Key Takeaways for FICO Stock as of July 2026

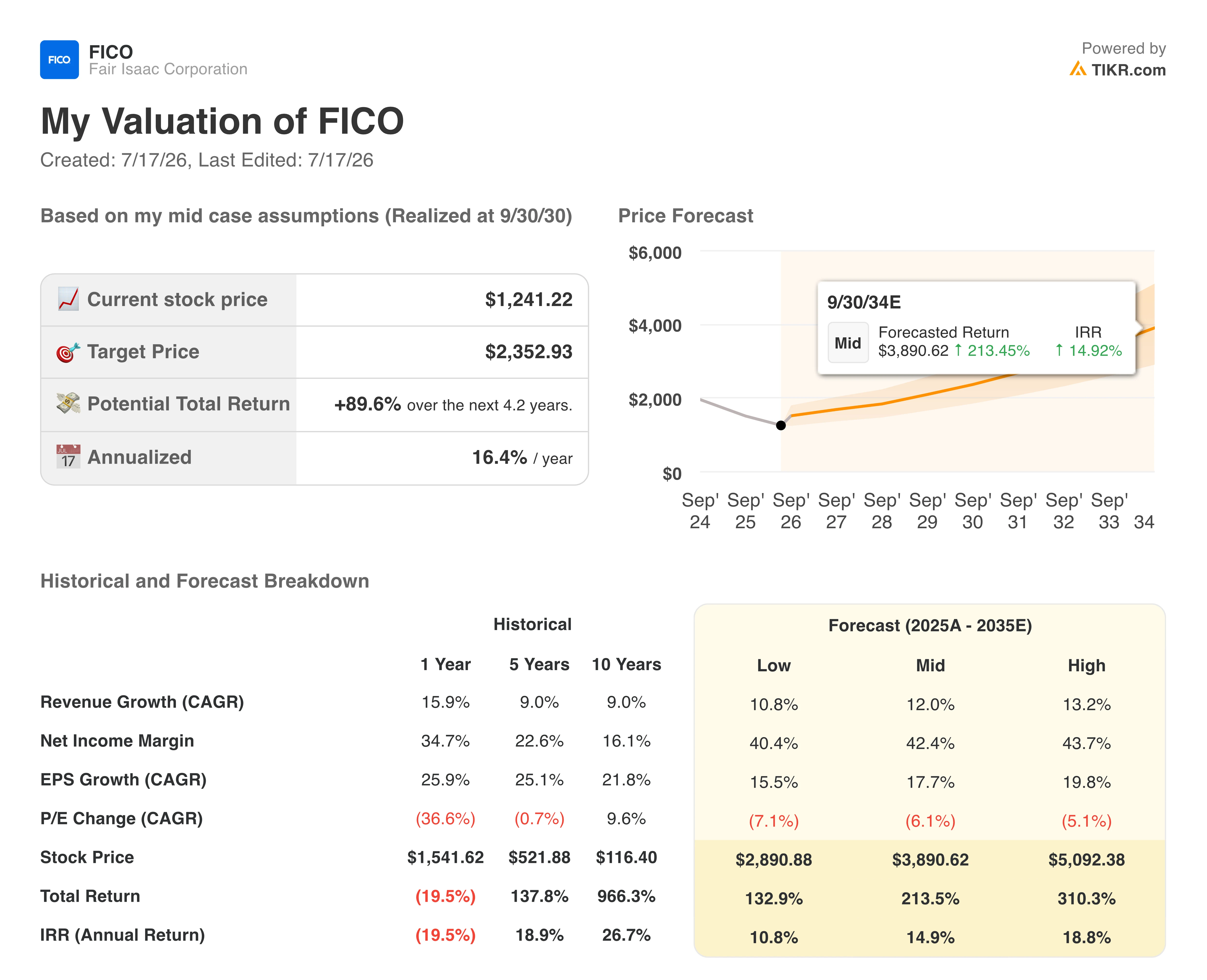

- TIKR’s valuation model puts Fair Isaac’s fair value at $2,353, a 90% total return from today’s $1,241, worth 16% annualized through September 2030.

- Eleven of twenty analysts rate FICO stock a buy; only one recommends selling.

- Facing FHFA-driven competition from VantageScore, FICO cut its 10T mortgage score price from $4.95 to $0.99 in April, and Q2 revenue still grew 39% to $692 million.

- Down 34% from its high even after clawing back from an April 10 drawdown that hit 50.93%, FICO stock still prices in far more competitive fear than Q2’s 39% revenue growth justifies.

FICO stock trades near a 90% gap to TIKR’s fair value target. See the full model on TIKR for free

FICO Slashes 10T Mortgage Score Pricing to $0.99 as Revenue Jumps 39%

Fair Isaac Corporation (FICO) cut the upfront price of its FICO 10T mortgage score from $4.95 to $0.99 in April 2026, matching VantageScore’s headline price point just as Q2 revenue climbed 39% to $692 million. The move landed in the same quarter the Federal Housing Finance Agency pushed to open the conforming mortgage market to VantageScore as a second credit-scoring option, a shift that had cut 32% off FICO stock’s value over the prior year.

CEO Will Lansing addressed the competitive threat directly on Q2 earnings call when pressed by an analyst on VantageScore’s actual footprint: “Ballpark, I would call it 2%.” He added that in the nonconforming mortgage market, where lenders choose freely between scores, “I don’t think they have any share at all.” Those numbers cut against the market narrative that priced FICO stock down from a $1,828 close in June 2025.

The pricing cut itself is not a retreat. Lansing structured it as a $0.99 upfront fee paired with a $65 success fee collected only once a loan closes, a model FICO estimates could capture half the mortgage scoring market once its Direct License Program launches with the credit bureau resellers. Scores segment revenue still grew 60% to $475 million in the quarter, with mortgage origination revenue up 127% and accounting for 63% of total scores revenue. Management raised full-year guidance to $2.45 billion in revenue, a 23% increase, right after making the price cut that was supposed to signal weakness.

That combination, an aggressive defensive price move paired with accelerating growth and raised guidance, is the development repricing FICO stock. The market read the $0.99 price as capitulation to VantageScore. The Q2 numbers say it was leverage.

FICO Stock’s 51% Drawdown Meets a Falling Street Target

FICO stock fell 51% from its peak, bottoming out on April 10, 2026, right as the FHFA’s push for VantageScore competition hit its loudest point. Shares have since clawed back to a 34% drawdown, still deep even with Q2 revenue up 39% and guidance raised twice this fiscal year.

That gap between the drawdown and the growth numbers is what the 10T pricing move was built to close.

Eleven analysts rate FICO stock a buy, five call it outperform, four rate it hold, and one recommends selling, with 20 analysts covering the name as of July 16, 2026. The mean price target sits at $1,535, a 24% premium to the $1,241 close, though that target has fallen from $2,197 a year earlier as the regulatory overhang weighed on estimates.

Even after that cut, the Street’s target-to-close ratio has held above 120% every quarter since June 2025, including the current 124% reading.

TIKR Values FICO Stock at $2,353, Pricing In Continued Scores Growth

TIKR’s mid-case model values FICO stock at $2,353 by September 2030, implying a 90% total return from the current price of $1,241, or 16% annualized over 4.2 years.

That annualized return sits well above what a mature, low-volatility financial data name typically prices in, reflecting the model’s mid-case revenue growth assumption of 12% and a net income margin expanding to 42%.

The target is reachable because the 10T pricing cut protects scores revenue growth rather than trading it away, and Q2’s 60% scores segment growth and 39% total revenue growth show that protection already working. Management’s own guidance raise to $2.45 billion in FY26 revenue backs the model’s growth assumptions rather than undercutting them.

Should You Invest in Fair Isaac Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Fair Isaac Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fair Isaac Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FICO stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!