Key Stats for Avantor Stock

- This Week Performance: -3%

- 52-Week Range: $8.4 to $18

- Current Price: $8.8

What Happened?

Avantor (AVTR) shed its identity as a unified life sciences supplier on February 11, splitting into two distinct businesses — VWR Distribution and Services and Bioscience and Medtech Products — a structural overhaul that reframes AVTR, now trading at $8.78, as a turnaround story with clearer accountability and brand equity.

The immediate catalyst was Q4 earnings: revenue of $1.66 billion beat the $1.64 billion consensus, though adjusted EPS of $0.22 merely matched estimates, and net income collapsed 89.6% year-over-year to $52.4 million as $785 million in full-year impairment charges weighed heavily.

The sharpest forward signal sits inside Bioscience and Medtech Products, where process chemicals exited 2025 with a book-to-bill above 1 and an order book up high single digits year-to-date, even as operational bottlenecks delayed full revenue conversion.

Additionally, CFO Brent Jones stated on the Q4 earnings call that “Q1 bears the additional burden of being the historically softest quarter of the year for our industry,” connecting directly to guidance of just $0.15 to $0.16 in Q1 EPS before a projected back-half recovery.

Still, the company guided full-year adjusted EPS of $0.77 to $0.83 against a stock trading near its 52-week low of $8.43, implying a forward P/E of roughly 11x as director Gregory T. Lucier bought 50,000 shares on February 23, a vote of confidence from inside the boardroom.

The VWR relaunch, $10 million to $15 million e-commerce investment, and separation of high-margin manufactured products from the distribution engine give Avantor a cleaner margin structure to defend over the next three to five years, provided the Revival program converts its strong bioprocessing order book into organic growth by late 2026.

Wall Street’s Take on AVTR Stock

The VWR resegmentation and Revival program shift the investment narrative, but the financials confirm AVTR remains in contraction, with 2026 consensus revenue of $6.50 billion implying another 0.8% decline following four consecutive years of shrinking top-line results.

Fundamentally, EBITDA is forecast to compress further to $970 million in 2026, down 9% year-over-year, while EBIT margins are expected to narrow to 13.3% from 14.6% in 2025, extending a deterioration that began in 2022.

Wall Street holds 14 analysts at “hold,” 3 at “buy,” and 1 at “sell,” with a mean price target of $10.89, implying just 24.1% upside from the current $8.78 price, a modest premium that reflects deep skepticism about Revival’s near-term execution capacity.

The target range spans $8.00 on the low end to $19.00 on the high end, where the bear case prices in continued organic decline and margin compression while the bull case rewards successful bioprocessing order book conversion and VWR e-commerce traction.

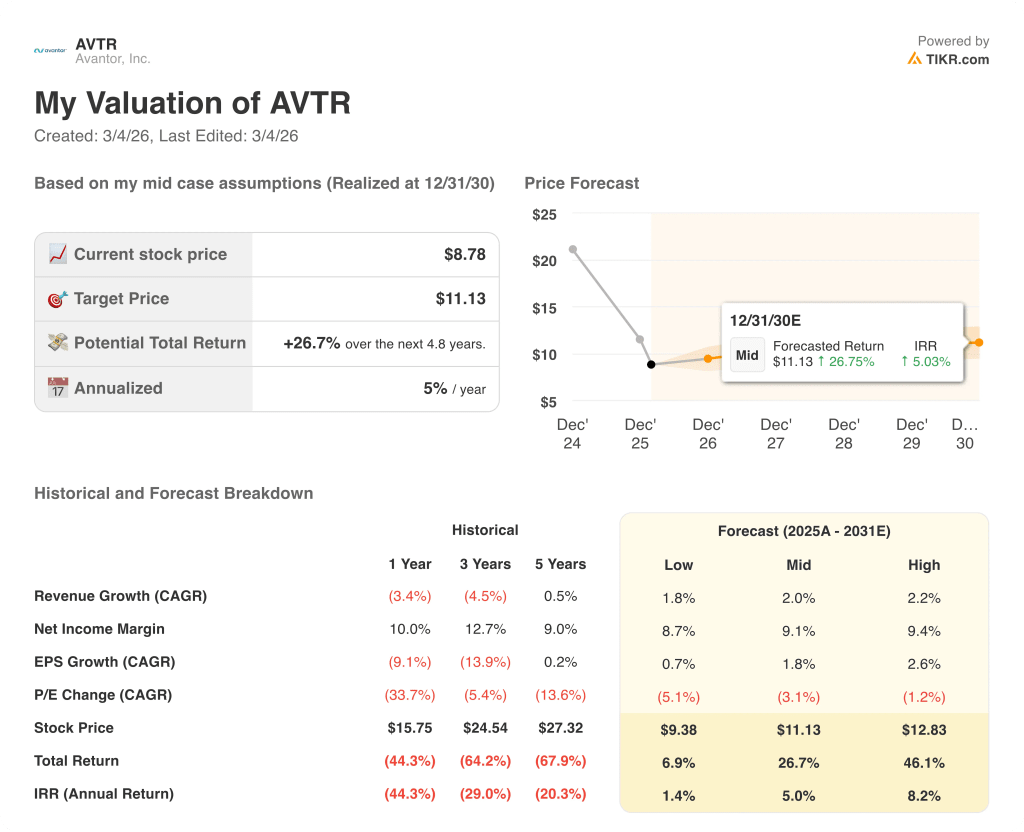

What Does the Valuation Model Say?

The valuation model targets $11.13 by December 2030, a 26.7% total return over nearly five years, implying only a 5% annualized IRR at current prices, which barely compensates investors for the execution risk embedded in a multi-year turnaround.

However, the market appears to be pricing AVTR as a structurally declining distributor, yet the Bioscience and Medtech Products segment carries a 26.7% adjusted operating margin, a premium manufacturing profile the current $8.78 price does not reflect.

Also, its normalized EPS is forecast at $0.79 for 2026, down 12.1% year-over-year, yet director Gregory T. Lucier purchased 50,000 shares on February 23, signaling insider conviction that the stock trades well below intrinsic value at this level.

The risk that breaks the thesis is leverage: at 3.2x adjusted EBITDA with EBITDA declining toward $970 million in 2026, debt reduction targets below 3x become materially harder to achieve.

The single clearest signal for the bull case will be Q3 2026 organic revenue growth, where management has explicitly guided for sequential improvement throughout the year.

AVTR is a deep-value turnaround with a credible brand restructuring thesis, but the Revival program’s execution through 2026 determines whether the stock re-rates or stagnates near its 52-week low.

Should You Invest in Avantor, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AVTR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Avantor, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AVTR stock on TIKR for Free →