Key Stats for ASML Stock

- Past-Week Performance: -1.3%

- 52-Week Range: €508.4 to €1,312.8

- Current Price: €1,233.4

What Happened?

ASML‘s CTO Marco Pieters confirmed on February 26 that High NA EUV machines have processed 500,000 wafers and achieved 80% uptime, technically validating the $400 million tools for high-volume chip production at a critical industry inflection point.

The confirmation arrived alongside ASML’s strongest quarterly order intake on record, with Q4 net bookings hitting €13.2 billion, split between €7.4 billion in EUV and €5.8 billion in non-EUV systems, all while the stock trades at €1,233.40.

Beneath the order surge, the engine driving ASML’s momentum is a structural increase in lithography intensity across both advanced logic and DRAM, where customers migrating to 3-nanometer nodes and 4 F-square DRAM architectures require significantly more EUV layers per chip.

Investors are actively re-rating ASML from a cyclical equipment supplier to a structural AI infrastructure enabler, as the company’s 2025 annual report formally identified AI demand as the primary growth driver across its entire customer base for the first time.

CEO Christophe Fouquet stated on the Q4 earnings call that “the last few months have confirmed the positive impact of AI on customer demand for our advanced product and especially for our EUV system,” directly linking the AI buildout to accelerating capacity expansion across logic and DRAM customers simultaneously.

Further supporting that conviction, ASML’s board launched a new €12 billion share buyback program on January 28, running through December 31, 2028, signaling that management views the current price as an attractive entry point relative to its €44 billion to €60 billion 2030 revenue target.

Looking out three to five years, ASML’s monopoly on EUV and High NA lithography tools positions it as the single irreplaceable bottleneck in the global AI chip supply chain, making its long-term competitive moat arguably stronger today than at any prior point in its history.

Wall Street’s Take on ASML Stock

ASML’s CTO confirmation on February 26 that High NA EUV tools have processed 500,000 wafers and achieved 80% uptime directly validates the company’s path toward its €44 billion to €60 billion 2030 revenue target.

That trajectory is already showing up in the numbers: revenue grew 15.6% to €32.7 billion in 2025, EPS surged 28.4% to €24.71, and consensus projects further EPS expansion to €29.65 in 2026, a 20% increase.

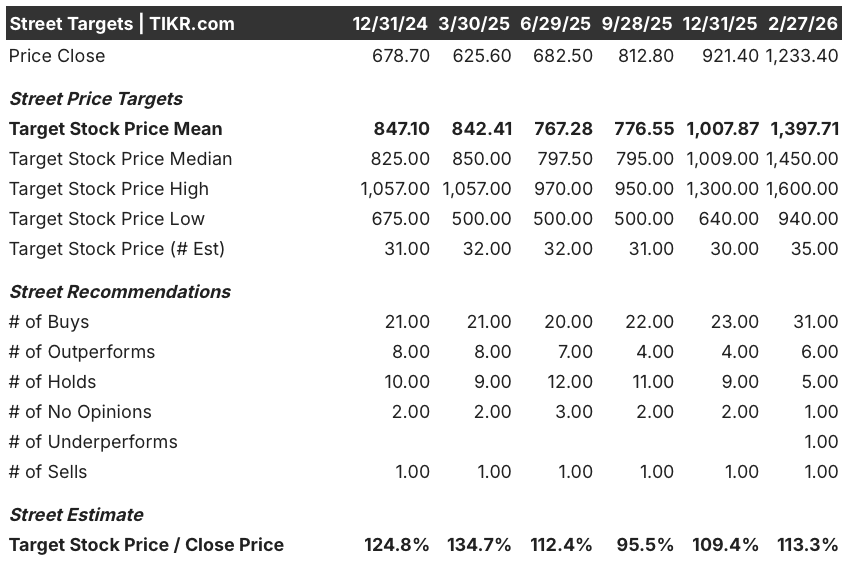

Currently, 31 analysts rate ASML a Buy, 6 rate it Outperform, 5 Hold, 1 Underperform, and 1 Sell, producing a mean price target of €1,397.71, implying 13.3% upside from the February 27 close of €1,233.40.

The analyst target range spans €940 on the low end to €1,600 on the high end, where High NA adoption acceleration and DRAM EUV layer expansion drive the upside case while export control escalation on China’s 20% revenue share anchors the downside.

What Does the Valuation Model Say?

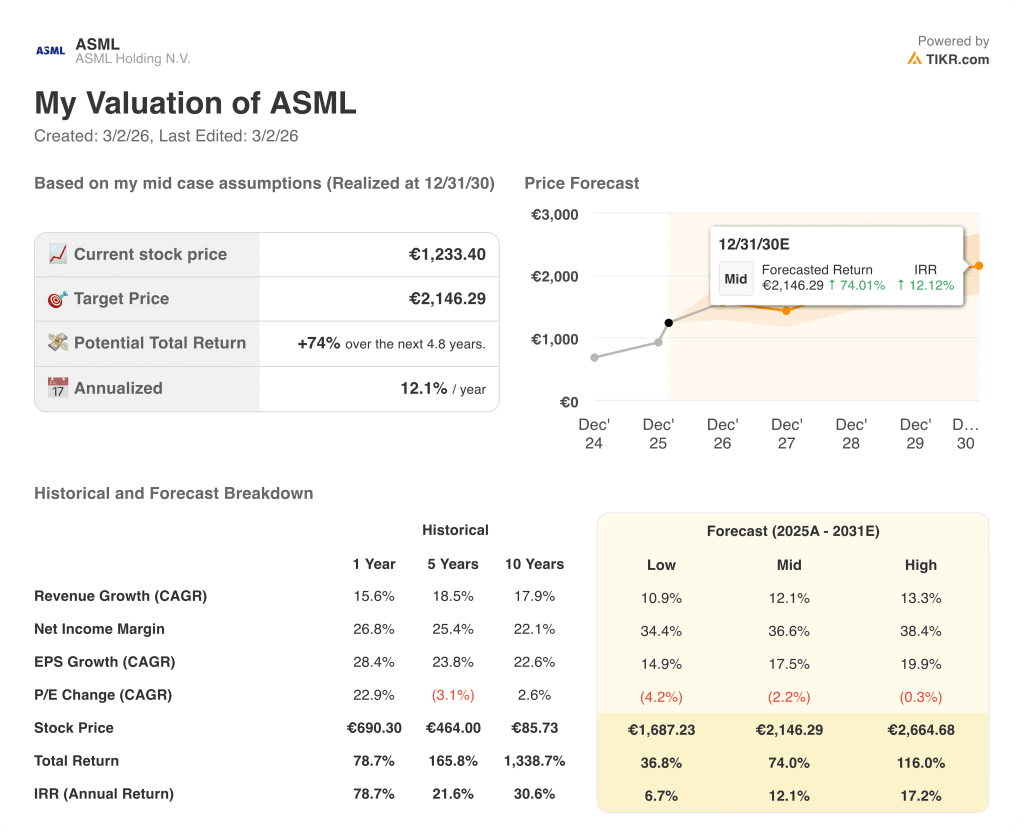

TIKR’s mid-case valuation model targets €2,146.29, implying a 74% total return over 4.8 years at a 12.1% annual IRR. The stock currently trades at a 42.6% discount to that mid-case target.

The market is treating ASML’s wide 2026 revenue guidance range of €34 billion to €39 billion as uncertainty, but the backlog of €38.8 billion already covers the high end of that range entirely.

EBITDA margins expanded to 37.7% in 2025 and consensus projects further expansion to 39% in 2026, making the current valuation a discount to an accelerating margin profile.

ASML’s new €12 billion share buyback program, announced January 28, signals that management views €1,233.40 as significantly below intrinsic value, a conviction statement backed by €11 billion in 2025 free cash flow.

The core risk is that escalating U.S. and Dutch export controls push China’s revenue contribution meaningfully below the guided 20% of sales, directly compressing the €34 billion to €39 billion revenue range and gross margin simultaneously.

The second half 2026 revenue progression will reveal whether customer fab completions and ASML’s quarterly EUV move rate increase align as management projected, making it the single most important data point for bulls this year.

ASML appears to be undervalued at €1,233.4 with a €2,146.29 mid-case target and a monopoly no competitor can replicate, but China export control developments remain the one variable that could reframe the entire earnings picture.

Should You Invest in ASML Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ASML stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ASML Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ASML stock on TIKR for Free →