Key Takeaways:

- Strategic Reset: New CEO Enrique Lores takes over on March 1st to accelerate execution after branded checkout struggles.

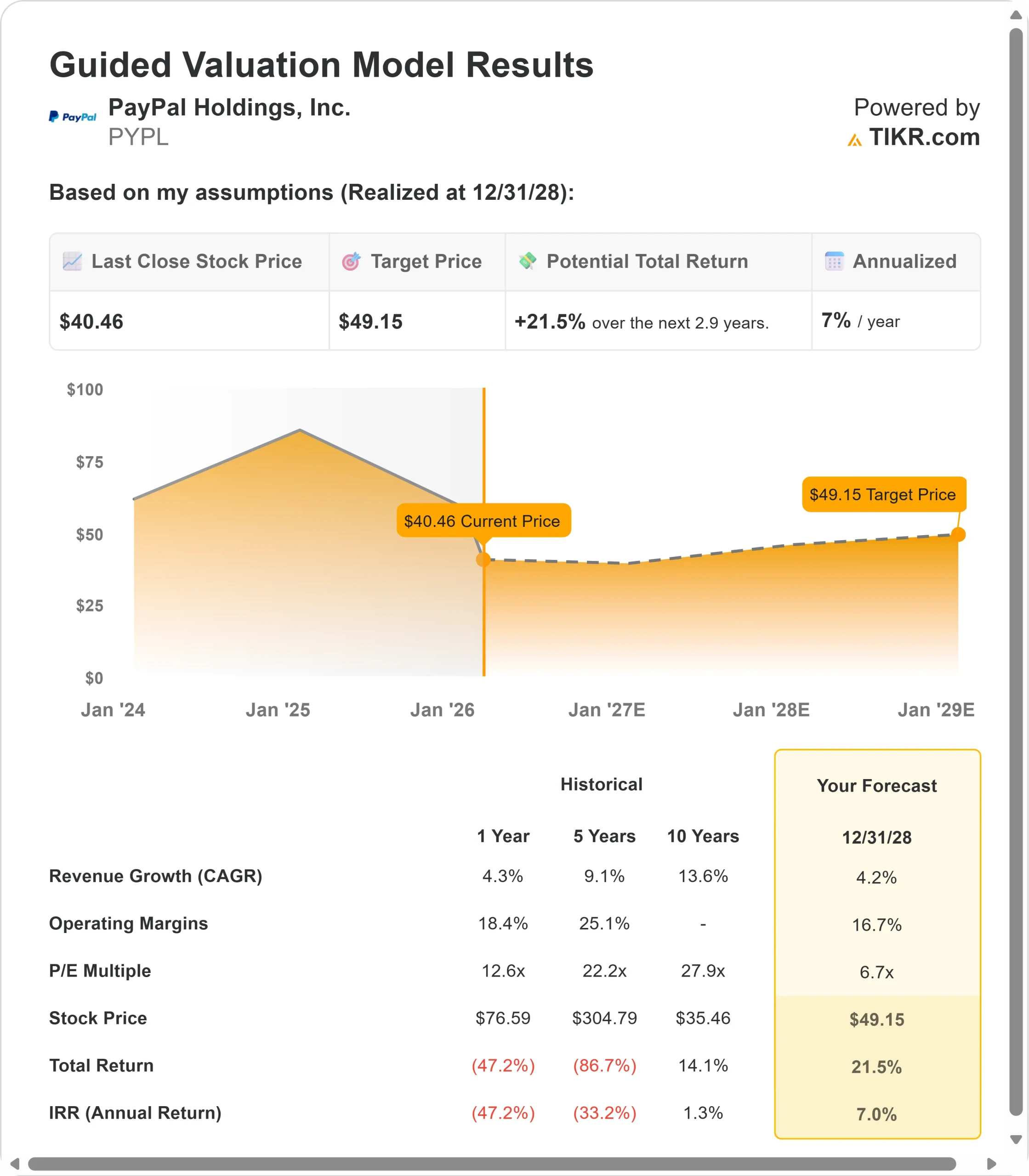

- Price Projection: Based on current assumptions, PYPL stock could reach $49 by December 2028.

- Potential Gains: This target implies a total return of 21.5% from the current price of $40.46.

- Annual Return: Investors could see roughly 7% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

PayPal Holdings (PYPL) faced significant headwinds in Q4, with online branded checkout TPV growing just 1% on a currency-neutral basis—down sharply from 5% in Q3.

The company announced a leadership change, appointing Enrique Lores as CEO effective March 1st to bring greater execution discipline during this critical transformation period.

- The slowdown stemmed from three main areas: U.S. retail weakness among lower- and middle-income consumers, international headwinds, particularly in Germany, and a deceleration in high-growth verticals such as travel, ticketing, and gaming.

- Despite branded checkout challenges, several businesses performed well. Venmo revenue grew approximately 20% to $1.7 billion in 2025, with total active accounts surpassing 100 million.

- Enterprise Payments delivered seven consecutive quarters of profitable growth, returning to double-digit volume growth in Q4.

- Buy Now, Pay Later delivered over $40 billion in TPV, growing more than 20% year-over-year.

- PayPal’s turnaround strategy centers on three priorities: experience, presentment, and selection.

- On experience, the company needs competitive placement with biometric authentication and passkey adoption—currently only 36% of consumers are “checkout-ready” with biometric authentication. Management targets bringing nearly half of consumers to this status by end of 2026.

- For presentment, PayPal sees dramatic results when positioned competitively. When the company secures placement above competitors with upstream BNPL messaging and a second payment button, selection rates more than double. Currently, BNPL messaging accounts for less than 15% of traffic—a significant opportunity for improvement.

- Upon launch, PayPal is introducing PayPal Plus, a rewards program that lets consumers earn and redeem rewards at checkout.

- Early U.K. results showed mid-single-digit growth in branded checkout TPV for enrolled users versus non-enrolled users in December, achieved almost entirely organically, with no marketing.

The company is making calculated investments in 2026, representing approximately 3 points of headwind to transaction margin dollar growth. About two-thirds of the target is branded checkout and BNPL, with the remainder supporting Venmo loyalty and agentic commerce initiatives.

PayPal expects these investments to deliver improved results as redesigned experiences scale and biometric adoption increases.

See analysts’ full growth forecasts and estimates for PYPL stock (It’s free) >>>

What the Model Says for PayPal Stock

We analyzed PayPal’s transformation from a pure-play digital wallet into a diversified commerce platform.

The company benefits from multiple growth drivers beyond branded checkout, including Venmo’s evolution into a monetized commerce platform, Enterprise Payments’ return to profitability, and emerging opportunities in agentic commerce.

Using a forecast of 4.2% annual revenue growth and 16.7% operating margins, our model projects the stock will rise to $49 within 2.9 years. This assumes a 6.7x price-to-earnings multiple.

That represents significant compression from PayPal’s historical P/E averages of 12.6x (one year), 22.2x (five years), and 27.9x (ten years).

The lower multiple acknowledges near-term execution challenges in branded checkout, competitive intensity, and the time required for strategic investments to generate returns.

The real value lies in successfully executing the three-pillar strategy while scaling high-growth businesses like Venmo and expanding Enterprise Payments market share.

Management is not committing to its 2027 Investor Day targets at this time, citing more challenging market conditions and slower-than-anticipated merchant adoption.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PYPL stock:

1. Revenue Growth: 4.2%

PayPal’s growth centers on stabilizing branded checkout while scaling diversified revenue streams.

The company expects slightly positive to low-single-digit branded checkout growth for 2026 as product deployments scale and biometric adoption increases.

Venmo is on track to exceed $2 billion in revenue ahead of plan, while Enterprise Payments returned to double-digit volume growth in Q4.

Management sees improving results building over time as strategic merchant integrations are completed, presentment improves, and rewards programs drive the consumer flywheel.

2. Operating margins: 16.7%

We assume modest compression to 16.7% as the company invests heavily in branded checkout improvements, merchant co-marketing agreements, and consumer rewards programs.

These investments represent approximately 3 points of headwind to transaction margin dollars in 2026 but position the business for stronger long-term performance.

3. Exit P/E Multiple: 6.7x

The market currently values PayPal at 7.6x earnings.

We assume the P/E will compress to 6.7x over our forecast period. Near-term uncertainty from branded checkout execution weighs on the multiple.

The company faces intense competition from alternative payment methods, particularly in international markets like Germany.

As PayPal demonstrates execution improvements across its three strategic priorities and proves the effectiveness of its investment programs, the company should command a higher multiple relative to historical averages.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

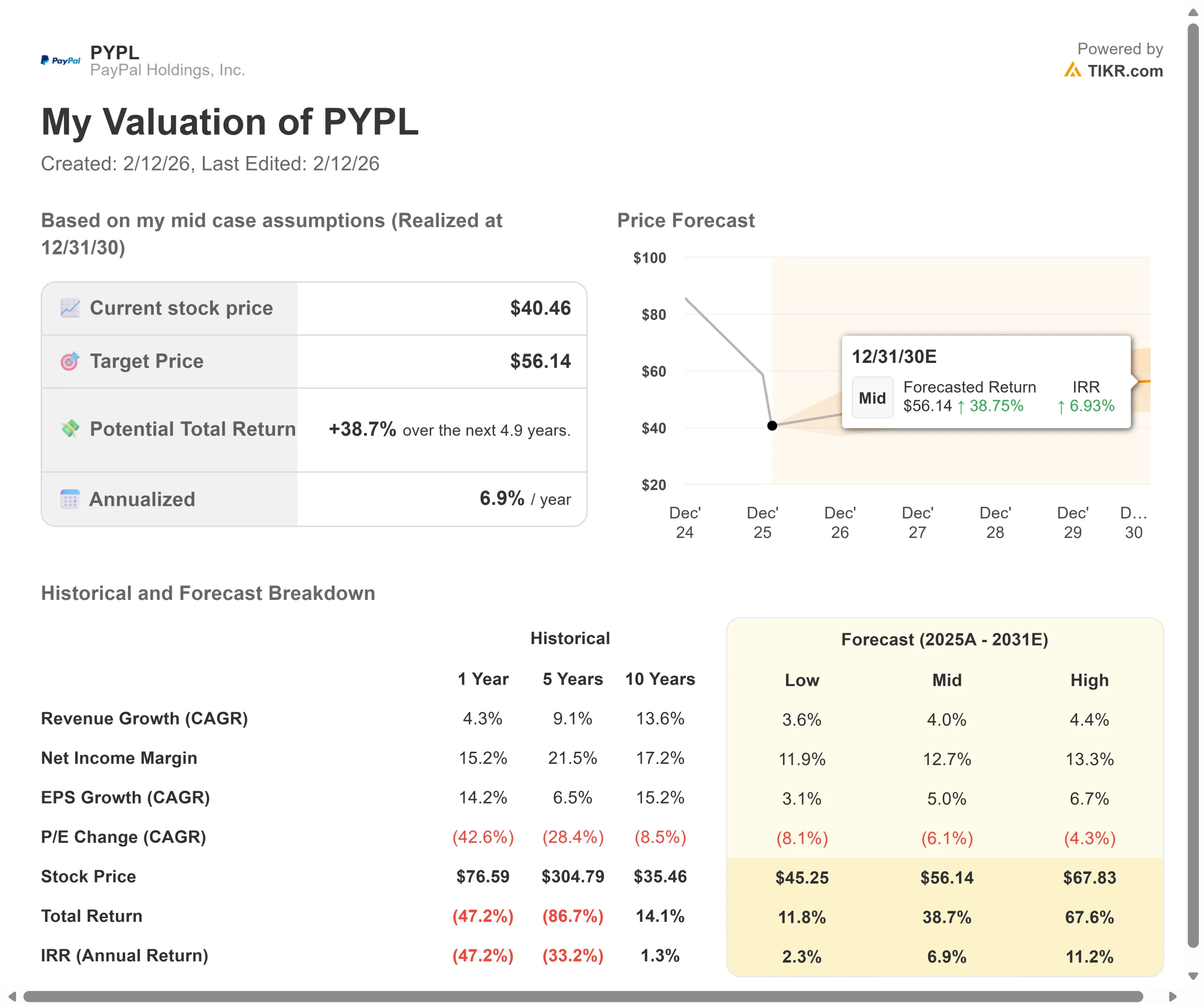

Digital payments face rapid innovation cycles and shifting consumer preferences. Here’s how PayPal stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 3.6% and net income margins compress to 11.9%, investors still see an 11.8% total return (2.3% annually)

- Mid Case: With 4.0% growth and 12.7% margins, we expect a total return of 38.7% (6.9% annually)

- High Case: If branded checkout execution exceeds expectations, driving 4.4% revenue growth while PayPal maintains 13.3% margins, returns could hit 67.6% total (11.2% annually)

See what analysts think about PYPL stock right now (Free with TIKR) >>>

The range reflects execution of the three-pillar strategy, successful merchant adoption of redesigned experiences, and PayPal Plus’s ability to drive consumer habit formation.

In the bear case, branded checkout continues to decline, and investments fail to deliver expected returns.

In the best case, biometric adoption accelerates faster than anticipated, upstream presentment drives significant share gains, and Venmo exceeds revenue expectations.

How Much Upside Does PayPal Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!