Key Takeaways:

- AI Infrastructure Boom: Data center revenue grew 38% year-over-year, driven by surging AI demand and optical interconnect leadership.

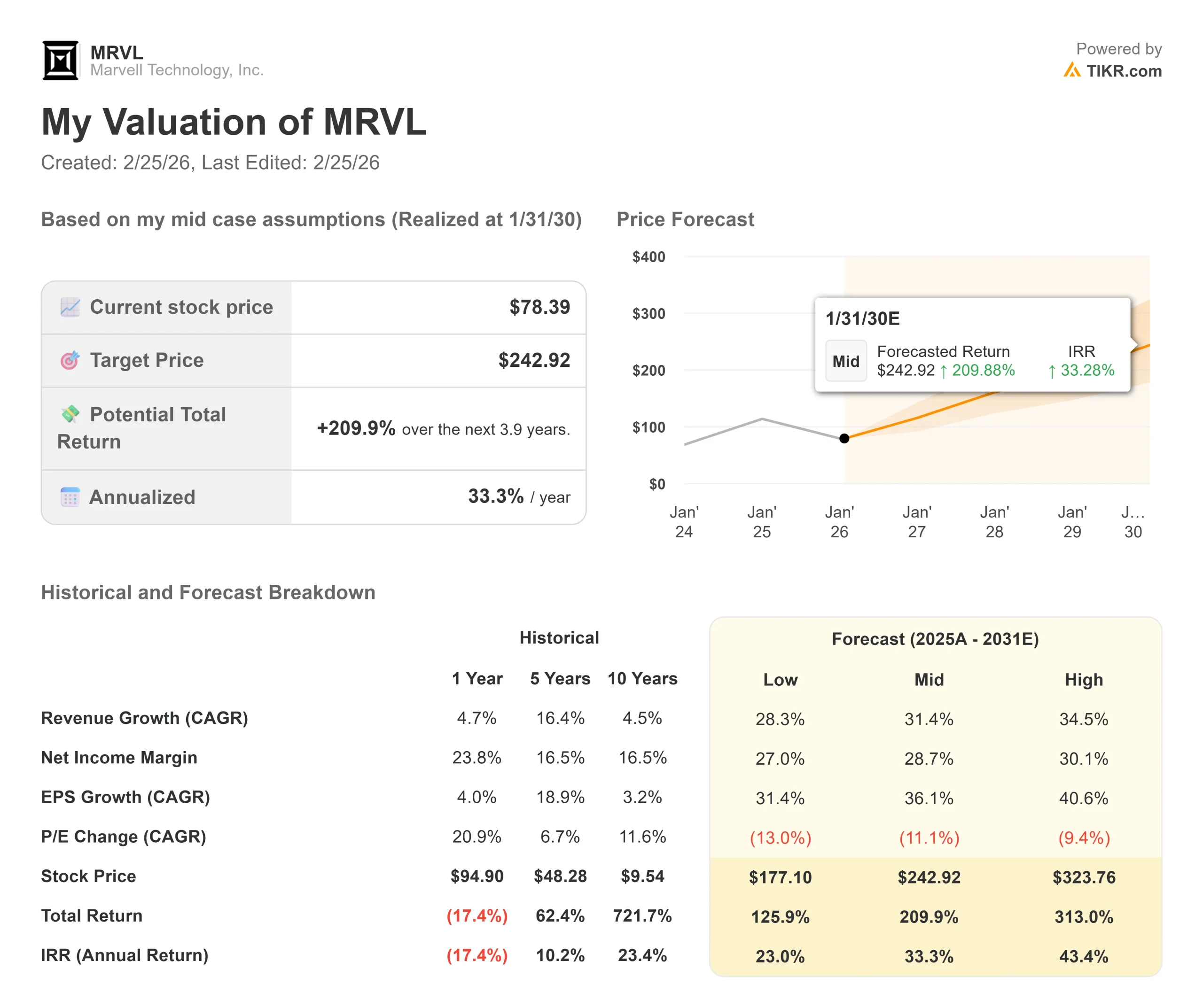

- Price Projection: Based on current execution, MRVL stock could reach $138 by January 2028.

- Potential Gains: This target implies a total return of 76% from the current price of $78.

- Annual Return: Investors could see roughly 34% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Marvell Technology (MRVL) delivered record third-quarter fiscal 2026 revenue of $2.08 billion, up 37% year-over-year, as CEO Matt Murphy outlined an aggressive growth strategy extending through 2029.

- The company raised its fiscal 2027 data center revenue growth forecast to over 25%, citing stronger cloud capital expenditure trends and accelerating demand across its portfolio.

- Murphy highlighted three key growth drivers.

- First, the interconnect business—representing half of data center revenue—continues outpacing cloud CapEx growth as hyperscalers deploy 1.6-terabit optical solutions.

- Second, the custom chip business expects at least 20% growth next year, backed by purchase orders for next-generation programs.

- Third, switching and storage revenue should grow 15%, accelerating from the prior 10% outlook.

- The company also announced the strategic acquisition of Celestial AI, bringing photonic fabric technology for next-generation scale-up interconnects.

- This positions Marvell to capture a $10 billion addressable market in optical interconnects by 2030, with Celestial AI expected to reach $500 million in annualized revenue by late fiscal 2028.

- Beyond fiscal 2027’s projected $10 billion in revenue, Murphy sees data center growth accelerating to 40% in fiscal 2028, driven by custom chip programs doubling and continued strength in optical interconnects.

See analysts’ full growth forecasts and estimates for MRVL stock (It’s free) >>>

What the Model Says for Marvell Technology Stock

We analyzed Marvell through its transformation into a comprehensive AI infrastructure provider with market-leading positions across data center networking, custom silicon, and optical interconnects.

The company benefits from structural tailwinds in AI deployment. Hyperscalers are building million-GPU clusters requiring massive bandwidth and low-latency connectivity.

Marvell’s electro-optics portfolio—spanning PAM DSPs, coherent solutions, and now photonic fabrics—addresses this need comprehensively.

The custom chip business provides significant upside. Marvell has secured 18 design wins for XPU and XPU-attach sockets, with several already in production.

The XPU-attach market alone offers line of sight to $2 billion in revenue by fiscal 2029, as hyperscalers deploy custom NICs and CXL memory expansion across their AI server fleets.

Management’s track record on acquisitions strengthens confidence. Previous deals including Inphi and Innovium proved transformational, with Inphi’s PAM technology becoming the industry standard for 800-gig and 1.6-terabit connectivity.

Using a forecast of 31.3% annual revenue growth and 36.1% operating margins, our model projects the stock will rise to $138 within 1.9 years. This assumes a 21.7x price-to-earnings multiple.

That represents compression from Marvell’s historical P/E averages of 24.9x (one year) and 31.7x (five years). The lower multiple reflects near-term execution risk as the company integrates Celestial AI and ramps multiple custom programs simultaneously.

The real value lies in Marvell’s positioning across every critical component in AI infrastructure—from optical interconnects and switching to custom accelerators—during a multi-year buildout cycle.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MRVL stock:

1. Revenue Growth: 31.3%

Marvell’s growth centers on expanding its AI infrastructure.

The company expects sequential revenue growth in each quarter of fiscal 2027, with the second half significantly stronger than the first.

Management’s visibility extends well beyond typical guidance horizons. Customers are providing multi-year capacity plans to ensure supply for their AI buildouts.

This enables Marvell to forecast 25% data center growth in fiscal 2027, with further acceleration in fiscal 2028.

The interconnect business continues to outgrow cloud CapEx, with next year’s growth expected to exceed 30%.

Marvell leads at 1.6 terabits with optimized 3-nanometer solutions already sampling, and has demonstrated 3.2 terabit technology for 2028 deployment.

2. Operating margins: 36.1%

Marvell has driven non-GAAP operating margin expansion to 36.3% in Q3, up 150 basis points sequentially.

CFO Willem Meintjes expects operating expenses to grow roughly half as fast as revenue in fiscal 2027, demonstrating significant operating leverage.

The company’s product mix favors margin expansion.

3. Exit P/E Multiple: 21.7x

The market values Marvell at 24.2x earnings. We assume the P/E will compress to 21.7x over our forecast period, below the five-year average of 31.7x.

This conservative multiple accounts for execution complexity as Marvell ramps the Celestial AI acquisition alongside multiple custom programs.

The photonic fabric technology represents unproven territory at a volume production scale, despite strong initial customer engagement.

As Marvell demonstrates consistent execution across its diversified growth drivers and Celestial AI progresses toward its $500 million revenue target, the multiple should re-rate higher toward historical averages.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Semiconductor companies face technology transitions and the risk of customer concentration. Here’s how Marvell stock might perform under different scenarios through January 2030:

- Low Case: If revenue growth moderates to 28.3% and net income margins compress to 27.0%, investors still see a 126% total return (23% annually).

- Mid Case: With 31.4% growth and 28.7% margins, we expect a total return of 210% (33% annually).

- High Case: If AI infrastructure acceleration drives 34.5% revenue growth while Marvell maintains 30.1% margins, returns could hit 313% total (43% annually).

See what analysts think about MRVL stock right now (Free with TIKR) >>>

The range reflects execution on custom chip ramps, successful Celestial AI integration, and the pace of AI infrastructure deployment.

In the low case, hyperscaler consolidation creates unexpected churn, or photonic fabric adoption takes longer than anticipated.

In the high case, AI capacity buildouts exceed current forecasts, custom attach rates surpass expectations, and Celestial AI achieves its revenue targets ahead of schedule.

How Much Upside Does Marvell Technology Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!