Key Takeaways:

- FDA Catalyst: Edwards Lifesciences secured FDA approval for the SAPIEN M3 mitral valve replacement system on 12/23/25, expanding transseptal replacement into a new U.S. indication and reinforcing management’s 2030 TMTT revenue target of $2 billion.

- Guidance Reset: Edwards Lifesciences posted Q4 sales of $2 billion on 2/10/26 and guided 2026 adjusted EPS at $3 to frame demand strength in structural heart, with TAVR at $1 billion and TMTT at $156 million in the quarter.

- Price Projection: Based on 10% revenue CAGR and 30% operating margins through 12/31/28, Edwards Lifesciences stock could reach $106 by 12/31/28 on a 26x P/E multiple as earnings scale with mix shifting toward higher-growth TMTT.

- Upside Math: Edwards Lifesciences’ $106 target implies 38% total upside from the current $77 price, representing an annualized return of 12% over about 3 years as valuation normalizes alongside margin recovery.

Breaking Down the Case for Edward Lifesciences

Edwards Lifesciences (EW) exited this month’s earnings with Q4 sales of $2 billion and 2026 adjusted EPS guidance of $3, reinforcing confidence in 2026 volume and mix as Transcatheter Mitral and Tricuspid Therapies (TMTT) momentum carried into 2025.

Edward Lifesciences stock’s Revenue reached $6 billion in 2025 with $5 billion of gross profit, reflecting scale in structural heart even as cost headwinds moderated gross margin to 78% from 80% in 2024.

EW stock’s operating expenses expanded to $3 billion in 2025 and operating income declined to $1 billion, pushing operating margin down to 21% as Edwards Lifesciences funded patient access initiatives and commercial buildout ahead of new therapy launches.

Meanwhile, FDA approval of SAPIEN M3 last December adds a new replacement leg alongside repair and tricuspid systems, while Q4 TMTT sales of $156 million and 2026 TMTT guidance of $740 million to $780 million establish a faster-growth mix inside the portfolio.

Management explicitly framed intent around execution and visibility, with CEO Bernard Zovighian stating on Q4 2025 earnings call that “we have increased confidence in meeting our 2026 full year sales growth rate guidance of 8% to 10% and earnings per share guidance of $2.90 to $3.05.”

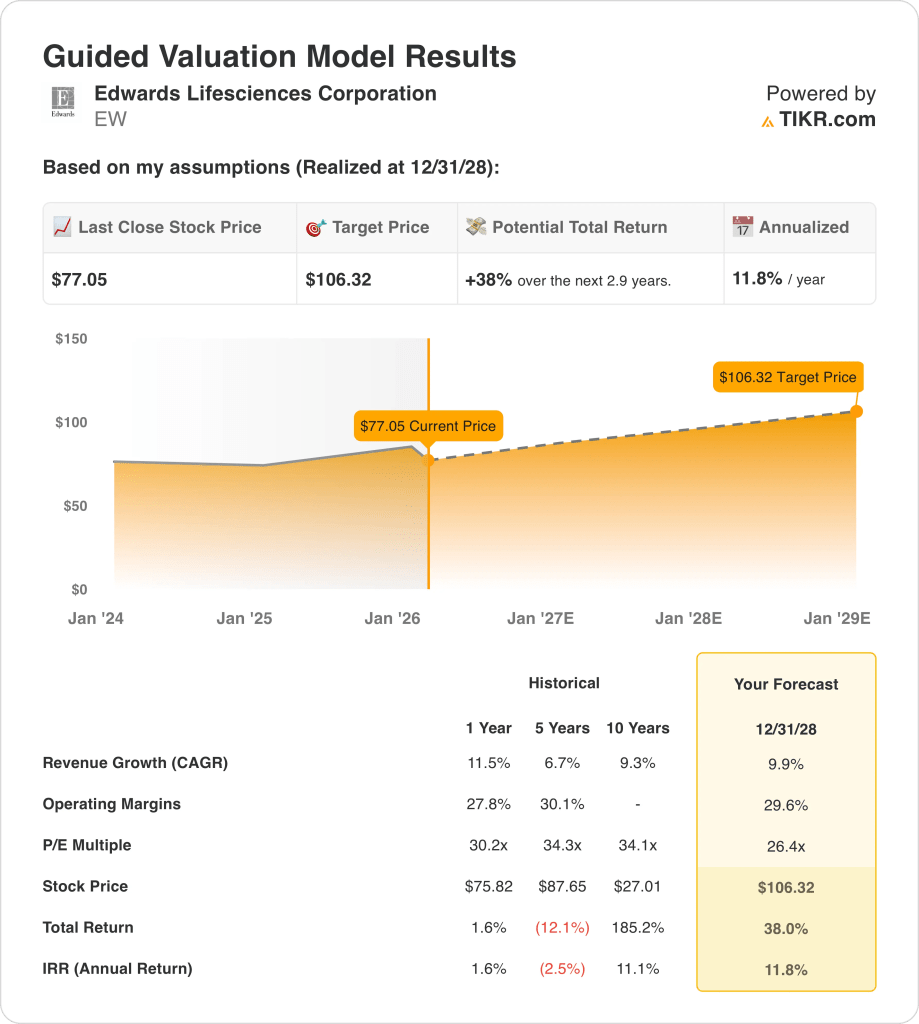

The market now discounts this setup at $77 versus a modeled $106 12/31/28 value on 26x earnings, creating tension between a 10% growth path and the 21% current operating margin that still trails a 29% 2026 target band.

What the Model Says for EW Stock

Edwards Lifesciences pairs 11.5% LTM revenue growth with 27.1% EBIT margins and 78.0% gross margins, reflecting durable structural heart positioning but recent operating deleverage from 30.5% EBIT margins in 2021.

The market assumption embeds 9.9% revenue growth and 29.6% operating margins versus 27.1% in 2025, alongside a 26.4x exit P/E below the recent 30.9x NTM average, producing a $106.32 target price by 12/31/28.

That implies 38.0% total upside from $77.05 and an 11.8% annualized return over 2.9 years, exceeding a 10% equity hurdle but below prior 10-year IRR of 11.1%.

Therefore, the model signals a conservative a Buy, as an 11.8% annualized return at 26.4x reflects multiple compression from 31.2x historical levels while margin recovery toward 29.6% restores earnings leverage.

An 11.8% annualized return modestly exceeds a 10% equity hurdle rate and reflects normalization from 30.9x NTM P/E toward 26.4x, implying compensated but measured capital appreciation relative to historical 34.3x five-year multiples, consistent with a disciplined Buy decision.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Edward Lifescience stock:

1. Revenue Growth: 9.9%

Edward Lifesciences stock revenue increased 11.5% in 2025 to $6.07 billion after declining 9.4% in 2024, while the 5-year CAGR stands at 6.7%, showing a business that has alternated between acceleration and digestion phases.

The model assumes 9.9% growth through 12/31/28, below the recent 11.5% rebound yet above the 5-year 6.7% rate, supported by 2026E revenue of $6.65 billion and continued TAVR and TMTT mix expansion.

Sustaining 9.9% requires consistent procedure growth and pricing stability as gross margins already sit at 78%, and any slowdown from 11.5% compresses operating leverage given fixed commercial investments.

This is below the 1-year historical revenue growth of 11.5%, as growth moderates after a rebound year and scale approaches $7 billion, and valuation expansion depends on durability rather than acceleration.

2. Operating Margins: 29.6%

EW stock’s EBIT margins reached 30.5% in 2021, declined to 27.1% in 2025, and EBITDA margins fell from 33.0% to 30.7%, showing recent reinvestment pressure following peak profitability.

The model assumes 29.6% operating margins by 2028, above the 27.1% 2025 level yet below the 30.5% 2021 peak, consistent with 2026E EBIT margin of 28.7% and incremental scale benefits.

Margin recovery depends on SG&A discipline after expenses rose to $3.49 billion in 2025, and slower revenue growth from 9.9% limits operating leverage while manufacturing expansion continues.

This is above the 1-year historical operating margin of 27.1%, as reinvestment moderates and scale improves mix, and earnings expansion must come from cost containment rather than pricing uplift.

3. Exit P/E Multiple: 26.4x

The Market assumption for Edward Lifesciences stock’s normalized earnings was 31.19x in 2024 and 30.93x at 12/31/25, declining to 26.44x this Februrary as growth expectations reset.

The model applies a 26.4x exit multiple on normalized earnings of $2.93 in 2026E, below prior 30x levels and aligned with the Market assumption of 26.44x on 2/10/26.

Therefore, applying 26.4x assumes valuation stability despite revenue growth moderating to 9.9% and margins at 29.6%, and any earnings miss from the $1.91 billion 2026E EBIT base would compress equity value quickly.

This is below the 1-year historical P/E of 30.19x, as valuation resets toward normalized growth and scale maturity, and upside depends on earnings delivery rather than multiple expansion.

What Happens If Things Go Better or Worse?

Edwards Lifesciences stock results hinge on TAVR volume durability, TMTT adoption pace, and cost discipline through 2030.

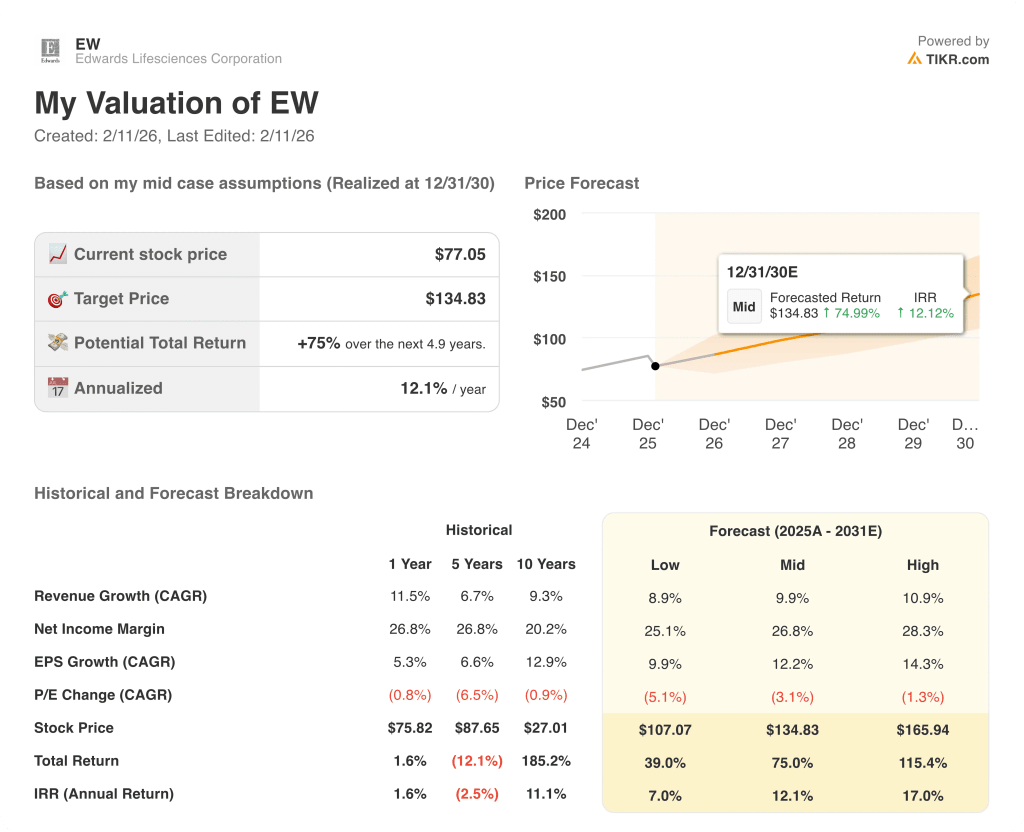

- Low Case: If procedure growth slows and investment spending persists, revenue grows around 8.9% and net income margin stays near 25.1% → 7.0% annualized return.

- Mid Case: With TAVR stable and TMTT scaling steadily, revenue growth near 9.9% and net income margin at 26.8% → 12.1% annualized return.

- High Case: If new indications expand access and mix improves, revenue reaches about 10.9% and net income margin approaches 28.3% → 17.0% annualized return.

How Much Upside Does Edward Lifesciences Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!