Key Takeaways:

- Product Reset: New styles will reach 35% of the assortment in spring 2026, up from current levels, as the design team accelerates innovation.

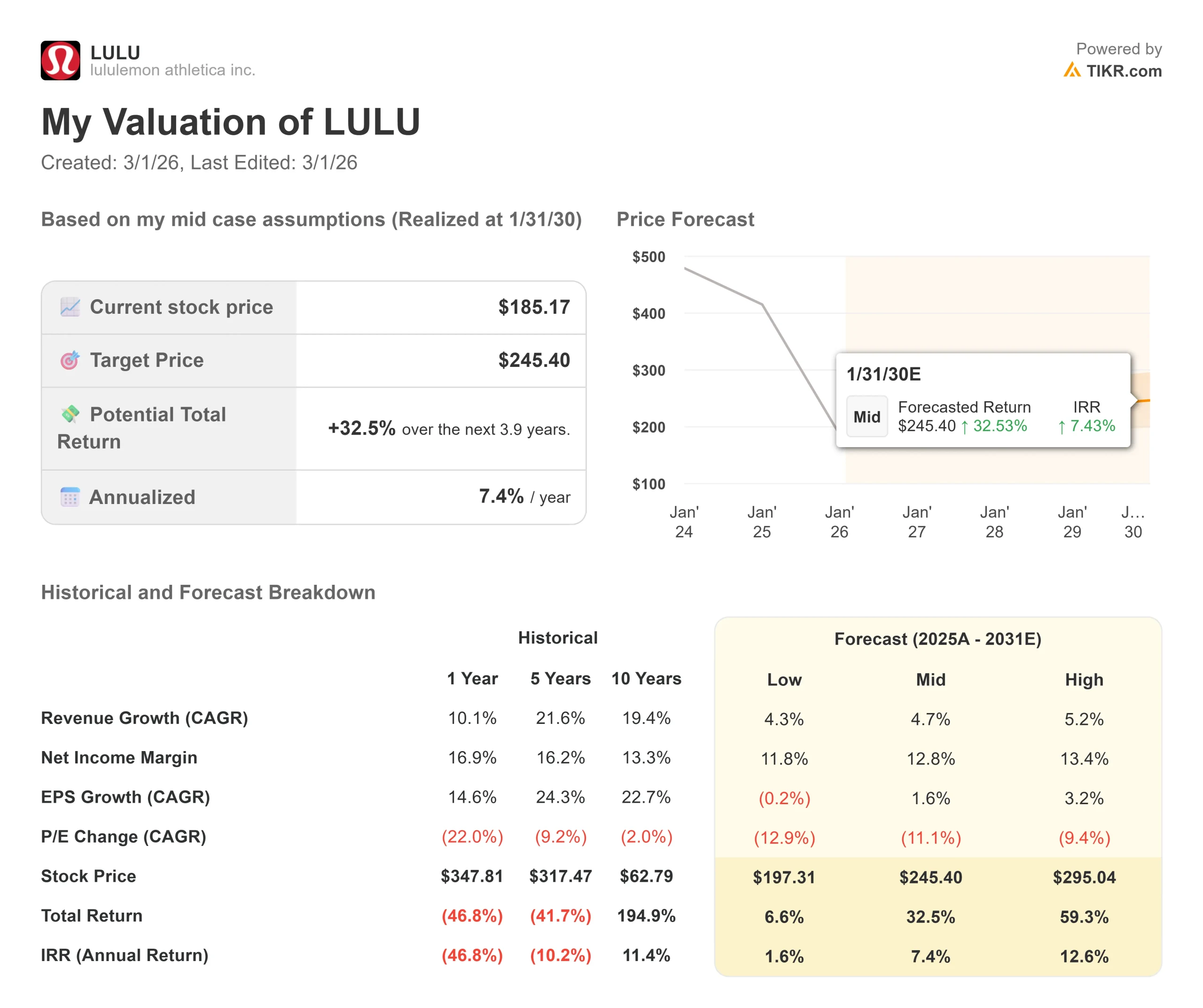

- Price Projection: Based on current execution, LULU stock could reach $212 by January 2028.

- Potential Gains: This target implies a total return of 15% from the current price of $185.

- Annual Return: Investors could see roughly 7% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Lululemon Athletica (LULU) reported mixed third-quarter results for fiscal 2025, with total revenue rising 7% to $2.6 billion while U.S. comparable sales declined 5%.

CEO Calvin McDonald, who will step down January 31 after seven years, highlighted encouraging Thanksgiving weekend performance despite subsequent softening.

- The company now expects full-year revenue of $10.96 billion to $11.05 billion, representing 5% to 6% growth excluding the 53rd week.

- The company expects U.S. revenue trends in Q4 to modestly improve relative to Q3.

- International momentum remains strong, with China Mainland revenue surging 47% in constant currency.

- Management now expects China’s growth at or above the high end of their 20% to 25% target for the year.

The core challenge lies in the U.S. market, where high-value guest frequency and spend remain below expectations.

CFO Meghan Frank outlined a three-pillar action plan focused on product creation, product activation, and enterprise efficiency to drive inflection in 2026.

See analysts’ full growth forecasts and estimates for LULU stock (It’s free) >>>

What the Model Says for Lululemon Stock

We analyzed Lululemon through its transformation effort to reenergize the product engine while maintaining international momentum and managing margin pressure from tariffs.

- The company faces near-term headwinds from increased tariffs and the removal of the de minimis provision, which, combined, will pressure Q4 operating margin by 410 basis points.

- For the full year, management expects gross margin to decrease by approximately 270 basis points, with tariffs accounting for 190 basis points of that decline.

- However, the product pipeline shows promise. The design team is increasing new style penetration to 35% for spring 2026, focusing on performance categories like train while refreshing key franchises, including Swiftly, Daydrift, and Steady State.

- Speed to market is improving, with the goal of reducing mainline product development from 18-24 months to 12-14 months.

International markets provide additional upside. China Mainland delivered exceptional Q3 results with minimal discounting and strong full-price selling.

The Rest of World segment grew 19%, with successful store openings in Seoul and Istanbul signaling a runway for geographic expansion.

Using a forecast of 4.8% annual revenue growth and 18.4% operating margins, our model projects the stock will rise to $212 within 1.9 years. This assumes a 14x price-to-earnings multiple.

That represents compression from Lululemon’s historical P/E averages of 16.3x (one year) and 30.7x (five years).

The lower multiple reflects near-term uncertainty around U.S. market recovery and tariff headwinds, though it may prove conservative if the product reset gains traction faster than expected.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for LULU stock:

1. Revenue Growth: 4.8%

Lululemon’s growth hinges on U.S. market stabilization and sustained international momentum.

- The company delivered 7% revenue growth for Q3, though U.S. weakness weighed on results.

- Management expects the U.S. to finish 2025 down 1% to 2%, while the China Mainland achieves at least 20% growth.

- The product reset beginning in spring 2026 should help drive acceleration, as new styles have historically generated outsized growth among high-value guests.

- Recent innovations like Milemaker and Shake It Out show strong guest response.

As the mix shifts toward 35% new styles, combined with improved visual merchandising and digital experience enhancements, the company has multiple levers to drive traffic and conversion.

2. Operating margins: 18.4%

Lululemon showed a gross margin to 55.6% of net revenue in Q4, compared to 58.5% in Q3 2024; here, near-term pressure is unavoidable.

The company expects Q4 operating margin deleverage of approximately 680 basis points, driven heavily by tariffs.

For 2026, management indicated negative factors will outweigh positives, with a full year of tariffs partially offset by strategic pricing, vendor negotiations, and efficiency initiatives.

The team is taking a conservative inventory posture, managing units below sales plans to minimize markdown risk and leverage chase capabilities.

3. Exit P/E Multiple: 14x

The market currently values Lululemon at 15.2x earnings. We assume modest compression to 14x over our forecast period, reflecting execution risk around the U.S. turnaround and margin pressure.

Leadership transition adds near-term uncertainty, with CFO Meghan Frank and Chief Commercial Officer Andre Maestrini serving as co-CEOs until a permanent replacement is named.

However, the product pipeline is largely set through the first half of 2026, providing continuity during the search.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

The athletic apparel market remains competitive, and consumer behavior is uncertain. Here’s how Lululemon stock might perform under different scenarios through January 2030:

- Low Case: If revenue growth slows to 4.3% and net income margins compress to 11.8%, investors still see a 7% total return (2% annually).

- Mid Case: With 4.7% growth and 12.8% margins, we expect a total return of 33% (7% annually).

- High Case: If the product reset accelerates U.S. recovery, driving 5.2% revenue growth while margins stabilize at 13.4%, returns could reach 59% total (13% annually).

See what analysts think about LULU stock right now (Free with TIKR) >>>

The range reflects execution on product innovation, successful navigation of tariff headwinds, and the company’s ability to reengage high-value guests while maintaining international momentum.

In the low case, U.S. trends fail to improve, tariff mitigation falls short, and competition intensifies.

In the high case, new product resonates strongly, China growth continues outperforming, and operational efficiency initiatives exceed expectations.

How Much Upside Does Lululemon Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!