Key Takeaways:

- E-commerce Expansion: GMV grew 35% in Brazil and Mexico, driven by lower shipping thresholds and improved value proposition.

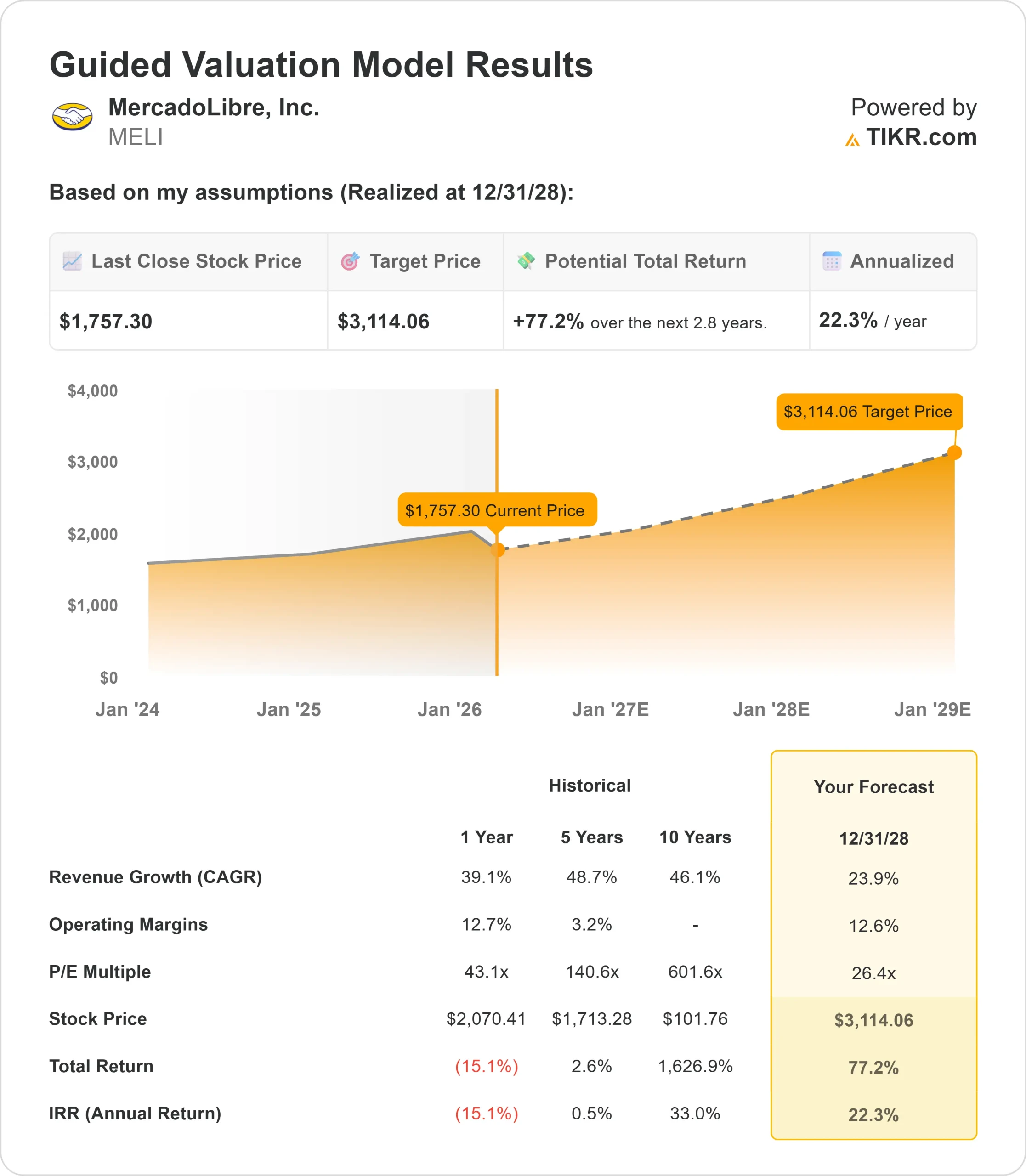

- Price Projection: Based on current execution, MELI stock could reach $3,114 by December 2028.

- Potential Gains: This target implies a total return of 77% from the current price of $1,757.

- Annual Return: Investors could see roughly 22% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

MercadoLibre (MELI) delivered impressive Q4 2025 with net revenue growth of 45% year-over-year. The company raised its full-year income from operations growth to 22%, demonstrating the strength of its ecosystem approach.

CFO Martin de los Santos emphasized that strategic investments are driving growth in both commerce and fintech.

- The decision to lower Brazil’s free shipping threshold accelerated purchase frequency and attracted new buyers, while the logistics network absorbed increased volumes with productivity gains.

- AI is transforming multiple business areas. In advertising, AI-powered bidding algorithms and automated campaign tools generated 67% revenue growth.

- The company’s Mercado Pago AI assistant now resolves 87% of customer interactions without human support, handling everything from credit card management to transfers.

- The fintech business reached a milestone, with Mercado Pago achieving the leading Net Promoter Score in Brazil, Mexico, Argentina, and Chile.

- Monthly active users grew by nearly 30% over 10 consecutive quarters.

- The credit portfolio almost doubled to $12.5 billion, including 3 million new credit cards issued in Q4 alone.

Despite strong fundamentals across commerce, fintech, and advertising, MercadoLibre trades at $1,757, offering substantial upside for investors who recognize the company’s dominance in underpenetrated Latin American markets.

See analysts’ full growth forecasts and estimates for MELI stock (It’s free) >>>

What the Model Says for MercadoLibre Stock

We analyzed MercadoLibre through its dual growth engines: marketplace expansion and financial services penetration in Latin America, where both e-commerce and digital payments remain significantly behind developed markets.

The commerce business benefits from multiple catalysts. Brazil’s GMV accelerated from 29% growth in Q2 to 35% in Q4, while items sold jumped 45%.

Mexico showed similar momentum with 35% GMV growth.

These gains came from deliberate investments in free shipping, which management views as essential for capturing long-term market share in a region where online retail penetration remains low.

The fintech opportunity is equally compelling. Credit card issuance accelerated from 1.5 million in Q2 to nearly 3 million in Q4, expanding across Brazil, Mexico, and the newly launched Argentina program.

Older credit card cohorts in Brazil are already profitable at the NIMAL level, validating the business model as it scales.

Using a forecast of 23.9% annual revenue growth and 12.6% operating margins, our model projects the stock will rise to $3,114 within 2.8 years. This assumes a 26.4x price-to-earnings multiple.

That represents significant compression from MercadoLibre’s historical P/E averages of 43.1x (one year) and 140x (five years). The lower multiple accounts for near-term margin pressure from investments in shipping, credit cards, cross-border trade, and first-party retail.

The real value lies in capturing structural growth as Latin America transitions from cash-based offline commerce to digital marketplaces and financial services.

Management deliberately prioritizes long-term market share over short-term margins, a strategy that has delivered 28 consecutive quarters of revenue growth above 30%.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MELI stock:

1. Revenue Growth: 23.9%

MercadoLibre’s growth centers on accelerating e-commerce adoption and fintech penetration across Latin America.

- The company delivered 45% revenue growth in Q4, with Brazil showing particular strength as items sold grew 45% and GMV increased 35%.

- Advertising represents an emerging high-margin revenue stream, growing 67% as AI-powered tools improve advertiser returns and drive higher budget allocation.

- Management sees substantial runway as ads currently represent a small percentage of GMV compared to global peers.

- The credit business is scaling rapidly, with the portfolio nearly doubling to $12.5 billion.

As the credit card program matures in Brazil and expands in Mexico and Argentina, it creates recurring revenue through interest income and strengthens ecosystem engagement.

2. Operating margins: 12.6%

MercadoLibre compressed margins by 5-6 percentage points through deliberate investments in free shipping, credit card expansion, cross-border trade, and first-party retail.

Management views these as foundational to long-term growth rather than as inefficiencies.

The company demonstrated operating leverage potential, with logistics absorbing higher volumes while reducing unit costs by 11% in Brazil.

As scale increases and newer initiatives like credit cards mature, margins should expand from current levels.

3. Exit P/E Multiple: 26.4x

The market values MercadoLibre at 30.4x earnings. We assume the P/E will compress to 26.4x over our forecast period, reflecting near-term margin investments and execution risk as the company scales multiple business lines simultaneously.

However, as investments in shipping and credit cards demonstrate, returns are realized, and advertising scales to higher penetration, the company should command a premium multiple.

The combination of strong unit economics, market leadership across Latin America, and multiple high-growth business segments supports valuation expansion as the investment cycle matures.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

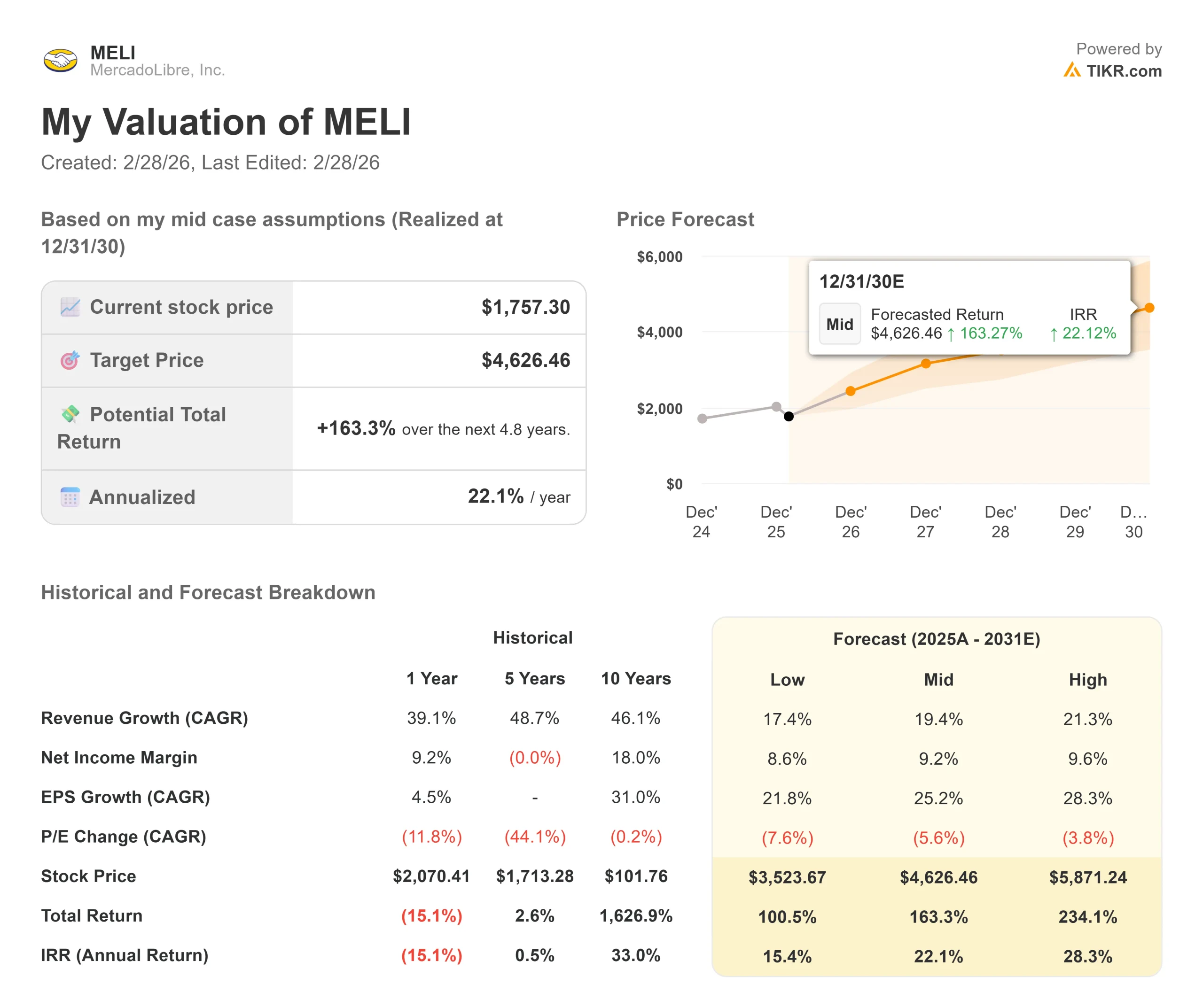

Latin American e-commerce and fintech companies face execution challenges and macroeconomic volatility. Here’s how MercadoLibre stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 17.4% and net income margins compress to 8.6%, investors still see a 100.5% total return (15.4% annually).

- Mid Case: With 19.4% growth and 9.2% margins, we expect a total return of 163.3% (22.1% annually).

- High Case: If e-commerce acceleration and credit scaling drive 21.3% revenue growth while MercadoLibre achieves 9.6% margins, returns could hit 234.1% total (28.3% annually).

See what analysts think about MELI stock right now (Free with TIKR) >>>

The range reflects execution on free shipping investments, credit card portfolio quality, advertising penetration, and the company’s ability to expand margins while maintaining growth momentum across Brazil, Mexico, Argentina, and smaller markets.

How Much Upside Does MercadoLibre Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!