that implies 26.7% upside from the February 26 close of $91.9, as analysts upgrade into earnings strength rather than fade it.

The spread between the analyst low target of $85.7 and the high of $142.7 is substantial, with the bull case hinging on sustained B2B video collaboration growth and China gaming momentum, while the bear case materializes if U.S. gaming demand and consumer spending deteriorate further.

What Does the Valuation Model Say?

Given Logitech’s 6.3% revenue CAGR and 15.3% net income margin embedded in the mid-case forecast, TIKR’s valuation model prices LOGN at $141.7, representing a 54.2% total return and an 11.2% annualized IRR through March 2030, a return profile that the Q3 execution record makes credible rather than optimistic.

The most consequential risk remains P/E multiple compression, with the model projecting a 6.4% annual P/E contraction in the mid-case, meaning Logitech must sustain EPS growth above 8% annually just to offset valuation headwinds and deliver meaningful price appreciation.

Overall, Logitech stock looks undervalued at $91.9 given 26.7% upside to the analyst mean target and an 11.2% annualized IRR in the base case, with the key variable to watch being whether Americas gaming demand recovers and B2B mix expansion continues driving margin upside through FY2027.

Should You Invest in Logitech International S.A?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LOGN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Logitech International S.A alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LOGN stock on TIKR for Free →