Key Takeaways:

- Digital Payments Growth: Merchant Solutions organic revenue grew 6% in 2025, driven by Clover platform expansion.

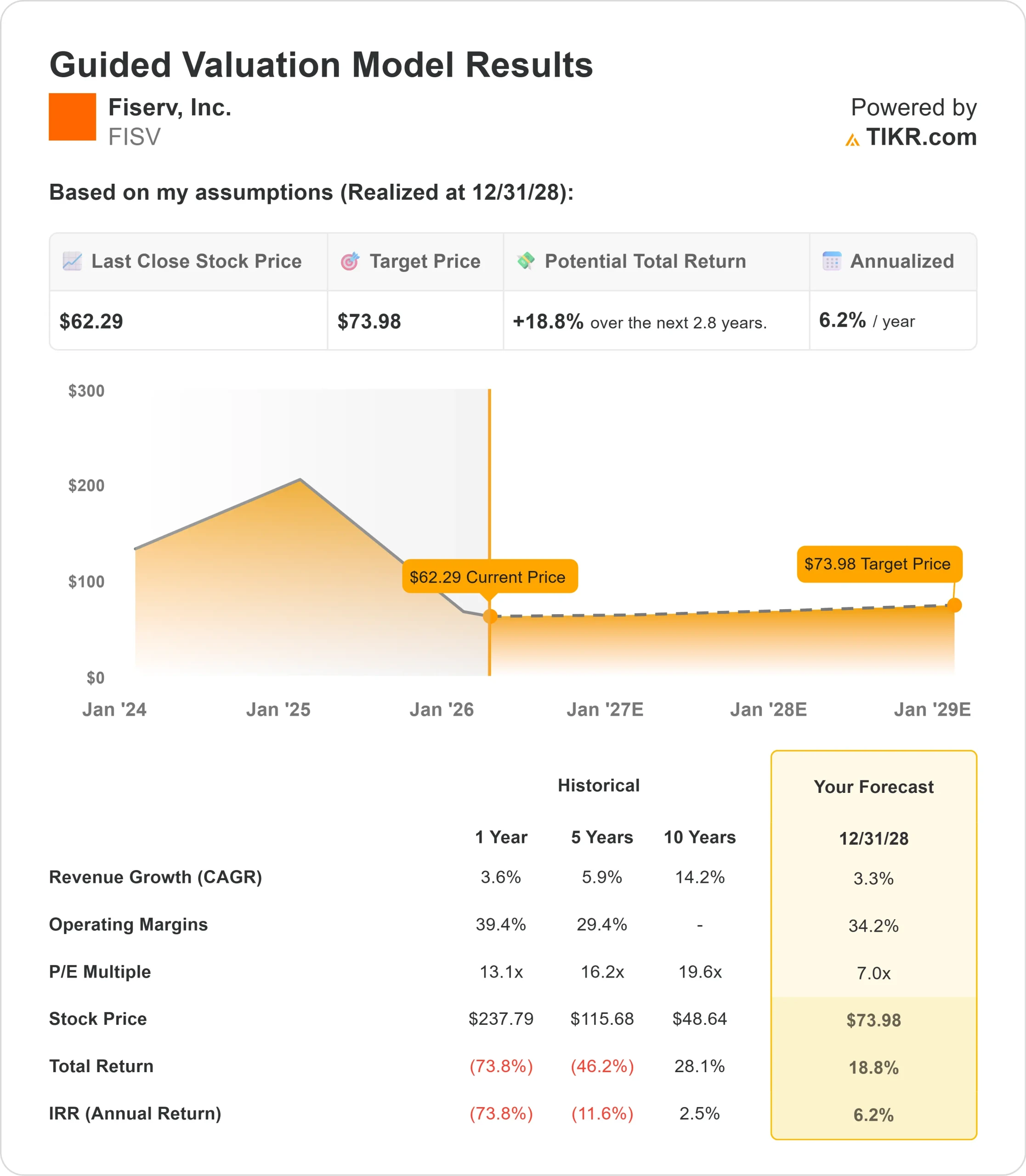

- Price Projection: Based on current execution, FISV stock could reach $74 by December 2028.

- Potential Gains: This target implies a total return of 19% from the current price of $62.

- Annual Return: Investors could see roughly 6% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Fiserv (FISV) delivered stable Q4 results with adjusted earnings per share of $8.64, exceeding guidance, while free cash flow of $4.44 billion topped expectations at 93% conversion.

CEO Mike Lyons emphasized the company’s multi-quarter transformation focused on client service, operational excellence, and innovation.

The team added senior leadership across technology, Clover, and merchant solutions while employee retention reached multi-year highs in 2025.

- Clover drives merchant momentum while banking faces headwinds. Small-business volume grew 7% in Q4, with Clover revenue climbing 12% despite fee eliminations, which created a 6-point drag.

- The platform processed over $200 billion through Commerce Hub in 2025, up more than 200% year-over-year.

- International expansion shows promise, particularly in Brazil, where results track ahead of plan through partnerships with Caixa.

- New strategic relationships with TD in Canada and SMCC in Japan position Clover for growth in large, underpenetrated markets.

- The Financial Solutions segment faces near-term challenges. Banking revenue declined 4% organically in Q4 as the company works through impacts from prior core conversion approaches.

- Management expects these headwinds to persist through the first half of 2026, then stabilize.

- Strategic investments target long-term growth. Fiserv made targeted investments in Q4 to enhance client experience, including increased client-facing resources and technology modernization.

- The company is completing multisite resiliency upgrades across payment platforms by mid-2026.

- CashFlow Central, the integrated AR/AP platform, went live with five financial institutions serving over 100,000 small businesses.

- With 155 banks signed since launch and a pipeline of 400 prospects, management sees significant long-term potential.

New capabilities in stablecoin through the StoneCastle acquisition enable unique recycling of reserves back to financial institutions.

Fiserv also launched FIUSD, providing banks with their own stablecoin solution.

See analysts’ full growth forecasts and estimates for FISV stock (It’s free) >>>

What the Model Says for Fiserv Stock

We analyzed Fiserv as it transformed into a unified commerce and finance platform with strong positions in merchant acquiring and financial technology.

- The company benefits from structural growth in digital payments. Small business volume expanded 7% in Q4 2025 while Clover’s value-added services reached 27% of revenue, up 5 points year-over-year.

- This reflects successful attachment of software, capital, and other services beyond basic payment processing.

- Management expects Clover GPV growth of 10% to 15% in 2026, with the lower end representing core growth and the upper end assuming successful conversion of non-Clover merchants.

- Based on mid-single-digit Merchant Solutions growth and stabilization in Financial Solutions during the second half of 2026, the company should return to consistent performance.

Using a forecast of 3.3% annual revenue growth and 34.2% operating margins, our model projects the stock will rise to $74 within 2.8 years. This assumes a 7.0x price-to-earnings multiple.

That represents significant compression from Fiserv’s historical P/E averages of 13.1x (one year) and 16.2x (five years). The lower multiple reflects near-term margin pressure as the company invests in client service and technology modernization.

For 2026, management guides to 1-3% organic revenue growth with adjusted operating margins of approximately 34%.

First-half margins will be pressured to 31-32% as investments ramp, with Q1 representing the low point below 30%.

Second-half margins should improve to 35-36% as the company laps prior-year headwinds.

The real value lies in executing the One Fiserv plan to deliver sustainable growth through enhanced client service, Clover expansion, and operational efficiency gains from Project Elevate.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for FISV stock:

1. Revenue Growth: 3.3%

Fiserv’s growth centers on merchant acceptance and financial technology. The company delivered 3.8% organic revenue growth in 2025, within guidance of 3.5% to 4%.

Management expects 2026 organic revenue growth of 1-3%, with Merchant Solutions in the mid-single digits and Financial Solutions flat to slightly down.

This reflects difficult first-half comparisons due to higher non-recurring revenue in 2025.

Clover’s low double-digit revenue growth target, combined with enterprise merchant growth and stabilizing banking revenues, supports the 3.3% assumption through 2029.

2. Operating margins: 34.2%

Fiserv delivered 37.4% adjusted operating margin in 2025, down 200 basis points as expected.

The company guides to approximately 34% margins for 2026 as investments in client service and technology infrastructure continue.

Management expects margins to trough in Q1 2026 below 30%, then improve throughout the year to 35-36% by Q4.

Project Elevate should unlock additional efficiency opportunities through business simplification and AI deployment.

3. Exit P/E Multiple: 7.0x

The market values Fiserv at 7.6x earnings. We assume the P/E will compress slightly to 7.0x over our forecast period, below the 13.1x one-year average and 16.2x five-year average.

This conservative multiple acknowledges execution risk during the transformation period and margin pressure from strategic investments.

As Fiserv demonstrates consistent client service improvements, Clover platform expansion, and operational efficiency gains, the company should command a higher multiple reflecting its position at the intersection of commerce and finance ecosystems.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

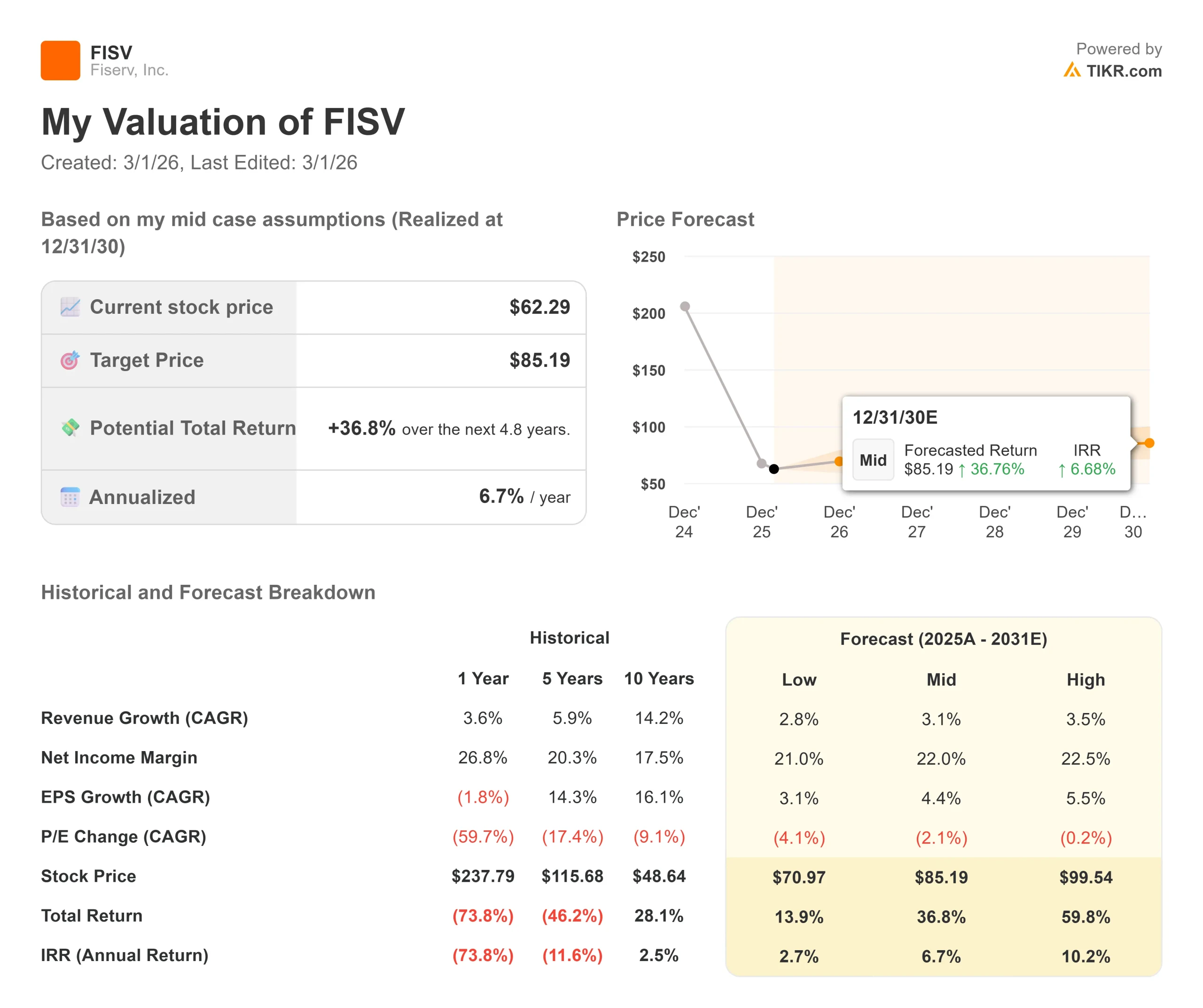

Payment processors face technology transitions and competitive pressures. Here’s how Fiserv stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 2.8% and net income margins compress to 21%, investors still see a 14% total return (2.7% annually)

- Mid Case: With 3.1% growth and 22% margins, we expect a total return of 37% (6.7% annually)

- High Case: If digital payment acceleration drives 3.5% revenue growth while Fiserv maintains 22.5% margins, returns could hit 60% total (10.2% annually)

See what analysts think about FISV stock right now (Free with TIKR) >>>

The range reflects execution on Clover international expansion, success converting non-Clover merchants, banking segment stabilization, and Project Elevate efficiency gains.

In the low case, banking headwinds persist longer than expected or merchant growth disappoints.

In the high case, Clover expansion accelerates, Financial Solutions returns to growth sooner, and margin improvement exceeds expectations as efficiency initiatives deliver results.

How Much Upside Does Fiserv Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!