Key Stats for GE Aerospace Stock

- Past-Week Performance: +9%

- 52-Week Range: $159.4 to $346.8

- Current Price: $345.6

What Happened?

GE Aerospace (GE) is trading within pennies of its 52-week high of $346.80, surging 9% in a single week as a cascade of contract wins, from United Airlines ordering 300 GEnx engines to American Airlines locking in LEAP-1A engines through 2032, reframes this stock as a demand-constrained franchise with no meaningful competition in sight.

Driving the momentum further, the Defense Logistics Agency awarded GE Aerospace a contract on February 24 to manage J85 engine readiness for the U.S. Air Force’s T-38 fleet, partnering with Palantir to deploy AI-driven logistics, adding a high-visibility defense technology angle to an already powerful commercial narrative.

The mechanical case behind the rally is straightforward: GE Aerospace closed 2025 with $9.1 billion in operating profit, $7.7 billion in free cash flow, a record 1,800-plus LEAP deliveries, and a $190 billion backlog that grew nearly $20 billion in a single year, all while priority supplier input surged over 40% to unlock even faster output in 2026.

Beyond the numbers, the market is fundamentally re-rating GE Aerospace from a post-spin industrial recovery story into a compounding aerospace platform, one that already hit its 2028 margin target of 21% three years early and now guides to $10 billion in operating profit in 2026, two years ahead of its original spin-off projection.

Chairman and CEO Larry Culp stated on the Q4 2025 earnings call that “we expect to deliver mid-teens revenue growth between ’24 and ’26 compounded and $10 billion of profit in ’26 two years earlier than our outlook at spin,” underscoring that the company is consistently outpacing its own ambitious financial roadmap.

Moreover, Pratt & Whitney’s public supply failure with Airbus, forcing the planemaker to cut its A320neo production target to 70 to 75 jets per month on February 19, hands CFM International a structural competitive advantage, as GE Aerospace’s joint venture with Safran now powers 60% of the world’s most in-demand narrowbody aircraft family with no credible near-term substitute.

Over the next three to five years, GE Aerospace’s combination of a sold-out LEAP engine program, a Singapore MRO hub targeting 33% higher repair volume, $3 billion in annual R&D, and a defense book-to-bill above 2.0 positions the company to dominate both the commercial aftermarket supercycle and the next generation of U.S. combat propulsion programs simultaneously.

Wall Street’s Take on GE Aerospace Stock

With United Airlines ordering 300 GEnx engines, American Airlines locking in LEAP-1A engines through 2032, and a new Defense Logistics Agency contract secured on February 24, GE Aerospace enters 2026 with commercial and defense demand reinforcing each other in a way that makes forward revenue visibility unusually strong.

The fundamental case backs that momentum directly, as analysts estimate GE Aerospace will grow revenue 13.8% to $48.2 billion in 2026 while expanding EPS 16.6% to $7.4, building on a 2025 base where operating profit already hit $9.1 billion and free cash flow reached $7.7 billion.

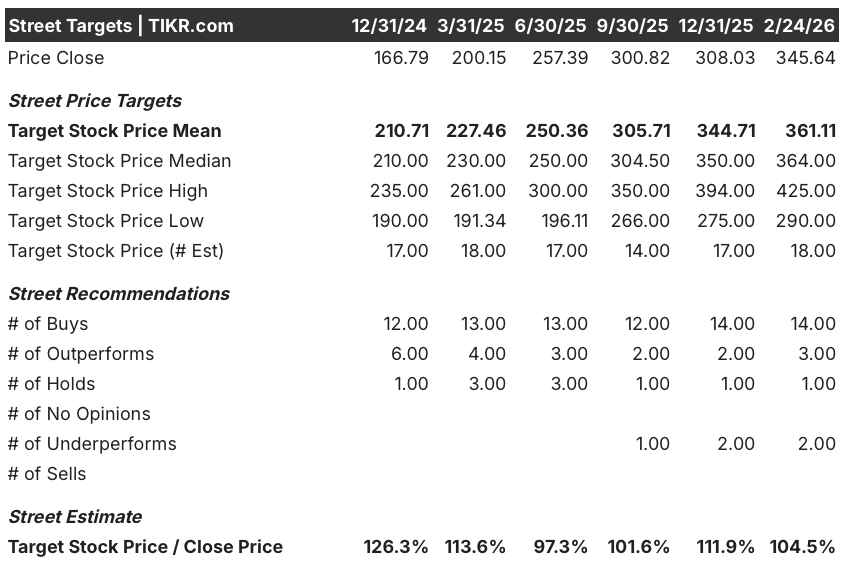

Wall Street stands firmly behind the stock, with 14 buy ratings and a mean price target of $361.1 among 18 analysts as of February 24, implying modest upside of 4.5% from current levels as the stock trades within reach of consensus.

The spread between the Street’s low target of $290.0 and its high of $425.0 reflects real disagreement about how fast GE Aerospace can scale LEAP production and whether the commercial aftermarket supercycle sustains its current pace through the end of the decade.

What Does the Valuation Model Say?

Against a backdrop of a $190 billion backlog, sold-out engine slots, and Pratt & Whitney’s public supply failure handing CFM a structural advantage, a TIKR mid-case valuation model prices GE at $522.9 per share by December 2030, implying a 51.3% total return and an 8.9% annualized IRR from today’s price.

The primary risk is margin pressure from GE9X program losses expected to double in 2026, a declining spare engine ratio, and rising corporate costs projected at $1.2 billion to $1.3 billion, all of which will weigh on CES margins even as services revenue grows.

At current levels, GE Aerospace looks fairly valued relative to near-term Street consensus but meaningfully undervalued on a through-cycle basis, given that its $190 billion backlog, LEAP profitability inflection, and defense growth have not yet fully materialized in reported earnings.

Should You Invest in GE Aerospace?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE Aerospace alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GE stock on TIKR for Free →