Key Takeaways:

- Consumer Finance Leader: Walmart partnership is the fastest-growing program launch in company history.

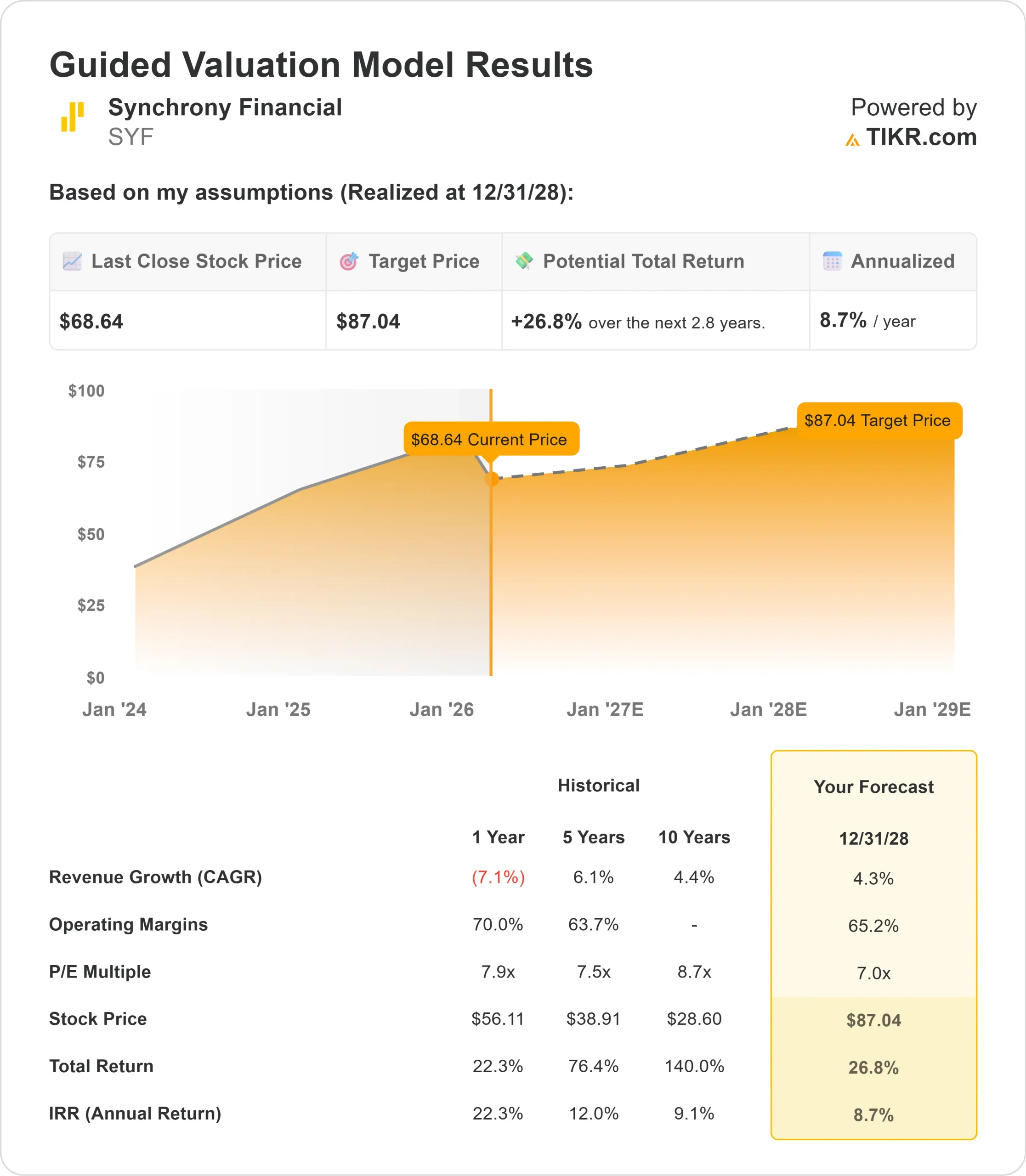

- Price Projection: Based on current execution, SYF stock could reach $87 by December 2028.

- Potential Gains: This target implies a total return of 27% from the current price of $69.

- Annual Return: Investors could see roughly 9% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Synchrony Financial (SYF) ended 2025 with strong momentum despite headwinds earlier in the year. The company reported Q4 net earnings of $2.04 per share and returned $3.3 billion to shareholders through buybacks and dividends.

CEO Brian Doubles highlighted accelerating purchase volume trends, with Q4 recording a 3% year-over-year increase to $49 billion. After a slow first half, spending patterns strengthened across nearly all platforms heading into year-end.

- The credit card issuer connected 70 million customers to its retail partners and generated over $182 billion in sales for merchants.

- Co-branded card purchase volume jumped 16% versus the prior year, driven by product upgrades and expanded utility.

- Credit performance improved significantly.

- The net charge-off rate declined to 5.37% in Q4, down 108 basis points from 6.45% a year earlier.

- This brought the full-year charge-off rate to 5.65%, within the company’s long-term target range of 5.5% to 6%.

- The Walmart partnership stands out as a major growth driver.

- Launched in September 2025, management called it the fastest-growing program in company history.

- The OnePay digital platform delivers a seamless experience, while Walmart+ members receive unlimited 5% cash back at Walmart and 1.5% everywhere else.

Despite strong fundamentals and improving credit, Synchrony trades at $69, offering upside for investors who recognize the company’s position in consumer financing and its expanding digital capabilities.

See analysts’ full growth forecasts and estimates for SYF stock (It’s free) >>>

What the Model Says for Synchrony Financial Stock

We analyzed Synchrony as it evolved into a digital-first consumer finance company, with strengthened partner relationships.

The company benefits from multiple growth catalysts.

- The Walmart partnership provides access to millions of customers through a best-in-class digital experience.

- Synchrony’s Pay Later product now operates at over 6,200 merchants, delivering at least 10% higher sales when offered alongside revolving credit.

- Health & Wellness continues outperforming, with partnerships across 35,000 small and mid-sized practices. The platform integration with companies like Weave eliminates friction in patient payment experiences while driving sales for providers.

- Management expects mid-single-digit loan receivables growth in 2026, accelerating in the second half as new programs mature.

- The Lowe’s commercial co-brand transfers to Synchrony’s portfolio in Q2, providing another boost.

Using a forecast of 4.3% annual revenue growth and 65.2% operating margins, our model projects the stock will rise to $87 within 2.8 years. This assumes a 7.0x price-to-earnings multiple.

That represents compression from Synchrony’s historical P/E averages of 7.9x (one year) and 7.5x (five years). The lower multiple reflects near-term headwinds from elevated payment rates and the yield-dilutive effect of rapid new-account growth.

The real value lies in Synchrony’s ability to compound earnings while returning substantial capital through an economic cycle, supported by its economic alignment model with partners.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SYF stock:

1. Revenue Growth: 4.3%

Synchrony’s growth centers on partner expansion and digital product innovation rather than broad credit loosening.

Purchase volume was positive in Q4, with momentum accelerating into early 2026.

The Walmart program provides significant upside given its rapid adoption and large customer base.

Health & Wellness investments continue paying off, while co-branded cards grew 16% in Q4, outpacing the overall portfolio.

Management projects mid-single-digit loan receivables growth for 2026, though elevated payment rates of 16.3% (155 basis points above pre-pandemic levels) will moderate balance growth.

2. Operating margins: 65.2%

The company’s Retailer Share Arrangements (RSAs) create economic alignment with partners, sharing program performance improvements.

While RSAs increased to 4.30% of receivables in Q4 due to better credit, they remain within the 4.0%-4.5% target range.

Technology investments in AI, cloud migration, and the Health & Wellness platform will drive efficiency over time while supporting growth initiatives.

3. Exit P/E Multiple: 7.0x

The market currently values Synchrony at 7.4x earnings. We assume modest compression to 7.0x over our forecast period, reflecting near-term uncertainty around loan growth timing.

Consumer finance companies typically trade at mid-to-high single-digit earnings multiples due to their sensitivity to the credit cycle.

Synchrony commands a premium due to its diversified partner base, with 97% of revenue secured from the top 25 partners through 2028.

As new programs like Walmart demonstrate sustained growth and credit remains stable, the multiple should stabilize near historical norms.

The company’s track record of generating 25% return on tangible common equity supports valuation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

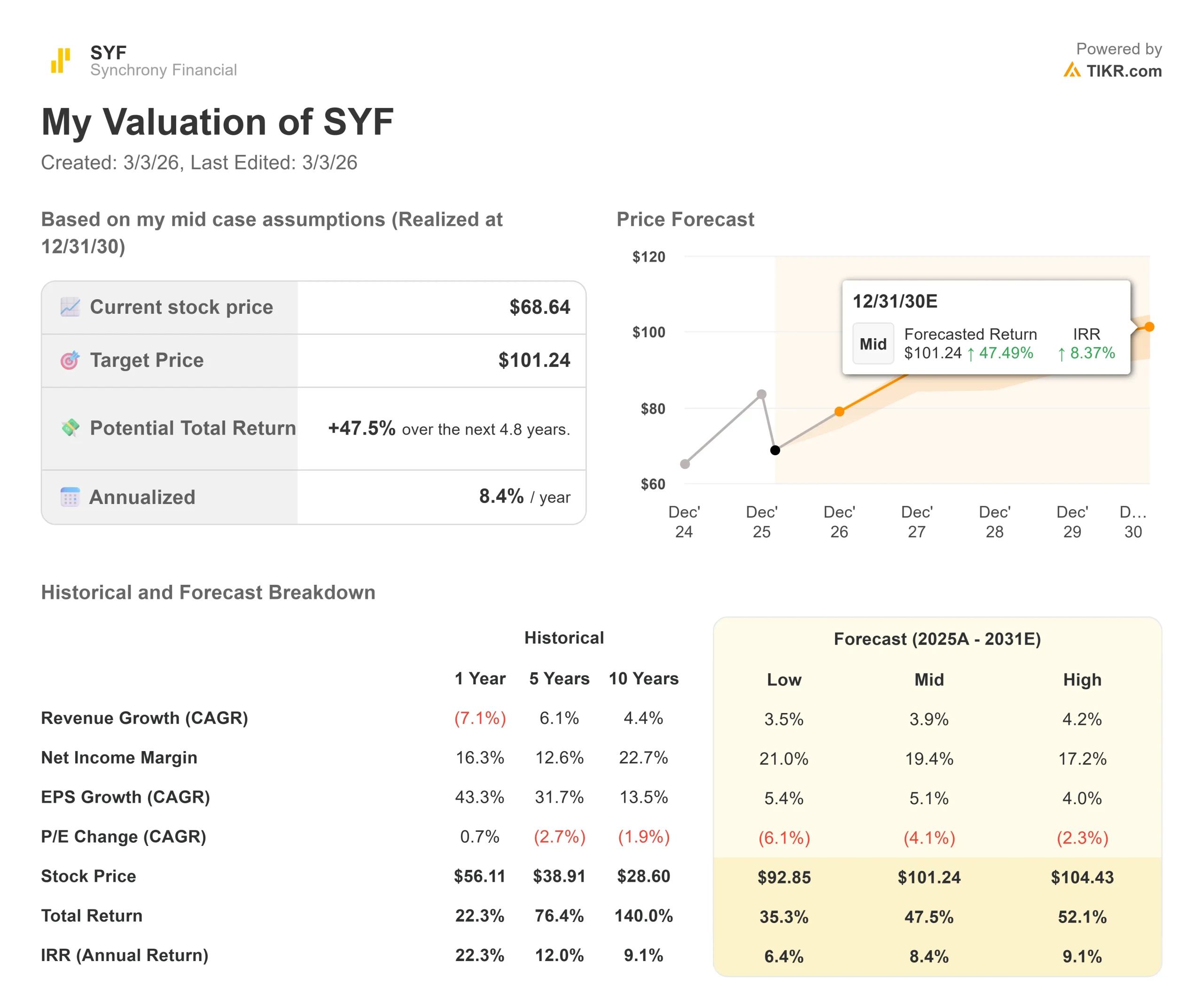

Consumer finance companies face economic cycles and shifts in consumer behavior. Here’s how Synchrony stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 3.5% and net income margins compress to 21.0%, investors still see a 35.3% total return (6.4% annually).

- Mid Case: With 3.9% growth and 19.4% margins, we expect a total return of 47.5% (8.4% annually).

- High Case: If consumer spending accelerates, driving 4.2% revenue growth while Synchrony maintains 17.2% margins, returns could hit 52.1% total (9.1% annually).

See what analysts think about SYF stock right now (Free with TIKR) >>>

The range reflects execution on the Walmart ramp, successful Health & Wellness expansion, and navigation of payment rate normalization.

In the low case, economic weakness drives higher charge-offs, or regulatory changes like APR caps significantly restrict lending.

In the high case, consumer confidence rebounds faster than expected, payment rates normalize downward, boosting receivables growth, and Pay Later adoption accelerates across the partner base.

How Much Upside Does Synchrony Financial Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!