Key Takeaways:

- Insurance Innovation: The Hartford is leveraging AI-first capabilities across claims, underwriting, and operations to drive competitive advantage.

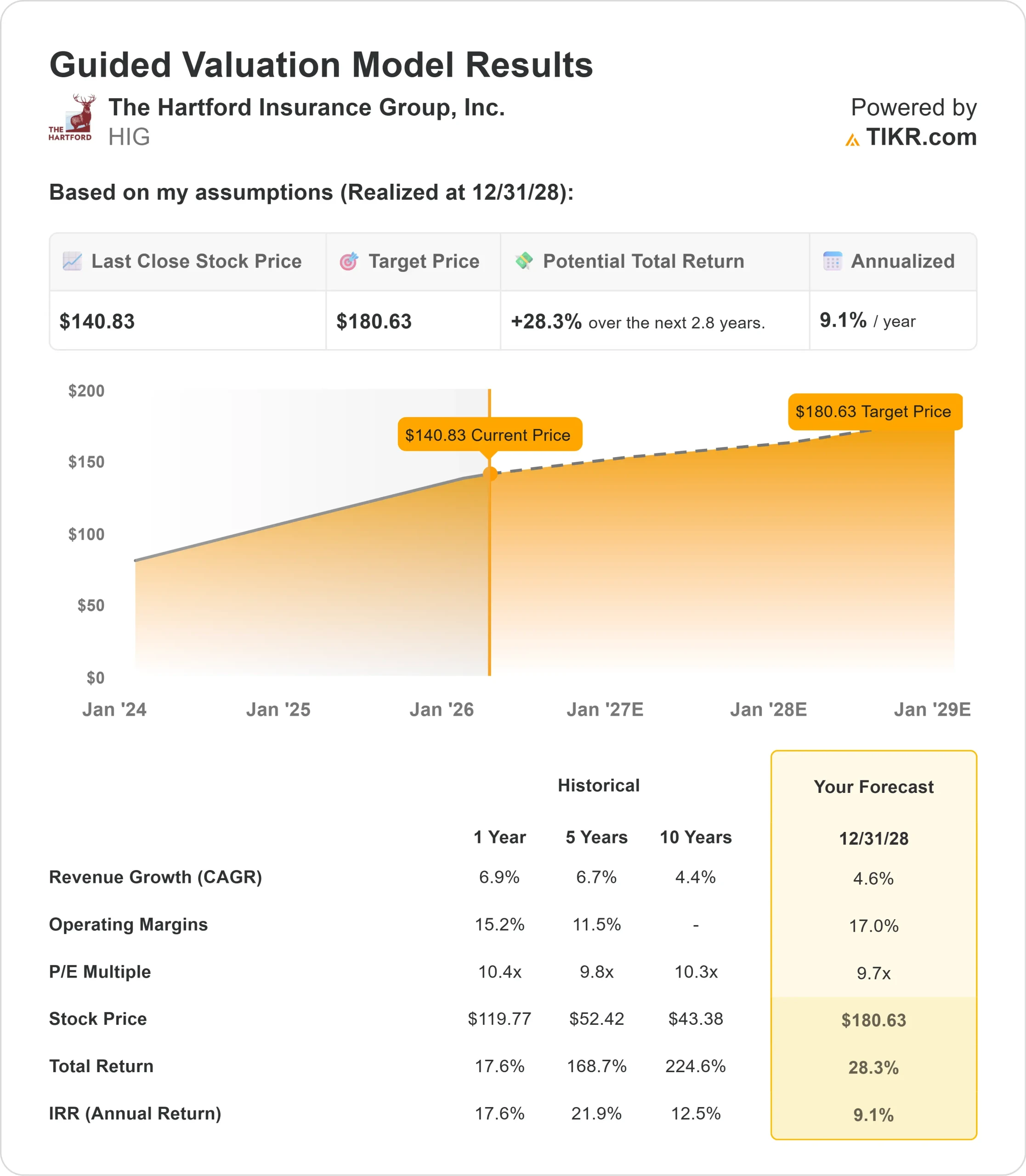

- Price Projection: Based on current execution, HIG stock could reach $181 by December 2028.

- Potential Gains: This target implies a total return of 28% from the current price of $141.

- Annual Return: Investors could see roughly 9% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

The Hartford Insurance Group (HIG) delivered outstanding Q4 and full-year 2025 results with core earnings of $3.8 billion and a core earnings ROE of 19.4%.

CEO Chris Swift emphasized the company’s technology-driven transformation, highlighting how AI is accelerating medical record summarization in claims, providing data-rich insights in underwriting, and enhancing customer interactions through Amazon’s call center technology.

- Business Insurance drove robust performance with 8% written premium growth and an excellent underlying combined ratio of 88.5%.

- Small Business unit maintained industry leadership with $6 billion in written premium and earned the #1 ranking from Keynova Group for digital capabilities for the seventh consecutive year.

- Increasing commercial activity supports continued demand for business insurance products. The Hartford’s focus on the SME segment, combined with advanced underwriting capabilities, positions the company to capture market share while maintaining strong profitability through market cycles.

- Personal Insurance achieved a pivotal turnaround in 2025, with auto reaching targeted profitability levels.

- The Prevail platform now operates in 10 agency states with approximately 30-state launches planned by early 2027, creating meaningful growth opportunities in the retail channel.

- Employee Benefits reported an impressive 8.2% core earnings margin, driven by strong results in life and disability.

- The business is expanding into the under-500-lives segment with enhanced product offerings, including dental and vision coverage.

Despite strong fundamentals and disciplined execution, Hartford Insurance trades at $141, offering upside for investors who recognize the company’s competitive positioning in property and casualty insurance.

See analysts’ full growth forecasts and estimates for HIG stock (It’s free) >>>

What the Model Says for Hartford Insurance Stock

We analyzed The Hartford as it transformed into a technology-enabled insurance leader, with market-leading positions across business, personal, and employee benefit lines.

The company benefits from multiple growth drivers.

- In Business Insurance, the focus on small- and mid-market customers provides stability and growth potential.

- Small Business renewal written pricing of 4.3% all-in, or 7.7% excluding workers’ compensation, demonstrates pricing power in a competitive environment.

- The Hartford’s investments in AI and digital capabilities create operational advantages.

- These technologies improve underwriting speed and accuracy while enhancing agent, broker, and customer experiences.

- Management expects these investments to drive both top-line growth and improvement in the expense ratio over time.

- Personal Insurance presents additional upside as the Prevail platform expands into agency distribution.

- With 15% growth in written premiums in the agency channel during Q4 2025, the company is executing on its strategy to leverage retail distribution relationships.

Using a forecast of 4.6% annual revenue growth and 17% operating margins, our model projects the stock will rise to $181 within 2.8 years. This assumes a 9.7x price-to-earnings multiple.

That represents compression from Hartford’s historical P/E averages of 10.4x (one year) and 9.8x (five years). The conservative multiple acknowledges potential softening in property pricing and competitive pressures in certain casualty lines.

The real value lies in capturing profitable growth across diversified insurance lines while leveraging technology investments to improve margins and customer experience.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for HIG stock:

1. Revenue Growth: 4.6%

The Hartford’s growth centers on market-share gains in Business Insurance and on policy-count expansion in Personal Insurance.

The company delivered strong written premium growth across all three Business Insurance units in 2025, with Small Business up 9%.

Management expects continued momentum as investments in digital capabilities and AI-driven workflows differentiate The Hartford from competitors.

Agency partners increasingly want to consolidate business with fewer carriers that meet all their needs, positioning The Hartford to benefit from this structural shift.

2. Operating margins: 17%

The Hartford has maintained strong profitability through disciplined underwriting and risk selection.

Business Insurance achieved an 88.5% underlying combined ratio in 2025, while Personal Insurance improved significantly, with auto returning to targeted profitability.

Management sees opportunities to improve the expense ratio, as premium growth provides leverage and technology investments enhance operational efficiency.

The company targets expense ratios below 30% in Business Insurance and below 25% in Personal Insurance by the end of 2027.

3. Exit P/E Multiple: 9.7x

The market currently values Hartford Insurance at 10.5x earnings. We assume the P/E will compress modestly to 9.7x over our forecast period.

Property pricing moderation and competitive dynamics in certain casualty lines create near-term headwinds.

However, as The Hartford demonstrates resilient execution across its diversified portfolio and technology investments drive operational improvements, the company should maintain attractive valuations.

The company’s strong capital generation supports shareholder returns, with share buybacks increasing to $450 million quarterly beginning in Q1 2026.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

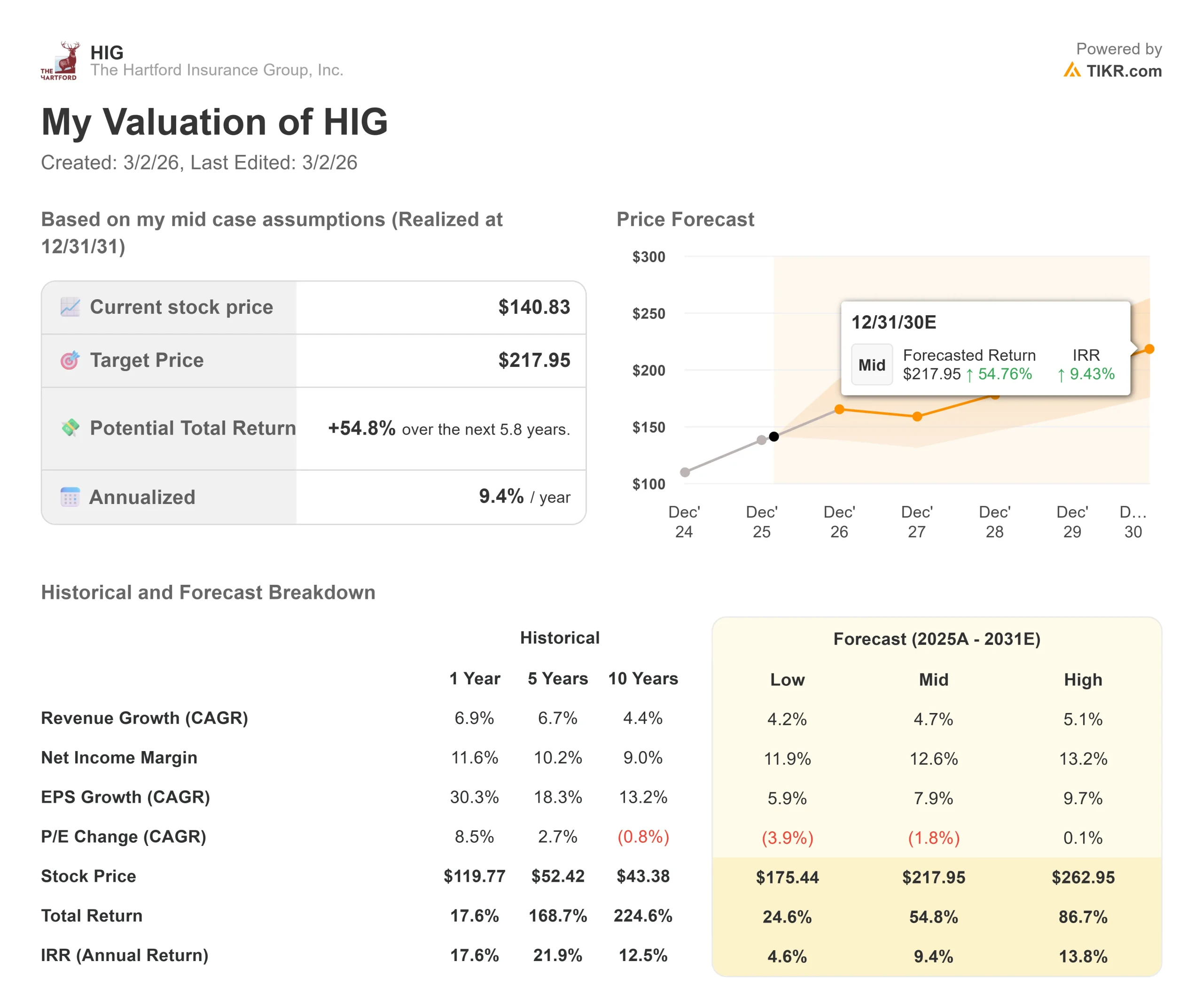

Insurance companies face market cycles and volatility from catastrophes. Here’s how Hartford Insurance stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 4.2% and net income margins compress to 11.9%, investors still see a 24.6% total return (4.6% annually).

- Mid Case: With 4.7% growth and 12.6% margins, we expect a total return of 54.8% (9.4% annually).

- High Case: If market share gains accelerate to 5.1% revenue growth while The Hartford maintains 13.2% margins, returns could hit 86.7% total (13.8% annually).

See what analysts think about HIG stock right now (Free with TIKR) >>>

The range reflects execution on technology investments, navigation of insurance market cycles, and success in expanding the Personal Insurance agency business.

In the low case, property pricing deteriorates faster than expected or casualty loss trends accelerate.

In the high case, AI-driven capabilities create stronger competitive moats, expense ratios improve ahead of schedule, and premium growth exceeds expectations across all business lines.

How Much Upside Does Hartford Insurance Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!