Key Stats for Monolithic Power Systems Stock

- Past-Week Performance: -5%

- 52-Week Range: $438.9 to $1,256.7

- Current Price: $1,142.7

What Happened?

Monolithic Power Systems (MPS) posted record Q4 revenue of $751.2 million, up 20.8% year-over-year, yet its stock sits at $1,142.7, nearly 9% below its 52-week high of $1,256.2, creating a compelling entry gap.

The February 27 restatement announcement for 2024 and 2025 financials introduced near-term uncertainty, pressuring shares down 3.2% on the day and rattling near-term sentiment across the investor base.

Beneath the restatement noise, MPS delivered full-year revenue of $2.8 billion, up 26.4%, with non-Enterprise Data end markets collectively surging over 40%, proving the company’s diversification engine is firing on all cylinders.

Still, the market is actively recalibrating its view of MPS, shifting from a traditional analog chipmaker narrative toward a full AI infrastructure systems provider, as optical modules, DDR5 power, and 800-volt data center solutions expand its addressable market.

Outgoing CFO Bernie Blegen stated on the Q4 earnings call that “whereas last quarter, I talked about a range of between 30% and 40%, maybe I can increase that to a floor of 50% growth,” as Enterprise Data backlog extended visibly into Q2 and Q3 of 2026.

Further reinforcing institutional conviction, BlackRock’s iShares A.I. Innovation and Tech Active ETF holds MPS as a core position within its $8.8 billion fund, which has attracted $7.9 billion in fresh capital over the past 12 months.

Over the next 3 to 5 years, MPS is positioning itself as the dominant power solutions architect for AI infrastructure, with design wins across all major hyperscalers, a $4.0 billion secured capacity base, and a product roadmap spanning silicon carbide, GaN, and module-level systems integration.

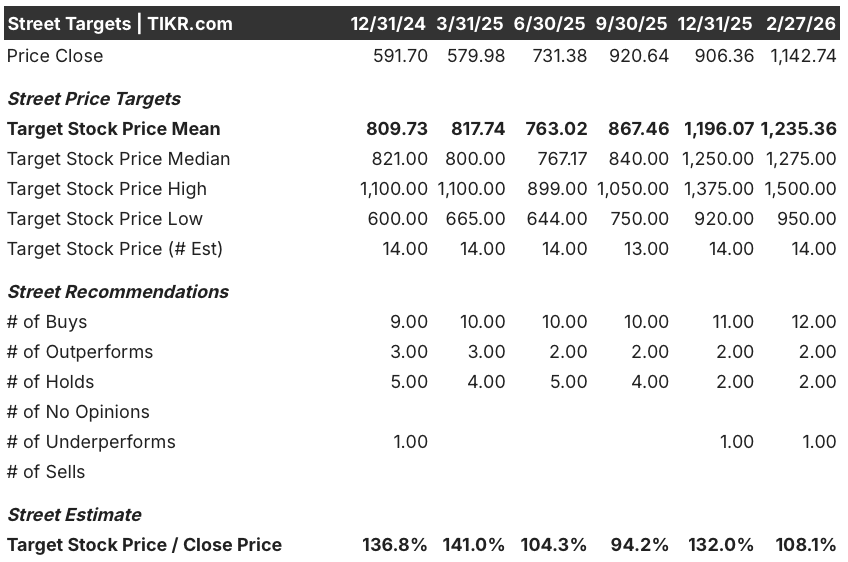

Wall Street’s Take on MPWR Stock

MPS’s February 27 restatement announcement rattled near-term sentiment, but its record Q4 revenue of $751.2 million and extending backlog confirm the underlying growth engine remains structurally intact.

The fundamental case stands firmly on its own: consensus estimates project FY 2026 revenue of $3.39 billion, up 21.4%, with normalized EPS growing 21.1% to $21.52, sustaining a decade-long compounding track record.

Wall Street currently carries 12 buys, 2 outperforms, 2 holds, and 1 underperform, with a mean price target of $1,235.4, implying 8.1% upside from the February 27 close of $1,142.7, reflecting analysts holding conviction through restatement noise.

The analyst target range spans $950.0 on the low end to $1,500.0 on the high end, with the upside scenario hinging directly on Enterprise Data delivering the 50%-plus growth management guided, while the downside reflects restatement overhang and macro uncertainty compressing multiples.

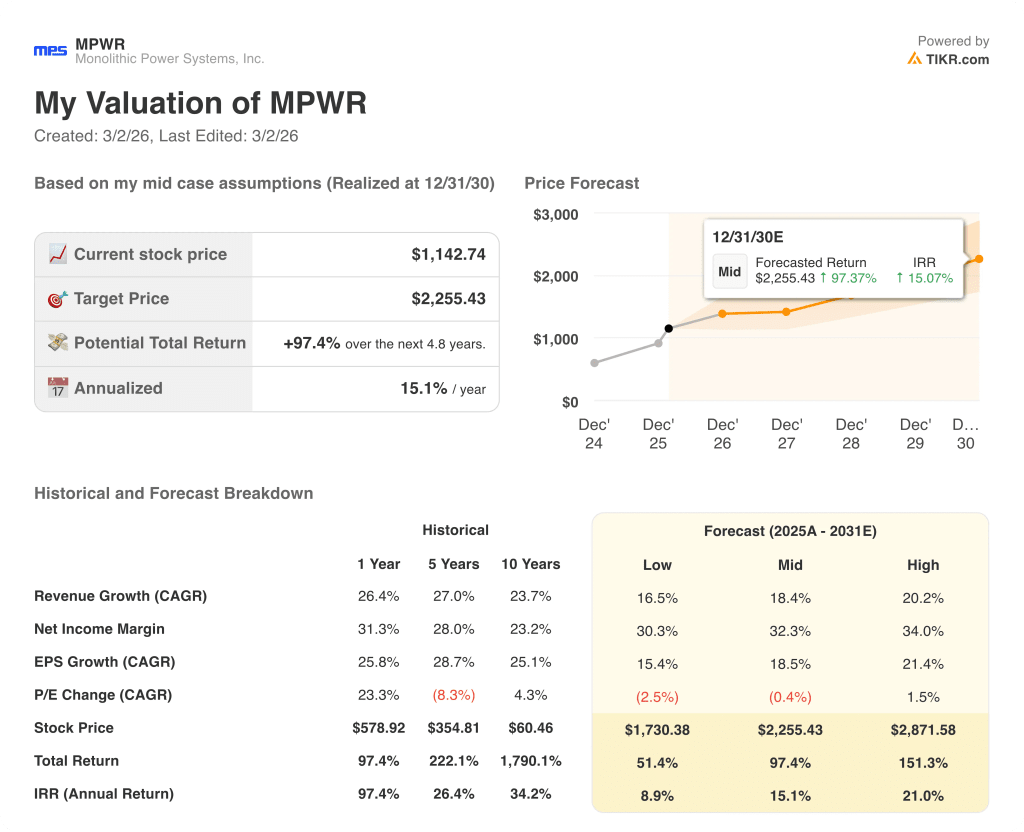

What Does the Valuation Model Say?

TIKR’s mid-case valuation model targets $2,255.4 by December 2030, implying a 97.4% total return and a 15.1% IRR from current levels, a gap the market appears to be ignoring entirely.

The market is pricing MPS as a restatement risk story, yet its 10-year revenue CAGR of 23.7% and 14 consecutive years of growth argue for a structurally premium valuation.

Normalized net income margins held at 30.8% in FY 2025 and are forecast to expand to 31.3% in FY 2026, directly contradicting any bear narrative around deteriorating profitability.

Management’s design win sweep across all major hyperscaler customers, combined with backlog extending into Q3 2026, signals this is a misunderstood re-rating story, not a broken one.

The restatement of both FY 2024 and FY 2025 financials carries real downside risk: if it reveals material earnings quality issues, it could invalidate the normalized EPS growth trajectory entirely.

The Q1 2026 earnings call, expected late April, will be the single most important event to watch, as it will either confirm or shatter the 50%-plus Enterprise Data growth floor.

MPS is undervalued at current levels, with a 15.1% annualized return model and 14 consecutive growth years behind it, but the restatement resolution in late April is the only gate that matters now.

Should You Invest in Monolithic Power Systems, Inc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MPWR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Monolithic Power Systems, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MPWR stock on TIKR for Free →