Key Takeaways:

- Mako Momentum: Installed base surpassed 3,000 systems worldwide, with two-thirds of U.S. knee procedures now performed robotically.

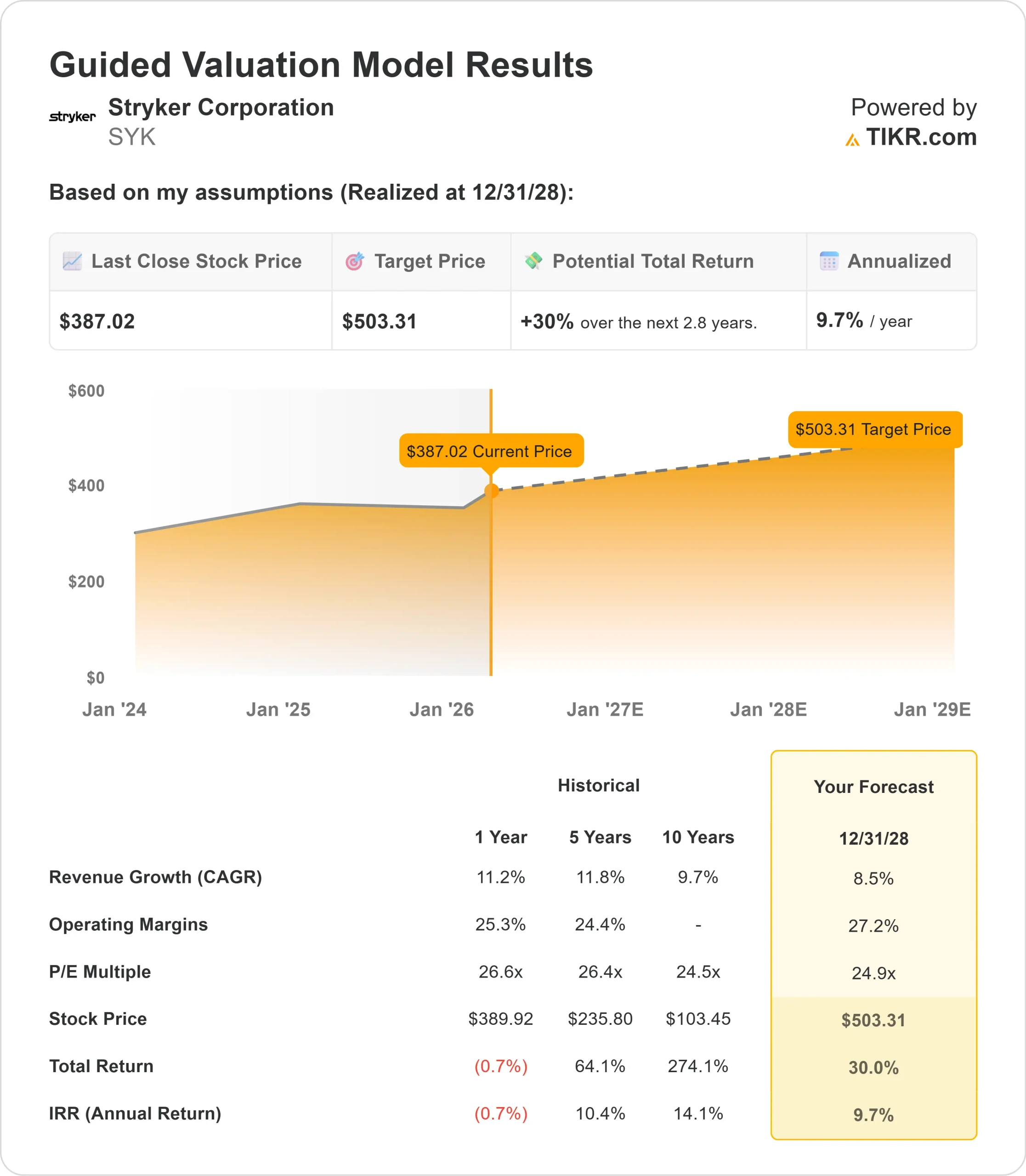

- Price Projection: Based on current execution, SYK stock could reach $503 by December 2028.

- Potential Gains: This target implies a total return of 30% from the current price of $387.

- Annual Return: Investors could see roughly 9.7% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Stryker Corporation (SYK) delivered exceptional Q4 results with 11% organic sales growth, capping off a remarkable year that saw revenues surpass $25 billion for the first time, marking its fourth consecutive year of double-digit expansion.

The company now expects to maintain momentum with 2026 organic growth guidance of 8% to 9.5%.

CEO Kevin Lobo highlighted the company’s structural growth drivers: exceptional talent and culture, active M&A, a steady cadence of product launches, and systematic specialization through new business units and sales force splits.

- The standout performer was Stryker’s Mako robotic platform. The company delivered record installations in Q4, expanding its global installed base to more than 3,000 systems.

- As the year closed, over two-thirds of U.S. knee procedures and one-third of hip procedures were performed on Mako.

- The transition to Mako 4 proved highly successful, with surgeons praising new applications, including revision hip capabilities.

- International markets present even stronger growth potential, particularly as regulatory approvals catch up to U.S. launches.

- Stryker’s MedSurg businesses also posted impressive results. Instruments grew 19.1% organically in the U.S., driven by demand for power tools and capital equipment.

- Endoscopy delivered 11.1% U.S. growth, with the company’s 1788 video platform continuing to gain traction years after its initial launch.

Despite facing $400 million in tariff headwinds for the full year, Stryker managed to expand adjusted operating margins by 100 basis points for the second consecutive year.

This demonstrates the operational efficiency and earnings power the company has built over time.

See analysts’ full growth forecasts and estimates for SYK stock (It’s free) >>>

What the Model Says for Stryker Stock

We analyzed Stryker through multiple lenses: its market-leading position in robotics, diversified MedSurg portfolio, and consistent margin expansion capabilities.

The company benefits from several structural tailwinds.

- Robotic-assisted surgery adoption continues to accelerate, with no ceiling in sight for penetration rates.

- Management believes robotics could eventually become the standard of care, unlike other surgical techniques, with natural adoption limits.

- Stryker’s MedSurg segment delivers exceptional growth through a proven playbook.

- The company maintains a dominant market share, continuously upgrades its products, makes strategic tuck-in acquisitions, and splits its sales forces to drive specialization.

- Recent examples include creating a dedicated breast care team within Endoscopy and separating the CMF sales force into oral maxillofacial and neuro divisions.

The balance sheet remains robust, providing firepower for M&A in 2026.

With each acquisition, Stryker opens new avenues for growth, whether in health IT following Vocera or in peripheral vascular after Inari.

Using a forecast of 8.5% annual revenue growth and 27.2% operating margins, our model projects the stock will rise to $503 within 2.8 years. This assumes a 24.9x price-to-earnings multiple.

That represents modest compression from Stryker’s historical P/E averages of 26.6x (one year) and 26.4x (five years). The slight compression acknowledges near-term tariff pressures and the inherent difficulty of maintaining double-digit growth as scale increases.

The real value lies in capturing long-term structural demand for robotic surgery while expanding the high-margin MedSurg portfolio through continuous innovation and strategic M&A.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SYK stock:

1. Revenue Growth: 8.5%

Stryker delivered 10.3% organic growth in 2025, up from 10.2% in 2024.

Management guides to 8% to 9.5% for 2026, with CEO Lobo noting that while comparisons get harder, the strong order book and Mako momentum provide confidence.

The company’s international markets should accelerate as key products, such as Insignia hip stems and Pangea plating systems, gain regulatory approval in Europe.

These products have already demonstrated strong traction in the U.S. but faced delays due to EU MDR regulations.

With Europe working to streamline its approval process, Stryker should see improved international growth.

2. Operating margins: 27.2%

This performance reflects operational excellence initiatives, including lean manufacturing, supply chain optimization, and the expansion of shared services.

Management targets at least 150 basis points of additional margin expansion through 2028, even as it absorbs substantial tariff costs.

The company demonstrated this capability in 2025, driving meaningful margin improvement despite $200 million in tariff headwinds.

3. Exit P/E Multiple: 24.9x

The market currently values Stryker at 25.8x earnings. We assume modest compression to 24.9x over our forecast period, reflecting the natural challenges of maintaining high growth rates at larger scale.

As Stryker continues demonstrating durable execution across robotics, MedSurg, and international markets, the company should command a premium multiple.

The entrepreneurial operating model with specialized sales forces provides agility to capture growth opportunities while managing market dynamics.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

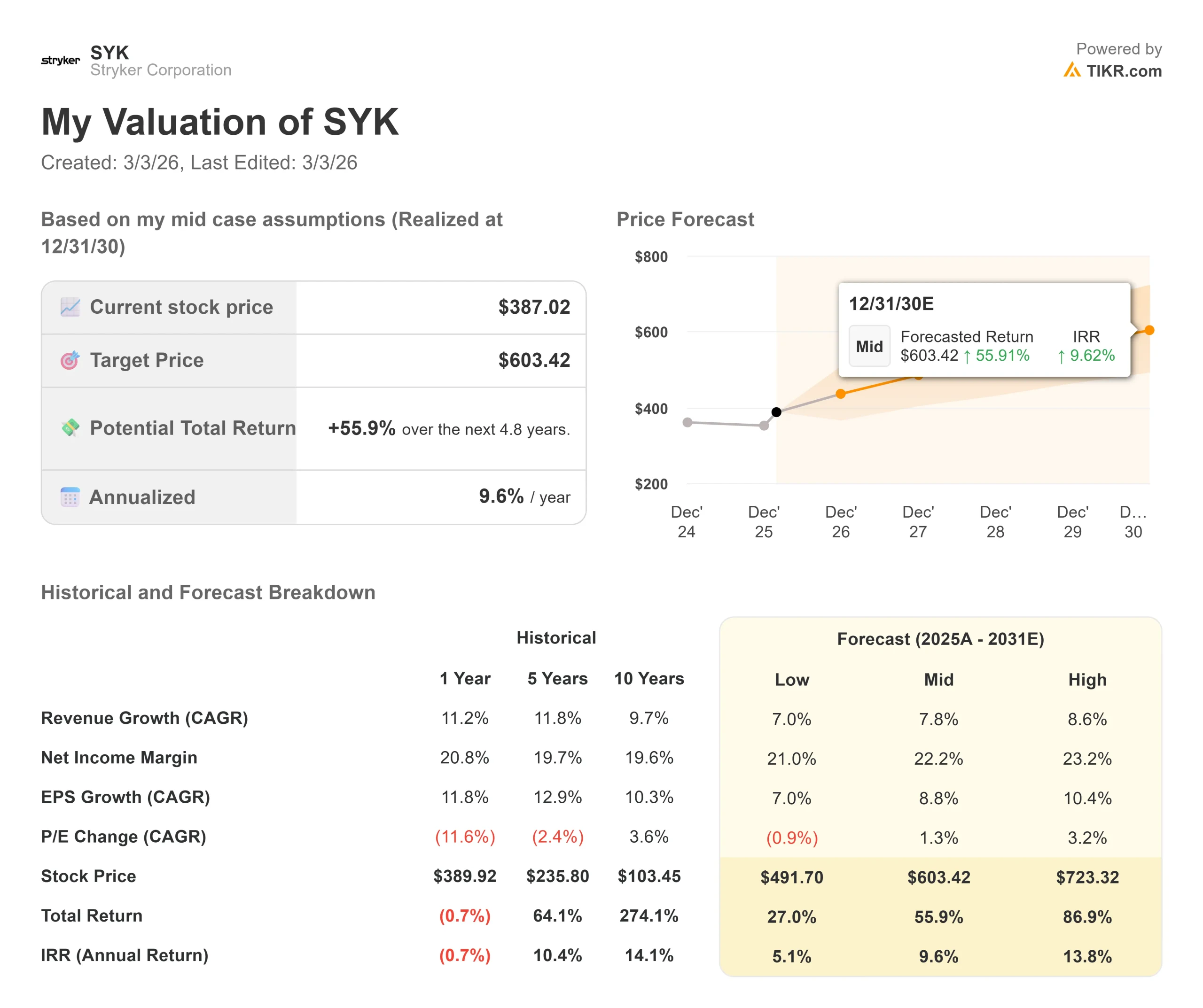

Medical device companies face technology adoption cycles and volatility in capital spending. Here’s how Stryker stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth moderates to 7% and net income margins compress to 21%, investors still see a 27% total return (5.1% annually).

- Mid Case: With 7.8% growth and 22.2% margins, we expect a total return of 56% (9.6% annually).

- High Case: If robotic adoption exceeds expectations and drives 8.6% revenue growth while Stryker maintains 23.2% margins, returns could hit 87% total (13.8% annually).

See what analysts think about SYK stock right now (Free with TIKR) >>>

The range reflects execution on Mako expansion, successful navigation of international launches, and the company’s ability to drive margin improvement through operational excellence while absorbing external cost pressures.

How Much Upside Does Stryker Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!