Key Stats for Marriott Stock

- Past-Week Performance: -1.7%

- 52-Week Range: $205.4 to $370

- Current Price: $341.7

What Happened?

Marriott International‘s record 610,000-room pipeline signals a company accelerating into dominance, even as the stock pulls back to $341.73 from its 52-week high of $370.00.

Multiple executives including CEO Anthony Capuano filed share disposals on February 19, while Marriott simultaneously priced a $1.45B senior notes offering on February 20.

Q4 gross fee revenues grew 7% to $1.4B, driven by a 16% surge in incentive management fees to $239M and 8% growth in co-branded credit card fees.

The market increasingly re-rates Marriott from a traditional hotelier to a fee-generating loyalty and fintech platform, with co-branded credit card fees projected to surge 35% in 2026.

CEO Anthony Capuano stated on the Q4 earnings call that “there is an almost insatiable demand for luxury,” contextualizing Marriott’s record 114 luxury deals signed during 2025.

Jefferies analyst David Katz engaged directly with management on February 10, pressing on net unit growth investment strategy as Marriott targets 4.5% to 5% rooms growth in 2026.

With 271M Bonvoy members, a FIFA World Cup partnership, and Spain and India expansion accelerating, Marriott’s global loyalty ecosystem will prove increasingly difficult for competitors to replicate.

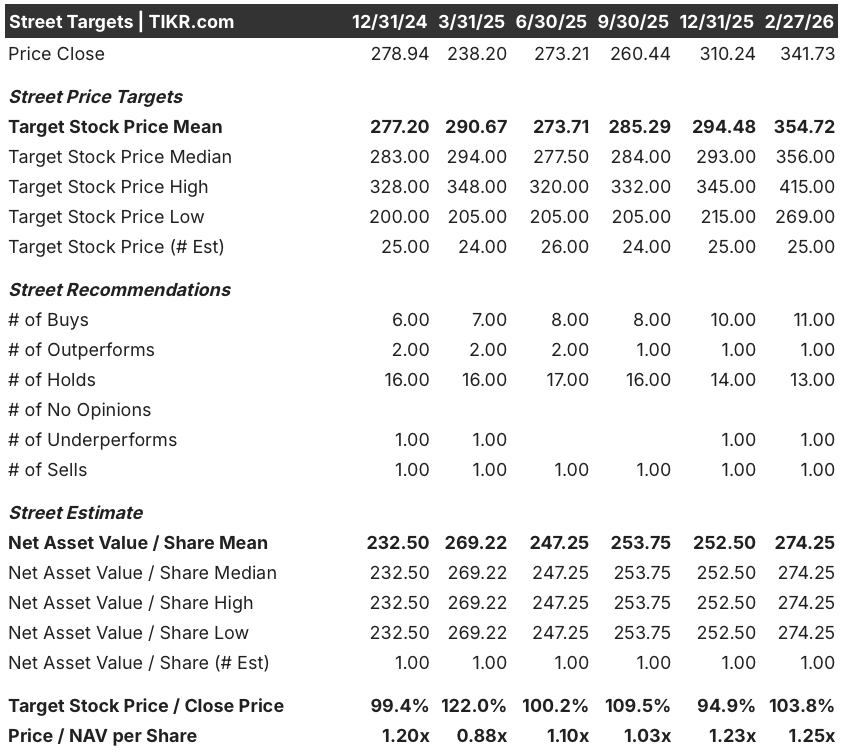

Wall Street’s Take on Marriott Stock

Marriott’s record 610,000-room pipeline and projected 13% to 15% adjusted EPS growth in 2026 directly confirm the fee revenue acceleration story is just beginning.

Revenue grew 4.3% in FY25 to $26.19B, while EBITDA expanded to $5.38B with margins rising to 20.6%, and FY26 estimates point to further expansion toward 21.1%.

Wall Street shows 11 buys, 1 outperform, 13 holds, 1 underperform, and 1 sell as of February 27, with a mean target of $354.72, implying 3.8% upside from $341.73.

Analysts set a low target of $269 and a high of $415, with the high requiring sustained credit card fee growth and World Cup RevPAR delivery above the 30 to 35 basis point guidance.

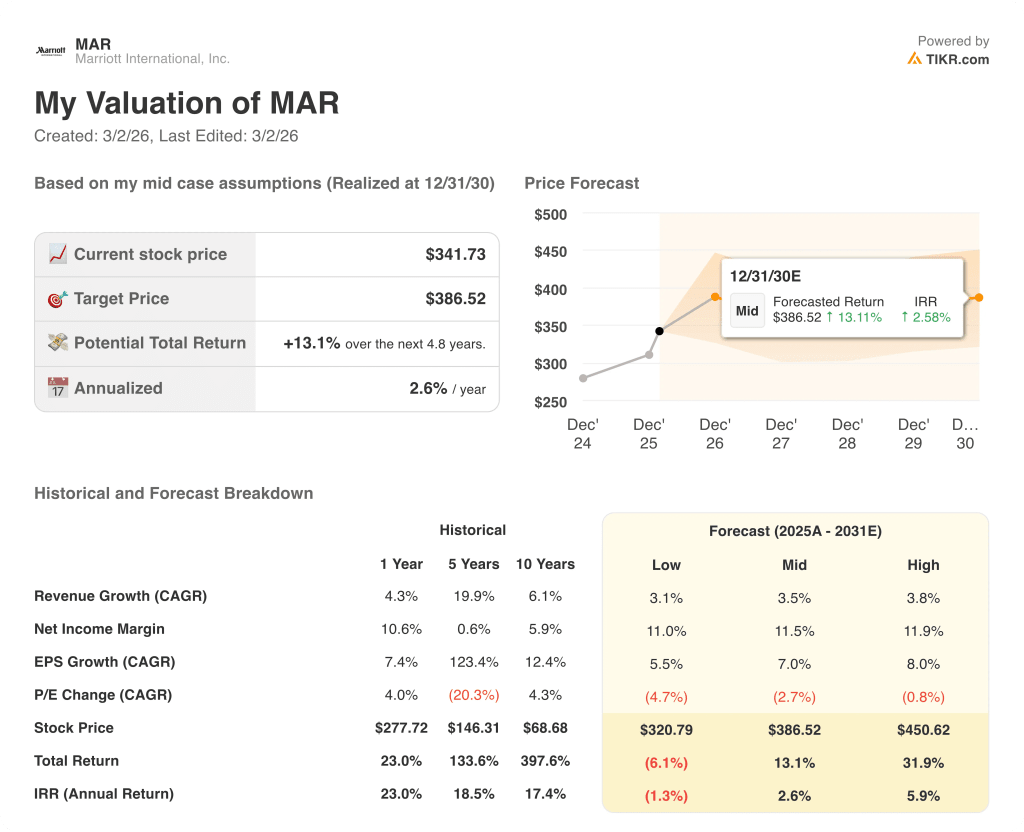

What Does the Valuation Model Say?

TIKR’s mid-case model targets $386.52 by December 31, 2030, delivering just 13.1% total return over 4.8 years. The 2.6% annualized IRR signals the market is pricing Marriott close to fair value today.

The market treats Marriott as a hotel operator, missing its transformation into a loyalty payments platform generating over $700M annually in co-branded credit card fees.

Furthermore, FY26 credit card fees alone are projected to surge 35%, a number no traditional hospitality multiple adequately captures.

Critically, management secured a contractual royalty rate increase with Chase and American Express, a structural earnings shift the current 13 holds on Wall Street have not yet rewarded.

If Greater China RevPAR stays flat and government travel remains 15% below prior levels, the 1.5% to 2.5% global RevPAR guidance breaks, directly compressing the $5.8B to $5.9B EBITDA target.

The March 12 J.P. Morgan Forum appearance by CEO Anthony Capuano will reveal whether new credit card deal negotiations with Chase and American Express are accelerating toward a 2026 close.

Marriott is fairly valued today but becomes genuinely compelling if the new credit card deals close in 2026, unlocking fee revenue the model has not yet priced.

Should You Invest in Marriott International, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MAR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marriott International, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MAR stock on TIKR for Free →

-via-Canva/@Aflo-Images-from-アフロ(Aflo)-via-Canva)