Key Stats for Mastercard Stock

- Past week’s performance: -2%

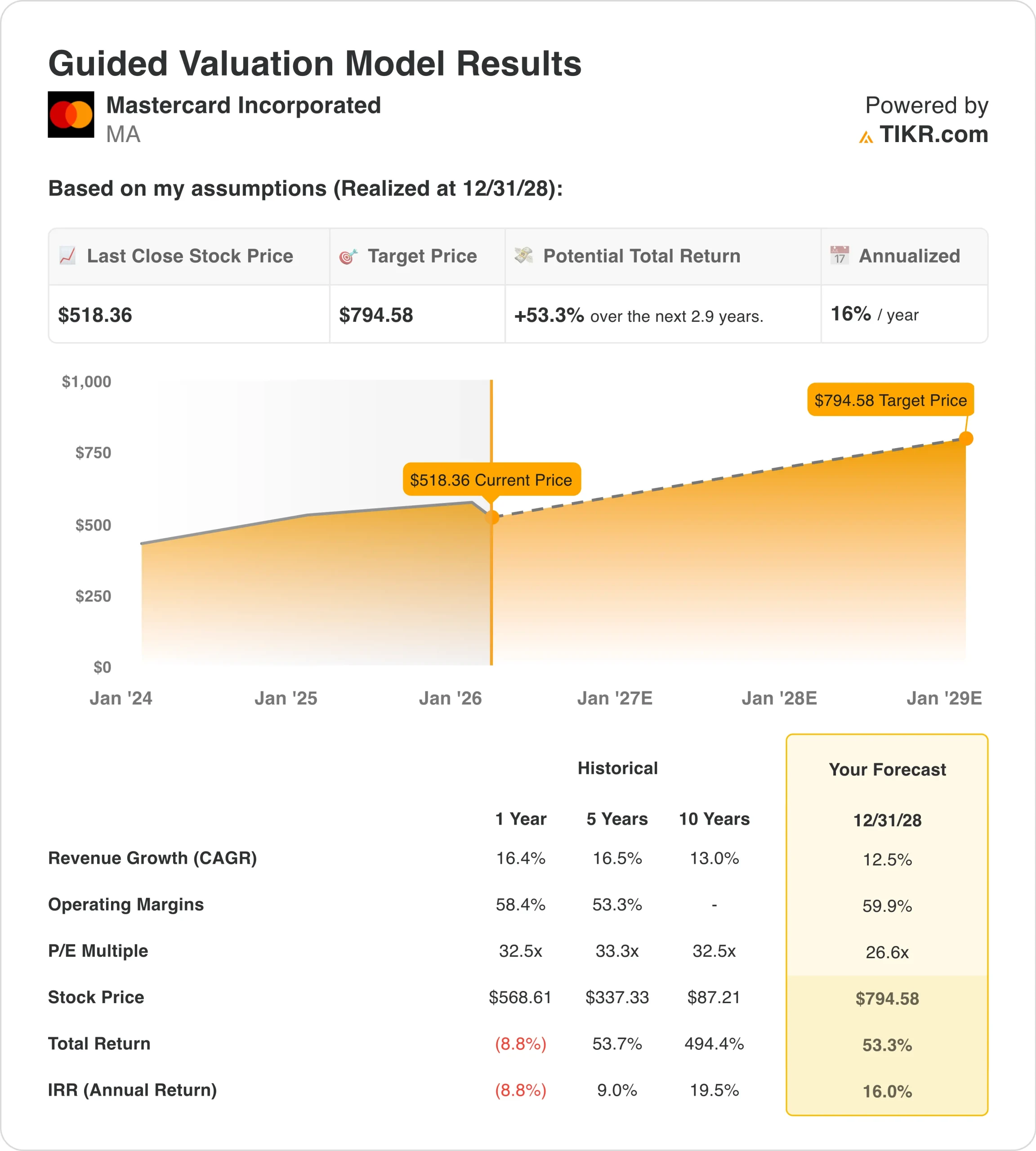

- 52-week range: $466 to $602

- Valuation model target price: $795

- Implied upside: 53% over 2.9 years

Value your favorite stocks like Mastercard with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Shares of Mastercard (MA) slipped about 2% this week, closing near $518, even after the company reported solid Q4 results.

The pullback followed Mastercard’s Q4 earnings release on January 29, where the company reported adjusted EPS of $4.76, beating consensus estimates by 12%. Revenue of $8.8 billion also came in modestly ahead of expectations and rose nearly 18% year over year.

Despite the beat, the stock traded lower because expectations were already elevated after a strong run into earnings. Investors appeared to focus on margin normalization, as EBIT margins declined sequentially from Q3 levels even though they improved year over year.

At the same time, broader payment stocks weakened during the week after renewed discussion in Europe around reducing reliance on U.S.-based card networks. Reports highlighting alternative payment rails and regulatory scrutiny weighed modestly on sentiment across the sector.

Management commentary remained constructive, with executives noting steady growth across both affluent and mass-market consumers and continued strength in cross-border volumes. However, there were no major guidance changes to reset near-term expectations.

Overall, the move reflects valuation sensitivity and profit-taking rather than a change in Mastercard’s underlying business performance.

See analysts’ growth forecasts and price targets for Mastercard (It’s free) >>>

Is Mastercard Stock Undervalued?

Under the valuation model assumptions realized through 2028, the stock is modeled using:

- Revenue growth (CAGR): 12.5%

- Operating margins: 159.9%

- Exit P/E multiple: 26.6x

Based on these inputs, the model estimates a target price of $795, implying 53% total upside from the current share price and a 16% annualized return over the next 2.9 years.

Execution remains the key driver behind these assumptions, especially volume growth and pricing resilience across global payment flows.

Revenue trends continue to benefit from steady consumer spending, e-commerce growth, and cross-border recovery, driving Mastercard’s 16% revenue growth over the past year.

Margins remain elevated near 59% because of operating leverage and disciplined expense growth, even as the company continues to invest in security, data, and value-added services.

Cash generation also remains strong, with free cash flow of nearly $4.9 billion in Q4, supporting continued share repurchases and dividend growth.

While regulatory headlines and valuation concerns can drive short-term volatility, Mastercard’s fundamentals continue to reflect consistent growth, high profitability, and strong capital returns.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>