Key Takeaways:

- Market Resilience: Maintenance spending remains strong despite new pool construction dropping to ~60,000 units.

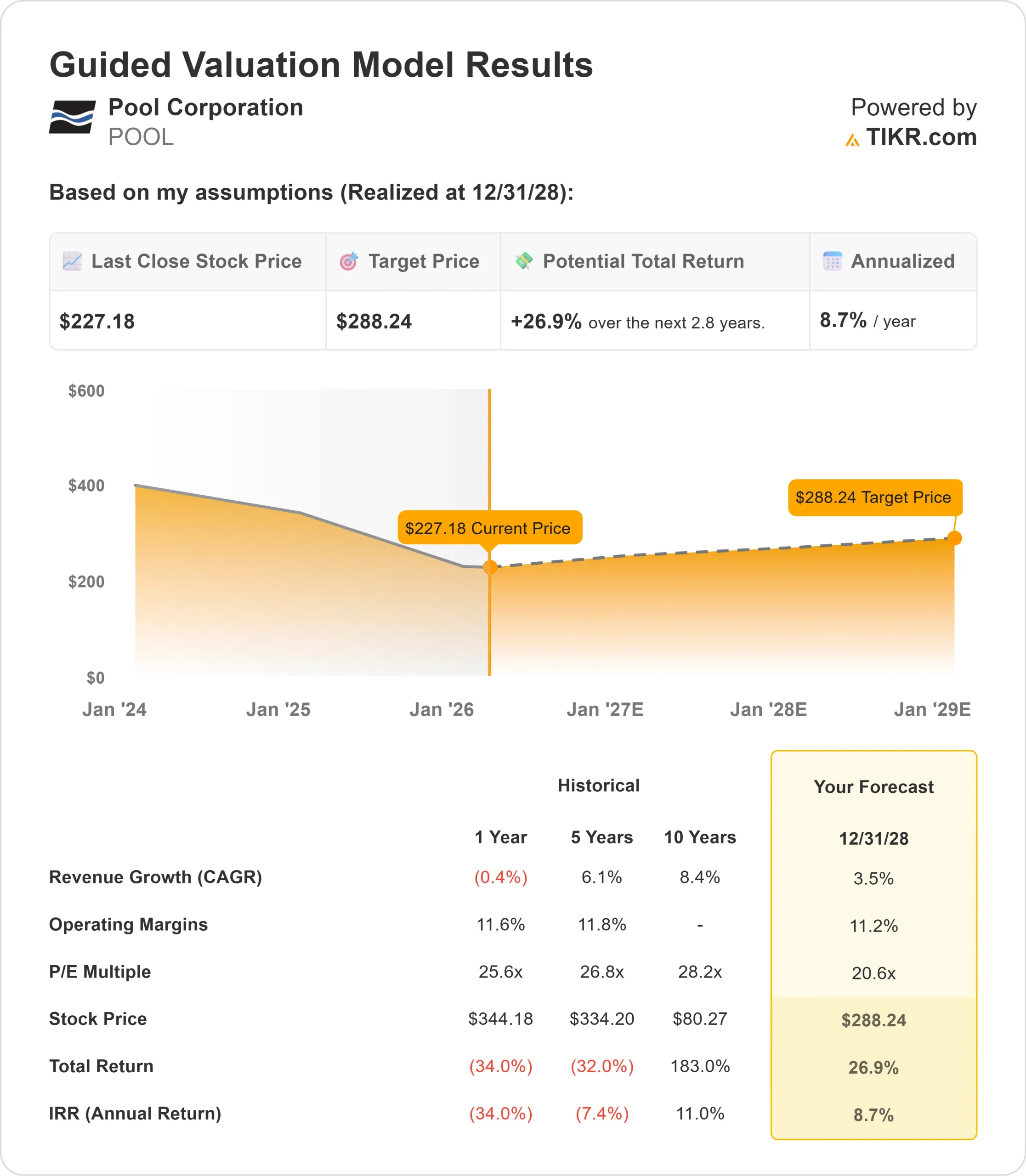

- Price Projection: Based on current execution, POOL stock could reach $288 by December 2028.

- Potential Gains: This target implies a total return of 27% from the current price of $227.

- Annual Return: Investors could see roughly 9% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Pool Corporation (POOL) navigated a challenging 2025 with revenue holding steady at $5.3 billion despite persistent headwinds in new pool construction. The company maintained its market leadership position while investing in digital capabilities and exclusive brands.

CEO Peter Arvan highlighted the resilience of maintenance spending even as new pool construction declined.

- Approximately 60,000 new pools were built in the U.S. during 2025, representing a mid-single-digit decline from the prior year and roughly half the pandemic peak.

- Despite industry challenges, Pool Corporation delivered 70 basis points of gross margin expansion in Q4, reaching 30.1%.

- This performance reflected disciplined pricing strategies, supply chain optimization, and growing sales of exclusive brands.

- The company’s digital platform, POOL360, reached 15% of total sales for the full year—an all-time high.

- During peak pool season, digital sales surged to 17% of revenue, demonstrating strong customer adoption of technology investments.

Management expects maintenance revenues to remain resilient in 2026, supported by the installed pool base.

The company projects low single-digit sales growth while continuing to invest in operational efficiency and customer experience.

See analysts’ full growth forecasts and estimates for POOL stock (It’s free) >>>

What the Model Says for Pool Corporation Stock

We analyzed Pool Corporation, the dominant distributor in the swimming pool industry, with growing opportunities in exclusive brands and digital platforms.

- The company benefits from predictable maintenance demand that accounts for roughly 64% of pool product sales.

- This recurring revenue base provides stability even during periods of weak discretionary spending on new pools and renovations.

- Pool Corporation’s exclusive brands and enhanced digital capabilities position the company to gain share.

- The POOL360 platform improves customer engagement while reducing cost to serve.

- Management’s focus on operational efficiency should drive margin improvement as recent facility investments mature.

Using a forecast of 3.5% annual revenue growth and 11.2% operating margins, our model projects the stock will rise to $288 within 2.8 years. This assumes a 20.6x price-to-earnings multiple.

That represents compression from Pool Corporation’s historical P/E averages of 25.6x (one year) and 26.8x (five years).

The lower multiple acknowledges near-term uncertainty about the timing of recovery in discretionary spending categories such as new pool construction and major renovations.

The real value lies in the company’s unmatched distribution network, growing exclusive brand portfolio, and ability to capture maintenance wallet share across an expanding installed base of pools.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for POOL stock:

1. Revenue Growth: 3.5%

Pool Corporation’s growth centers on maintaining stable maintenance demand and expanding market share through differentiated offerings.

The company expects approximately 60,000 new pools to be built in 2026, consistent with 2025 levels.

Maintenance activity should benefit from the cumulative installed base, while early signs suggest stabilization in renovation and remodel spending.

Digital platform investments are driving customer engagement, with POOL360 adoption creating competitive advantages.

Management expects to realize pricing benefits of 1% to 2% from vendor cost increases and pre-season inventory purchases.

The company’s exclusive brands, including National Pool Trends building materials, provide insulation against commodity pricing pressure in areas such as chemicals.

2. Operating margins: 11.2%

Pool Corporation has invested significantly in technology and distribution infrastructure over recent years.

These investments are now positioned to drive operational leverage as management focuses on capacity absorption rather than expansion.

- The company slowed facility openings to extract more value from existing locations.

- Technology upgrades and supply chain initiatives are generating measurable efficiency gains.

- Operating margins should benefit from better asset utilization across the 456 sales center network.

Management plans to open only 5 to 8 new locations in 2026, with an investment of $5 million, compared to a more aggressive expansion in prior years, allowing a focus on improving profitability at newer branches and underperforming locations.

3. Exit P/E Multiple: 20.6x

The market currently values Pool Corporation at 20.6x earnings. We maintain this multiple through our forecast period, given mixed near-term dynamics.

Uncertainty around the timing of recovery in new pool construction and major renovation projects weighs on the multiple.

However, the company’s dominant market position, recurring maintenance revenue, and successful execution on strategic initiatives support a premium valuation relative to typical distribution businesses.

As Pool Corporation demonstrates, it is improving returns on recent investments and maintaining market leadership; the company should command a valuation that reflects its competitive moat and growth opportunities.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

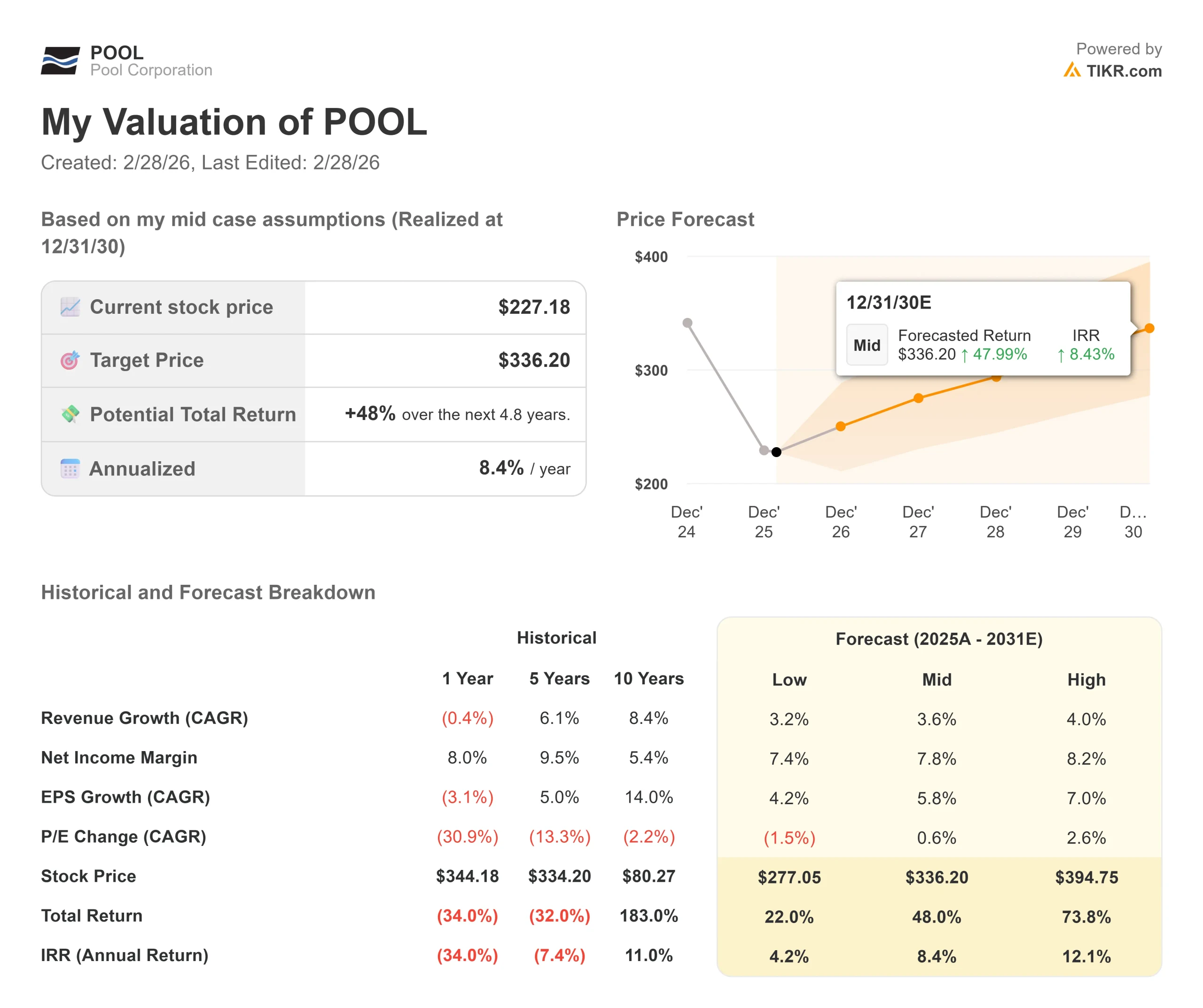

Swimming pool distributors face cycles in residential construction and consumer discretionary spending. Here’s how Pool Corporation stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 3.2% and net income margins compress to 7.4%, investors still see a 22% total return (4.2% annually)

- Mid Case: With 3.6% growth and 7.8% margins, we expect a total return of 48% (8.4% annually)

- High Case: If housing market recovery drives 4.0% revenue growth while Pool Corporation maintains 8.2% margins, returns could hit 74% total (12.1% annually)

See what analysts think about POOL stock right now (Free with TIKR) >>>

The range reflects execution on exclusive brand expansion, digital platform adoption, and operational efficiency gains.

In the low case, new pool construction remains depressed and competitive pressure intensifies.

In the high case, pent-up demand for pool projects materializes sooner than expected and the company successfully captures share through superior customer experience.

How Much Upside Does Pool Corporation Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!