Key Takeaways:

- AI-Driven Demand: AEP has secured 28 gigawatts of contracted load additions, 80% of which are from data centers, including Google, AWS, and Meta.

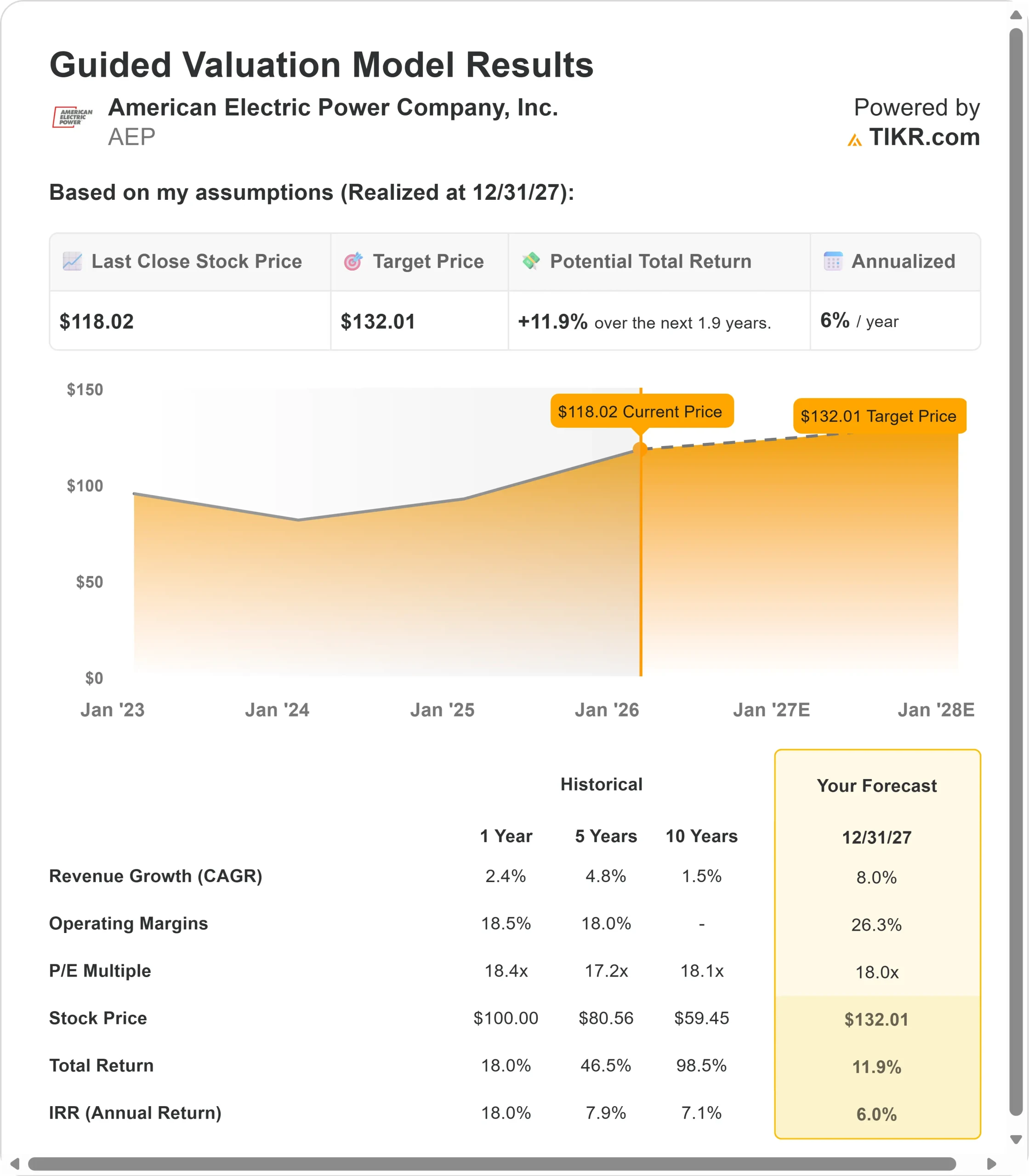

- Price Projection: Based on current execution, the stock could reach $132 by December 2027.

- Potential Gains: This target implies a total return of 12% from the current price of $118.

- Annual Return: Investors could see roughly 6% annual growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

American Electric Power (AEP) just announced one of the most aggressive growth plans in the utility sector.

The company unveiled a massive $72 billion capital spending program through 2030, driven by unprecedented electricity demand from data centers and industrial customers.

CEO Bill Fehrman is executing a strategy centered on AEP’s competitive advantage: the largest 765 kilovolt transmission system in America.

These ultra-high voltage lines carry more power than standard transmission infrastructure, making AEP uniquely attractive to hyperscalers building energy-intensive AI facilities.

- AEP expects system-wide demand to reach 65 gigawatts by 2030, up 76% from current levels.

- The company has already locked in 28 gigawatts through binding contracts with customers like Google, Amazon Web Services, and Meta.

- These aren’t speculative projections—they’re backed by take-or-pay agreements that protect both the utility and its existing customers.

Despite this transformation into a high-growth infrastructure play, AEP stock trades at $118, offering upside for investors who recognize the company’s position at the center of America’s AI buildout.

See analysts’ full growth forecasts and estimates for AEP stock (It’s free) >>>

What the Model Says for American Electric Power Stock

We analyzed AEP through the lens of its evolution from a traditional utility into a critical enabler of the digital economy.

- The company operates over 2,100 miles of 765kV transmission lines across six states—representing 90% of all such infrastructure in the United States.

- This network attracts data center customers who need massive amounts of reliable, efficiently delivered power.

- AEP’s contracted load growth breaks down roughly into 80% data centers and 20% industrial customers, such as steel mills and LNG facilities.

- About half the demand sits in Texas’s ERCOT market, with 40% in PJM and 10% in the Southwest Power Pool.

- The company has secured regulatory approval for specialized data center tariffs in Ohio, Indiana, Kentucky, and West Virginia, with similar filings pending in Michigan, Texas, and Virginia.

Using a forecast of 8% annual revenue growth and 26.3% operating margins, our model projects the stock will rise to $132 within 1.9 years. This assumes an 18x price-to-earnings multiple at exit.

That represents compression from AEP’s current NTM P/E of 19.1x.

The company’s multiple has averaged 18.4x over the past year and 18.1x over the last decade. The modest contraction reflects near-term execution risk as AEP deploys unprecedented capital while working through regulatory processes across 11 states.

However, the disciplined capital allocation and reduced regulatory lag should support gradual multiple expansion as the plan proves out.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for AEP stock:

1. Revenue Growth: 8%

AEP’s growth story centers on connecting new load to its transmission backbone. The company reported commercial and industrial load growth of nearly 8% on a rolling 12-month basis through September 2025. This momentum should continue as contracted customers energize their facilities.

Management distilled 190 gigawatts of customer interest down to 28 gigawatts of executed contracts—a conservative approach that filters out speculative demand.

CFO Trevor Mihalik emphasized the company will “underpromise and overdeliver,” reporting only load backed by letters of agreement or energy service agreements with financial commitments.

The $72 billion capital plan supports this load growth with two-thirds directed toward transmission and generation. AEP recently won 765kV project awards in both ERCOT and PJM, positioning the company for continued growth beyond the current planning horizon.

2. Operating margins: 26.3%

AEP expects margins to expand as investments come online. The capital plan drives a 10% compound annual growth rate in the rate base through 2030, with nearly 90% recovered through formula rates and other reduced-lag mechanisms.

Recent legislative wins support margin improvement. Ohio’s HB 15 establishes forward-looking test years with true-up provisions.

Texas HB 5247 creates a unified tracker for capital investment recovery. Oklahoma SB 998 authorizes cost deferrals between rate cases. These changes reduce regulatory lag and improve earned returns on equity toward the 9.5% target by 2030.

3. Exit P/E Multiple: 18x

The market currently values AEP at 19.1x next twelve months’ earnings. We assume the multiple compresses to 18x through our forecast period, slightly below the company’s historical average.

This conservative assumption accounts for execution risk inherent in deploying $72 billion of capital across diverse jurisdictions.

AEP must navigate rate cases, integrated resource plans, and generation procurement while maintaining customer affordability.

Management projects residential rates will rise roughly 3.5% annually over 5 year period—below the 4% five-year inflation average—but regulatory outcomes remain subject to commission decisions.

As the company demonstrates consistent execution and earnings growth accelerates in 2028-2030, the multiple should expand toward historical norms. AEP expects operating earnings to grow 7-9% annually from 2026-2030, with a 9% compound annual growth rate over the full five-year period.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

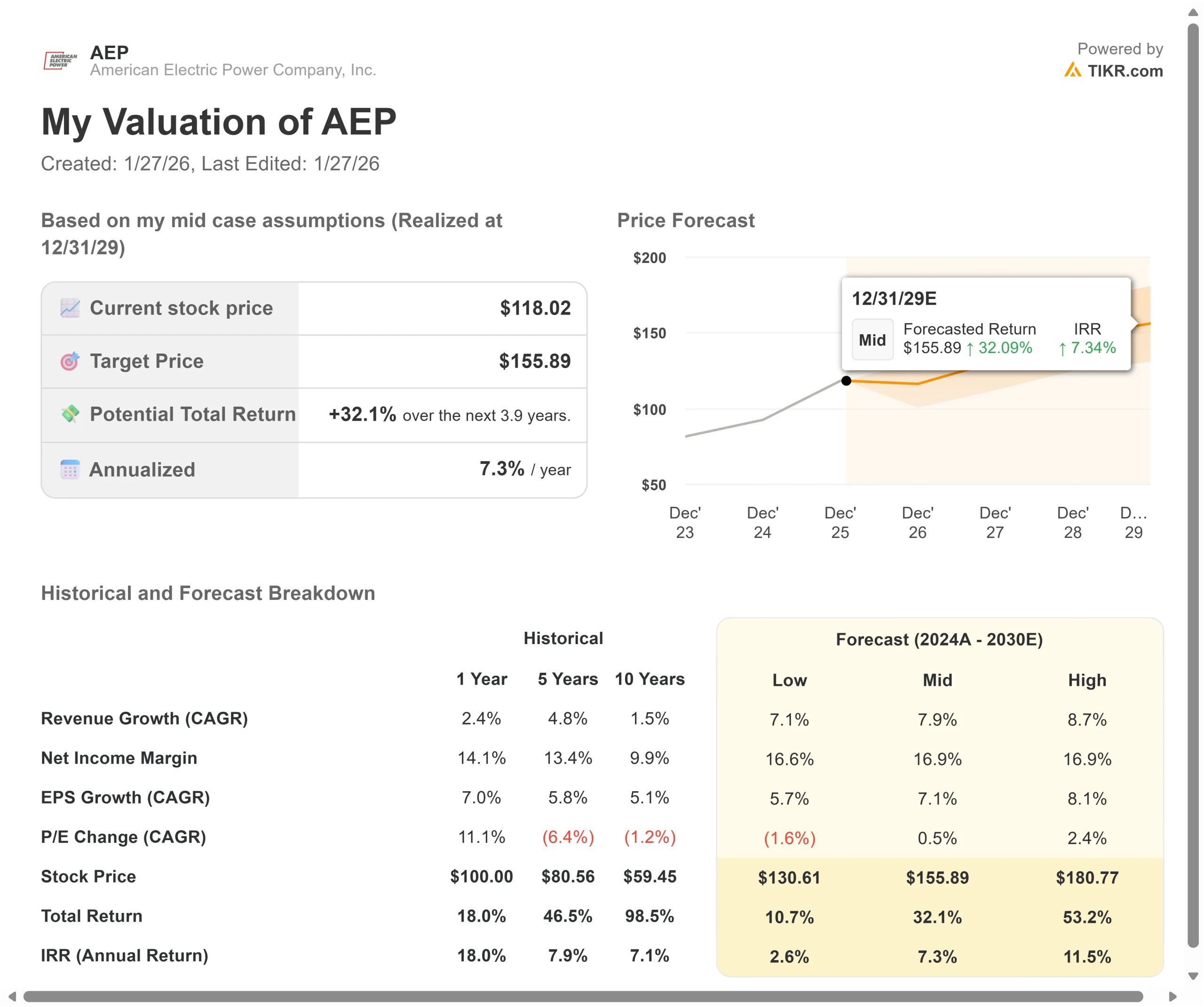

Electric utilities face regulatory uncertainty and capital deployment challenges. Here’s how AEP stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth moderates to 7.1% and margins compress to 16.6%, the stock still offers a 2.6% annual return.

- Mid Case: With 7.9% growth and 16.9% margins, we expect an annual return of 7.3%.

- High Case: If contracted load energizes faster and AEP maintains 16.9% margins while growing at 8.7%, returns could hit 11.5% annually.

See what analysts think about AEP stock right now (Free with TIKR) >>>

The range reflects execution on the capital plan, regulatory outcomes across 11 states, and the pace at which data center customers bring facilities online.

In the low case, permitting delays or adverse rate decisions slows progress.

In the high case, AEP converts additional portions of the 190 gigawatt opportunity pipeline into firm contracts ahead of schedule.

How Much Upside Does American Electric Power Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!