Key Takeaways:

- Türkiye Consolidation Move: Uber Technologies committed $335 million to acquire 100% of Getir’s food delivery business and invested another $100 million for a 15% stake, adding over $1 billion in gross bookings exposure in 2025.

- Autonomous Expansion: Uber Technologies partnered with Baidu to launch autonomous ride hailing in Dubai in 2026, targeting deployment of thousands of vehicles as Baidu scales beyond 22 cities and 17 million completed rides.

- Price Projection: Uber Technologies could reach $130 by 2028 based on 13% revenue growth, 16% operating margins, and a 22x earnings multiple, reflecting disciplined margin expansion from 11% in 2025.

- Valuation Math: Uber Technologies implies 77% upside from the current $73 price, equating to a 22% annual return over nearly 3 years if execution aligns with margin and multiple assumptions.

Breaking Down the Case for Uber

Uber Technologies, Inc. (UBER) is accelerating international delivery consolidation and autonomous mobility expansion in 2026, committing $335 million for Getir’s food assets and integrating robotaxi services in Dubai to strengthen marketplace density and margin durability.

Revenue reached $52 billion in 2025, rising 18% year over year, while gross profit expanded to $18 billion with gross margins improving to 34%, reflecting improved take rates and disciplined cost structure across mobility and delivery.

Uber’s operating expenses totaled $12 billion in 2025, supporting operating income of $6 billion and lifting operating margins to 11%, a marked improvement from negative margins 3 years earlier.

Management framed the strategic pivot clearly, stating it intends to “rapidly grow through the adoption of autonomous vehicles and expansion into other countries,” reinforcing a capital allocation shift toward scalable, technology driven assets.

The $335 million Getir acquisition builds on a prior $700 million Trendyol Go transaction in 2025, consolidating exposure to over $3 billion in combined gross bookings across Türkiye’s delivery ecosystem.

Meanwhile, the Baidu partnership extends autonomous services beyond 22 global cities and leverages more than 17 million completed robotaxi rides, positioning the platform to compress driver cost intensity over time.

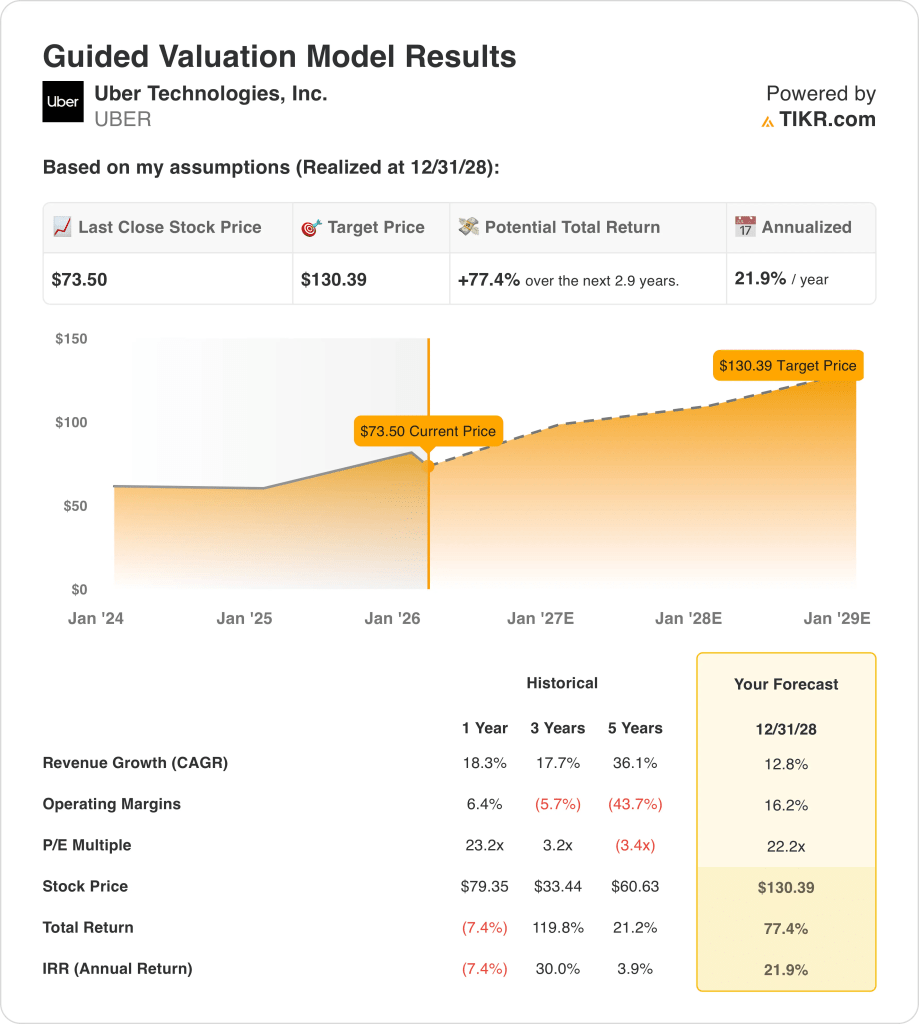

Despite revenue growth moderating toward 13% through 2028, the valuation framework assumes 16% operating margins and a 22x earnings multiple, implying a $130 price target from the current $73 level.

The market must reconcile a 21% quarterly stock decline against a business delivering $10 billion in projected EBITDA by 2026, leaving open whether margin durability justifies a sustained 22x earnings multiple.

What the Model Says for Uber Stock

Uber sustains 18.3% historical revenue growth while forward market assumptions compress NTM EV to EBITDA from 21.37x to 14.47x and lift free cash flow yield to 6.8%, reflecting moderated expectations despite improving scale economics.

The model assumes 12.8% revenue growth and 16.2% operating margins with a 22.2x exit multiple, above the current 19.23x NTM EV to EBIT market assumption, producing a $130.39 target price.

That implies 77.4% total upside from $73.50 and a 21.9% annualized return over 2.9 years, exceeding returns implied by a 6.8% free cash flow yield market assumption.

The model signals a Buy, as a 21.9% annualized return at a 22.2x exit multiple compensates for execution risk embedded in current 14.47x to 19.23x market assumptions.

A 21.9% annualized return exceeds a 10% equity hurdle rate and reflects margin expansion from 11% toward 16.2%, justifying valuation normalization above current 14.47x to 19.23x market assumptions.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Uber stock:

1. Revenue Growth: 12.8%

Uber stock’s revenue expanded 18.3% over the last year and 17.7% over three years, while scale increased to $52 billion, indicating the business has transitioned from recovery acceleration toward normalized expansion.

Gross profit reached $18 billion at a 34% margin in 2025, and recent Türkiye transactions add over $3 billion in gross bookings exposure that can support mid-teens marketplace growth.

The 12.8% assumption depends on sustained rider frequency, delivery density gains, and stable take rates, and any pricing pressure or demand softness would reduce incremental revenue conversion quickly.

This is below Uber stock’s 1-Year historical revenue growth of 18.3%, as post-pandemic normalization moderates volume expansion and valuation rests on steadier marketplace compounding instead of continued rebound acceleration.

2. Operating Margins: 16.2%

Operating margins improved to 11% in 2025 from negative levels three years earlier, and scale leverage plus disciplined operating expenses of $12 billion lifted operating income to $6 billion.

The model assumes a 16.2% margin as gross margins remain near 34% and revenue approaches $58 billion, and fixed-cost absorption increases operating income across mobility and delivery.

The margin target requires autonomous initiatives and international density to offset labor and regulatory cost pressure, and any execution shortfall reduces earnings sharply as contribution margins determine incremental profit.

This is above Uber stock’s 1-Year historical operating margin of 6.4%, because cost resets and mix improvements must continue at scale, and valuation relies on sustained operating leverage instead of expense expansion.

3. Exit P/E Multiple: 22.2x

The model’s assumption for Uber stock’s 22.2x exit multiple capitalizes terminal earnings after 12.8% growth and 16.2% margins, treating normalized net income as durable within a global marketplace platform generating over $10 billion in projected EBITDA.

This multiple closely matches the Market assumption of 22.24x NTM Price to Normalized Earnings for 2026, while current EV to EBIT trades at 19.23x and EV to EBITDA at 14.47x.

Selecting 22.2x avoids layering optimism on top of margin expansion, since earnings growth already captures scale benefits and terminal valuation assumes stable profitability rather than structural re-rating.

This is below the 1-Year historical P/E of 23.2x, because recent multiple compression reflects higher rate sensitivity and competitive risk, and valuation depends on earnings durability rather than renewed multiple expansion.

What Happens If Things Go Better or Worse?

Uber stock hinges on marketplace demand durability, delivery consolidation execution, and margin discipline through 2028.

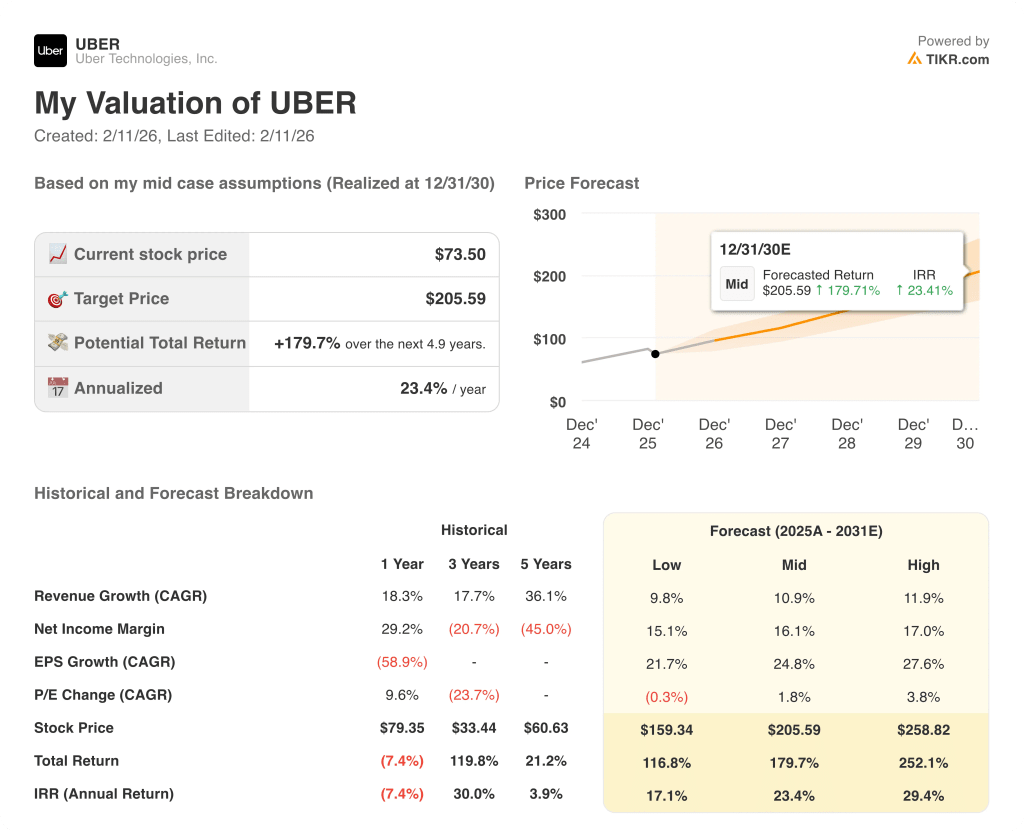

- Low Case: If mobility growth slows and cost leverage stalls, revenue grows 12.8% and margins hold 16.2% → 21.9% annualized return.

- Mid Case: With delivery scale integrating smoothly and pricing stable, revenue grows 12.8% and margins reach 16.2% → 21.9% annualized return.

- High Case: If autonomous rollout improves unit economics and density rises, revenue grows 12.8% and margins hit 16.2% → 21.9% annualized return.

How Much Upside Does Uber Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!