Key Takeaways:

- AI Innovation: New CEO Chris Young brings Microsoft AI expertise to transform tax compliance workflows.

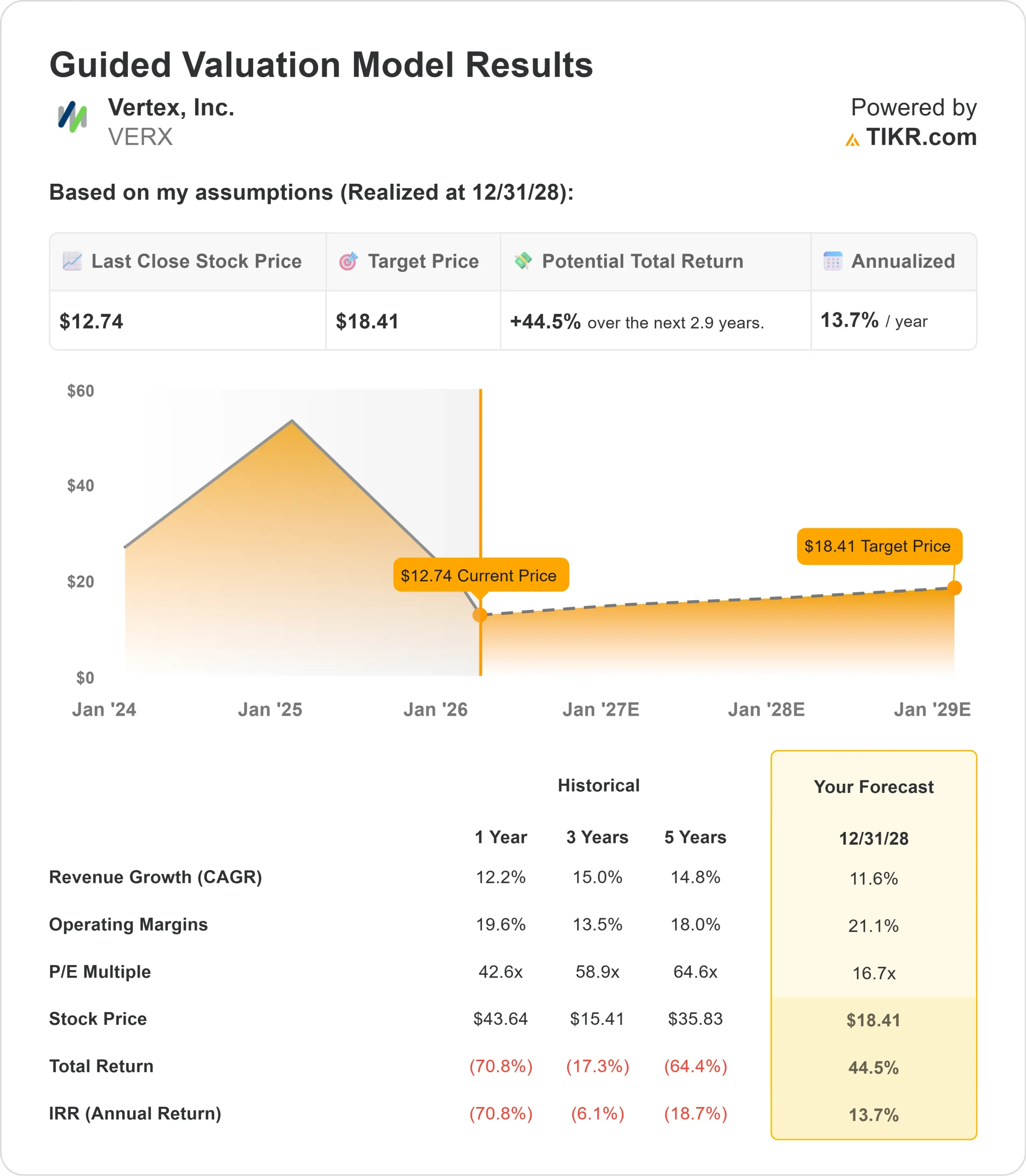

- Price Projection: Based on current execution, VERX stock could reach $18.41 by December 2028.

- Potential Gains: This target implies a total return of 44.5% from the current price of $12.74.

- Annual Return: Investors could see roughly 13.7% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Vertex (VERX) delivered fourth quarter 2025 revenue of $194.7 million, meeting guidance expectations, while adjusted EBITDA exceeded the high end at $42.5 million.

New CEO Chris Young highlighted both challenges and opportunities during his first earnings call.

- For the full year, the company achieved 12.2% revenue growth alongside solid profitability.

- The company faced lower entitlement growth and higher customer attrition in 2025, concentrated primarily in smaller accounts averaging under $50,000 in annual revenue. However, competitive losses remain modest, and Vertex continues winning more business from competitors than it loses.

- The company’s e-invoicing business exceeded expectations in its first year, with cross-sells increasing customer revenue by an average of over 20%.

- New product offerings, such as smart categorization, are gaining traction with marquee six-figure wins in retail.

- Vertex serves over 60% of the Fortune 500, providing mission-critical tax calculation and compliance across jurisdictions.

- Young emphasized that indirect tax compliance is “rule dense, data heavy, and highly repetitive” – exactly the type of work suited for AI transformation.

The company’s embedded position in customer workflows and revenue-based pricing model provides advantages as AI adoption accelerates.

See analysts’ full growth forecasts and estimates for VERX stock (It’s free) >>>

What the Model Says for Vertex Stock

We analyzed Vertex through its transformation into an AI-first tax compliance platform with expanding global capabilities.

The company benefits from structural tailwinds. Enterprise customers are consolidating tax solutions, often standardizing on Vertex after using competitors in parts of their business.

E-invoicing mandates are proliferating globally, with Belgium launching in January 2026, followed by France and Germany.

- Vertex now covers 39 countries for e-invoicing, up significantly from earlier positioning.

- The combined VAT calculation and e-invoicing platform is unique in the marketplace, creating cross-sell opportunities within the installed base.

- Young’s AI strategy focuses on automating manual workflows like product SKU categorization and returns processing.

- Smart categorization already secured several six-figure retail wins, with plans to expand across additional industries.

Using a forecast of 11.6% annual revenue growth and 21.1% operating margins, our model projects the stock will rise to $18.41 within 2.9 years. This assumes a 16.7x price-to-earnings multiple.

That represents compression from Vertex’s historical P/E averages of 42.6x (one year) and 58.9x (three years).

The lower multiple acknowledges near-term headwinds from retention challenges and the execution required to accelerate growth.

The real value lies in capturing the AI transformation opportunity while expanding e-invoicing globally. Management expects to restore accelerating growth through new product innovation and improved customer success coverage.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for VERX stock:

1. Revenue Growth: 11.6%

Vertex’s growth centers on proven land-and-expand motion with enterprise customers.

New logo revenue grew 20% in 2025, including competitive takeaways and customers switching from homegrown solutions.

E-invoicing provides meaningful acceleration potential. Initial deals are mid- to high five figures but serve as launching pads for full-suite adoption.

Cross-sells are increasing existing customer revenue by an average of over 20%.

Smart categorization addresses a clear pain point: retail customers pay six figures to automate SKU mapping. Expansion into additional industries broadens the addressable market.

2. Operating margins: 21.1%

Vertex expanded adjusted EBITDA margins to 21.6% in 2025 while making significant R&D investments in ecosio and AI.

Management expects margin improvement as these investments mature and generate returns.

The shift toward AI-powered automation should drive efficiency both internally and for customers.

Young’s focus on speed and execution aims to deliver more value while maintaining disciplined cost management.

3. Exit P/E Multiple: 16.7x

The market currently values Vertex at 17.3x earnings. We assume modest compression to 16.7x over our forecast period.

Near-term uncertainty around retention metrics and execution on the growth acceleration plan weighs on the multiple.

As Young demonstrates progress in AI innovation and e-invoicing expansion, the company should command a premium for its market leadership.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

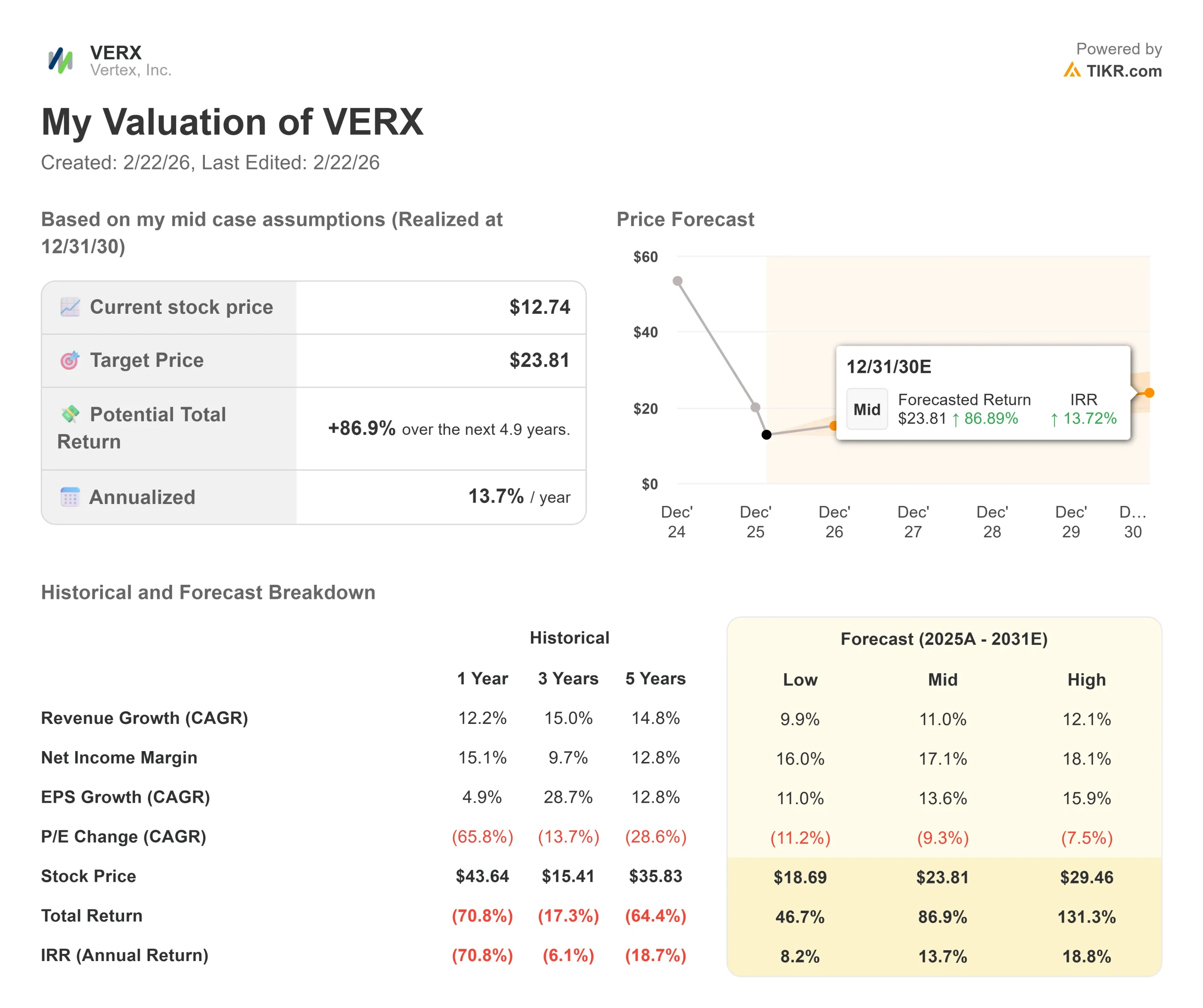

SaaS companies face execution risk in product innovation and customer retention. Here’s how Vertex stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 9.9% and net income margins compress to 16.0%, investors still see a 46.7% total return (8.2% annually).

- Mid Case: With 11.0% growth and 17.1% margins, we expect a total return of 86.9% (13.7% annually).

- High Case: If AI adoption accelerates, driving 12.1% revenue growth while Vertex maintains 18.1% margins, returns could hit 131.3% total (18.8% annually).

See what analysts think about VERX stock right now (Free with TIKR) >>>

The range reflects execution on AI product development, success navigating customer consolidation, and e-invoicing’s ability to capture global mandate-driven demand.

In the low case, retention challenges persist and AI innovation fails to generate meaningful revenue.

In the high case, smart categorization expands rapidly across industries, e-invoicing accelerates faster than anticipated, and AI-powered automation drives significant margin expansion.

How Much Upside Does Vertex Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!