Key Stats for Westlake Corporation Stock

- Past-Week Performance: +11%

- 52-Week Range: $56.3 to $113.5

- Current Price: $102.9

What Happened?

Westlake‘s three-pillar restructuring plan targets $600M in EBITDA improvement for 2026, a self-help story powerful enough to lift WLK 11% in a single week to $102.92 despite a Q4 net loss of $544M on $511M of plant shutdown charges.

The immediate trigger was Q4 earnings on February 24, where adjusted EPS of -$0.25 demolished the -$1.43 consensus estimate as Westlake Corporation began realizing savings from closing three North American chlorovinyl plants, one styrene asset, and its Pernis epoxy facility.

The $600M improvement breaks into three equal $200M contributions: footprint optimization already underway, plant reliability gains from dramatically fewer 2026 turnarounds, and incremental structural cost reductions layered on top of the $170M already achieved in 2025.

Separately, Westlake closed the ACI acquisition in January, adding silicon and crosslinked polyethylene to the HIP segment, while guiding 2026 HIP revenue of $4.4B to $4.6B at a 19% to 21% EBITDA margin.

CEO Jean-Marc Gilson stated on the Q4 earnings call that “2026 represents an inflection point following the actions we have taken to optimize our manufacturing footprint,” directly connecting to China’s April 1 removal of its 13% PVC export duty drawback, which has already pushed global export prices higher.

With 16-year average debt maturity, $2.9B in cash, a vertically integrated chlorovinyls and polyethylene chain running at higher utilization, and HIP positioned as supplier of choice for major national homebuilders, Westlake Corporation enters a multi-year cost advantage cycle that competitors without integrated feedstock positions cannot easily replicate.

Wall Street’s Take on WLK Stock

The $600M EBITDA improvement plan and February 24 earnings beat directly support a forward recovery, with consensus projecting 2026 EBITDA rebounding 38.1% to $1.58B after a 50% collapse in 2025, anchored by the three pillars already in execution.

The fundamental case strengthens further when pairing that EBITDA recovery with normalized EPS swinging from -$0.90 in 2025 to a projected $1.39 in 2026, a 254% recovery driven by footprint rationalization, fewer planned turnarounds, and incremental cost savings.

Wall Street currently shows 6 buys, 1 outperform, and 8 holds with a mean price target of $108.21, implying just 5.1% upside from $102.92, suggesting analysts believe the restructuring is credible but want execution proof before upgrading.

The target range spans $80.00 on the low end to $129.00 on the high end, where the bear case prices in persistent PEM overcapacity and global pricing weakness while the bull case rewards full delivery of the $600M three-pillar plan and China’s April 1 duty drawback removal.

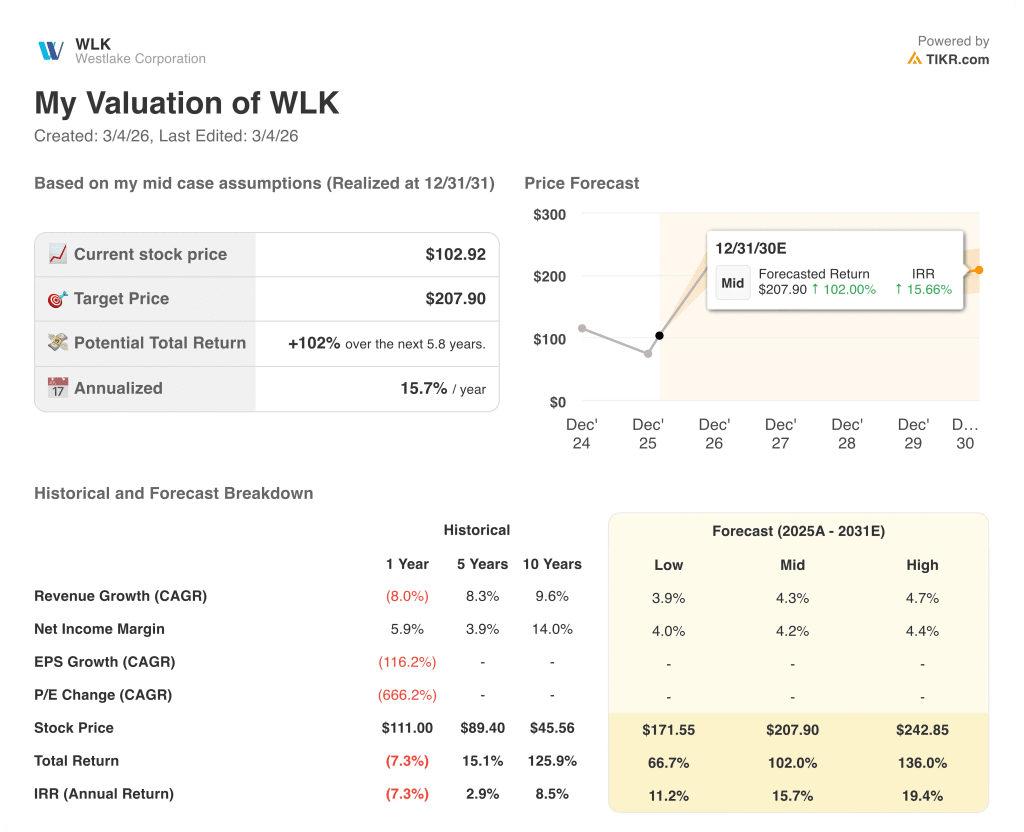

What Does the Valuation Model Say?

The valuation model targets $207.90 by December 2031, implying 102% total return from current levels. That mid-case IRR of 15.7% annually stands in sharp contrast to a stock Wall Street currently rates just 5.1% above fair value.

However, the market appears to be underpricing Westlake’s 10-year revenue CAGR of 9.6% and its historically demonstrated ability to generate 14% net income margins at the top of the cycle.

At $102.92, WLK trades on a trough earnings base while the forward model targets a return to $207.90, a gap that the $600M self-help plan makes structurally achievable rather than cyclically dependent.

Management’s confidence is underpinned by $2.9B in cash, a 16-year average debt maturity, and $170M in structural savings already banked, signaling this is a company executing a plan, not hoping for a market recovery.

The risk that breaks the thesis is sustained global PEM overcapacity, particularly in polyethylene and chlorovinyls, which could prevent the $200M reliability and $200M footprint pillars from converting into realized margin improvement.

The single clearest confirmation of the bull case will be Q2 2026 PEM margins, where the combined effect of the April 1 China duty drawback removal and fewer planned turnarounds should first become visible in reported results.

Altogether, Westlake enters 2026 with $2.9B in cash and a concrete $600M profit improvement plan already in motion; whether the turnaround is real will show up in second-quarter chemical margins

Should You Invest in Westlake Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WLK stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Westlake Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WLK stock on TIKR for Free →