Key Stats for Cognizant Technology Stock

- Past-Week Performance: -1%

- 52-Week Range: $60 to $87

- Current Price: $64.4

What Happened?

Cognizant Technology Solutions (CTSH) stock closed at $64.43 last Friday, sitting 26% below its 52-week high of $87.03, yet its FY2025 revenue of $21.1 billion and record Q4 bookings reframe this dip as a disconnect between price and fundamentals.

The February 9 research roundup showed Jefferies cutting its price target to $90 from $100, yet that $90 floor still implies 40% upside from current levels, signaling that even the most cautious institutional voice sees significant undervaluation.

Driving that conviction is Cognizant’s Q4 engine: 12 deals each exceeding $100 million in TCV, two mega-deals, and a single contract worth over $1 billion, pushing large-deal TCV 60% above the prior-year quarter.

Beyond the deal wins, the market is actively re-rating Cognizant from a legacy IT services integrator to an AI builder, with fixed-price and transaction-based work now exceeding 50% of revenue, up sharply from 41% three years ago.

CEO Ravi Kumar S. stated on the Q4 earnings call that “we can own the outcomes, we can make this a platform play, we can make it nonlinear cost and nonlinear revenue,” contextualizing Cognizant’s shift toward outcome-based agentic contracts across its BPO and engineering practices.

Further supporting that re-rating, Cognizant secured a position on the Missile Defense Agency’s SHIELD program through Belcan, an indefinite-delivery contract with a $150 billion ceiling value, adding a high-margin government revenue stream to its portfolio.

Looking three to five years out, Cognizant’s partnerships with Anthropic, Google Cloud, Microsoft, and Palantir position it as the enterprise bridge for a $4.5 trillion AI labor productivity opportunity that no single technology vendor can capture alone.

Wall Street’s Take on CTSH Stock

Cognizant’s expanded partnerships with Anthropic, Google Cloud, and Daimler Truck directly support the Street’s FY2026 revenue estimate of $22.4 billion, a 5.9% increase that depends on exactly this kind of large-deal momentum accelerating through the year.

The fundamental case earns its conviction: FY2025 EBITDA grew 9.1% to $3.9 billion, EBIT margins expanded to 15.8%, and FY2026 estimates project further EBITDA growth of 7.5% alongside EPS of $5.66, up 7.1% year-over-year.

Wall Street currently shows 10 buys, 3 outperforms, and 14 holds against zero sells, with a mean price target of $90.20 that implies 40% upside from $64.43, suggesting analysts are holding conviction firmly into a significant pullback rather than chasing strength.

The gap between the $75.00 low target and $108.00 high target is wide enough to demand attention, with the low scenario reflecting stalled discretionary spending recovery and the high scenario hinging on large-deal ramp acceleration in Q2 and Q3.

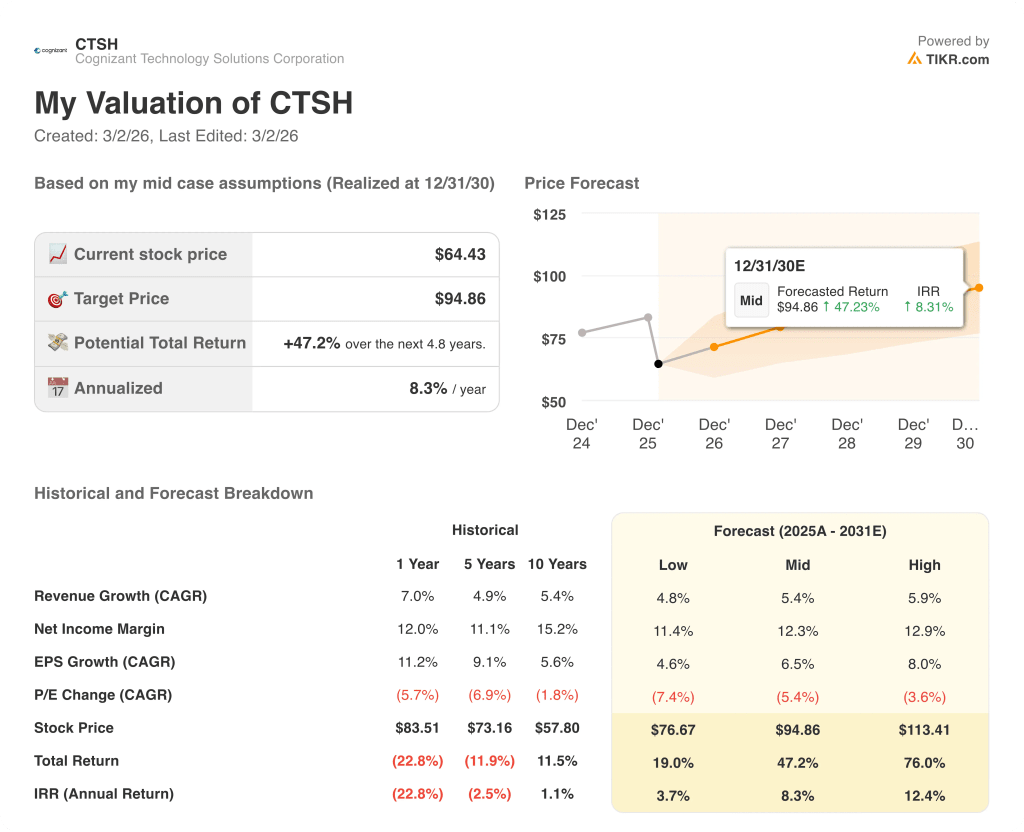

What Does the Valuation Model Say?

The valuation model prices CTSH at $94.9 by December 2030, implying a 47.2% total return and an 8.3% annualized IRR from current levels, a compelling gap the market has not yet closed.

The market is pricing CTSH as though AI disrupts its business model, yet BPO revenue just grew 9% year-over-year for the third consecutive year. That single number directly contradicts the disruption narrative driving the selloff.

Meanwhile, fixed-price and outcome-based contracts now represent over 50% of revenue, structurally protecting margins in ways the traditional time-and-materials model never could.

Management’s commitment to 20,000 India campus hires in 2026 signals cost pyramid expansion that analysts expect to drive further operating margin improvement toward the guided 15.9% to 16.1% range.

The primary risk is that organic revenue growth, guided at approximately 3.8% at the midpoint, fails to accelerate in the second half if discretionary spending stays compressed across Communications, Media, and Technology clients.

The March 3 Morgan Stanley TMT Conference presentation by CFO Jatin Dalal will be the first major opportunity to hear updated deal pipeline commentary and early Q1 signals.

CTSH is undervalued at $64.43 with a 40% gap to the analyst mean target and a proven large-deal engine that the current price simply does not reflect.

Should You Invest in Cognizant Technology Solutions Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CTSH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cognizant Technology Solutions Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CTSH stock on TIKR for Free →