Key Takeaways:

- Tariff-Capped Guidance: AMETEK set 2026 adjusted EPS guidance at $8 to $8, below the $8 consensus midpoint, as tariff uncertainty creates near-term demand risk across industrial tools.

- Acquisition-Backed Momentum: AMETEK added LKC Technologies on February 3, 2026 to expand ophthalmic exposure after the $920 million FARO deal in 2025, while Q4 sales reached $2 billion and backlog hit $4 billion.

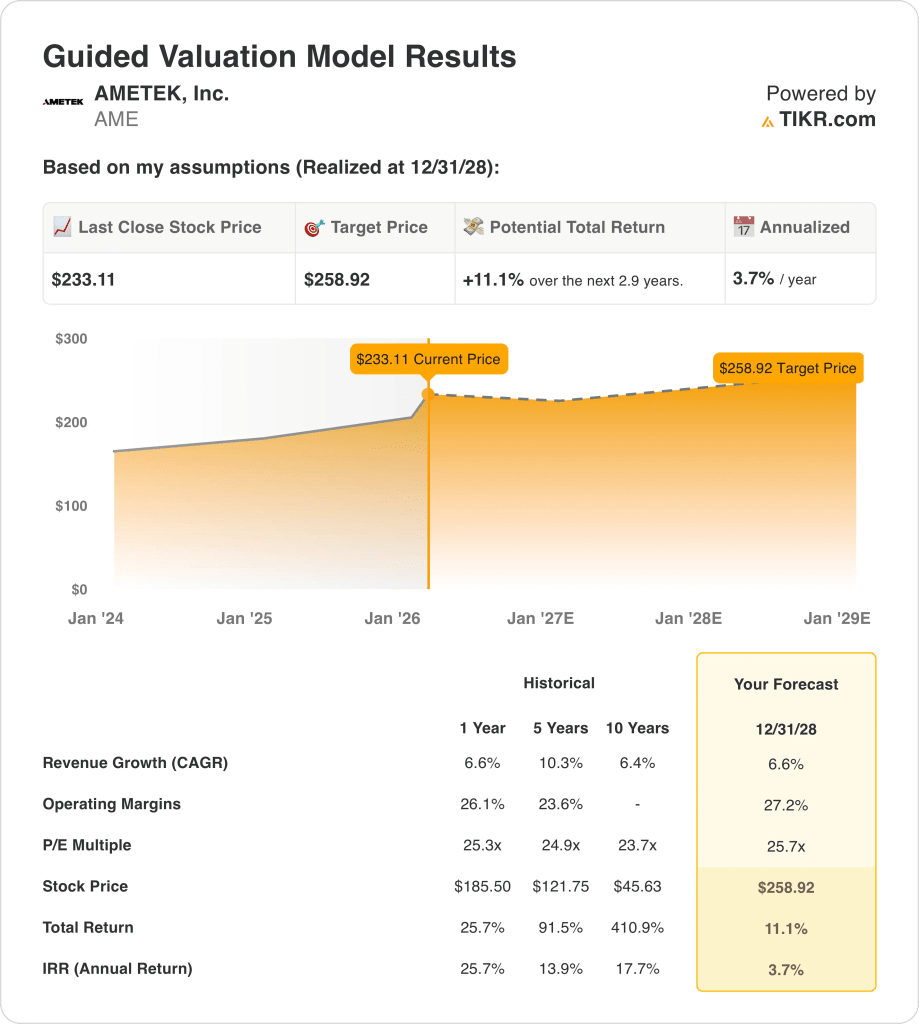

- Price Projection: AMETEK stock could reach $259 by 2028 as the model capitalizes 7% revenue growth, 27% operating margins, and a 26x exit P/E.

- Return Math: AMETEK upside totals 11% from the $233 price to $259, implying a 4% annualized return over 3 years.

Breaking Down the Case for AMETEK

AMETEK, Inc. (AME) entered 2026 with tariff uncertainty shaping its outlook after it guided 2026 adjusted EPS to $8 and announced the LKC Technologies acquisition on February 3, 2026.

AMETEK expands its ophthalmic diagnostics portfolio through the acquisition of LKC Technologies, increasing healthcare exposure within its Electronic Instruments Group and deepening participation in recurring medical instrumentation demand.

AME stock’s gross profit reached $3 billion in 2025, and $1 billion of operating expenses supported $2 billion of operating income at a 26% operating margin.

Q4 2025 results showed revenue of $2 billion and operating margin of 26%, and orders of $2 billion supported a $4 billion backlog entering 2026.

CEO David Zapico stated on the Q4 2025 earnings call, “We could spend $5 billion and still maintain our investment-grade credit rating,” underscoring that with $2 billion in debt and 1x gross leverage, acquisitions remain the top capital deployment priority over the next 1 year.

With the stock at $233 and the model’s $259 target by 2028, the market prices AMETEK near 26x earnings even as the modeled 4% annualized return trails a typical 10% equity hurdle.

What the Model Says for AME Stock

AMETEK stock sustains 26.2% operating margins on $7.40 billion revenue, yet incremental capital deployment raises expectation sensitivity.

The model applies 6.6% revenue growth, 27.2% operating margins, and a 25.7x exit multiple, producing a $258.92 target price.

That equates to 11.1% total upside and a 3.7% annualized return, below typical 10% equity hurdles.

The model signals a Sell, as 3.7% annualized return fails to compensate for industrial cyclicality and 25.7x valuation risk.

A 3.7% annualized return sits well below a 10% equity hurdle rate and offers limited capital appreciation relative to cyclical and multiple compression risks, indicating insufficient risk-adjusted compensation at 25.7x.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Ametek stock:

1. Revenue Growth: 6.6%

Total revenue of AMETEK stock rose from $5.55 billion in 2021 to $7.40 billion in 2025, which implies a 4-year CAGR near 7%, and the latest 1-year increase of 6.6% aligns with stabilized industrial demand.

Revenue reached $7.40 billion in 2025 and increased 6.6% year over year, as acquisitions added scale and core aerospace, power, and medical segments contributed steady organic expansion.

The model holds 6.6% growth through 2028, and that assumption requires consistent bolt-on acquisitions and durable pricing power, while cyclical end markets and tariff exposure can reduce volume momentum.

This matches the 1-year historical revenue growth of 6.6%, and the model assumes steady execution rather than acceleration, as acquisition dependence limits upside while constraining severe contraction.

2. Operating Margins: 27.2%

AMETEK stock’s operating margins improved from 23.6% in 2021 to 26.2% in 2025, as portfolio mix shifted toward higher-value instrumentation and fixed costs absorbed revenue growth across a $7.40 billion base.

The 2025 margin of 26.2% incorporated pricing discipline and acquisition cost control, and the model advances this to 27.2% as integration benefits persist and incremental margins remain above 30%.

The 27.2% assumption requires disciplined integration of recent transactions and sustained cost control, while lower-margin deal mix or softer demand would reduce incremental profitability.

This stands above the 1-year historical operating margin of 26.1%, and the model presumes continued mix improvement and cost absorption, as valuation stability rests on preserving current margin quality rather than expansion.

3. Exit P/E Multiple: 25.7x

The exit multiple capitalizes AMETEK stock’s normalized earnings from a business generating 26.2% operating margins and mid-single-digit revenue growth, which anchors terminal valuation to durable industrial instrumentation profitability.

The model applies a 25.7× P/E multiple, which is relatively below the market assumption of 28.95× for the next twelve months.

At 25.7×, the valuation assumes earnings durability without premium re-rating, while any earnings shortfall would likely compress the multiple rather than expand it further.

This is above the 1-year historical P/E of 25.3×, as sustained margin discipline and acquisition execution must hold, and valuation stability depends on preserving current earnings quality.

What Happens If Things Go Better or Worse?

AMETEK stock is driven by acquisition discipline, pricing power in niche instrumentation, and industrial demand stability, setting up a range of possible trajectories through 2030.

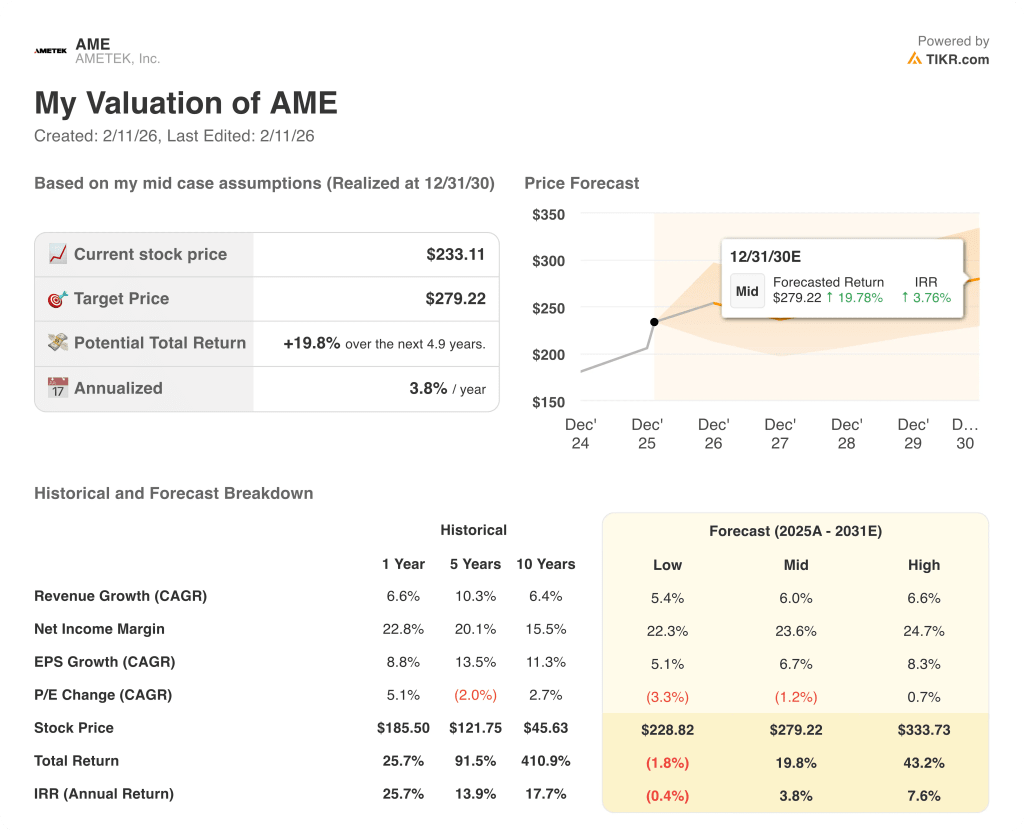

- Low Case: If industrial demand softens and integration benefits stall, revenue grows 5.4% and net margins hold near 22.3% → -0.4% annualized return.

- Mid Case: With steady aerospace, power, and medical demand, revenue grows 6.0% and net margins reach 23.6% → 3.8% annualized return.

- High Case: If acquisitions scale efficiently and pricing remains firm, revenue grows 6.6% and net margins expand to 24.7% → 7.6% annualized return.

How Much Upside Does Ametek Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!